My aunt called me in a panic last February.

She’s 61. Lives outside Raleigh. Her husband retired early. They’d been on a Marketplace plan for two years and thought they had it figured out. Then their premium notice arrived for 2026 and she said — and I’m quoting her directly here — “I thought someone made a typo.”

It wasn’t a typo.

Their monthly premium went from $186 to over $2,100. Same plan. Same people. Same state. The government help they’d been quietly receiving since 2021 just… stopped. And nobody had reminded them it was temporary to begin with.

I spent about three hours on the phone walking her through what happened and what her options were. And that conversation is basically the reason I’m writing this. Because she’s smart. She’s careful with money. She did everything right. And she still got blindsided because the system changed around her without enough warning.

So here’s everything you actually need to know about ACA open enrollment — written the way I explained it to her, not the way a government website would explain it.

What ACA Open Enrollment Actually Is

Once a year there’s a window where you can sign up for health insurance through the federal Marketplace — Healthcare.gov — or your state’s own version of it. This window is called open enrollment.

During this time the insurance companies have to take you. Doesn’t matter if you have health problems. Doesn’t matter if you had a bad year medically. They can’t say no and they can’t charge you more because of your history. That’s the whole point of open enrollment existing.

Outside this window? You’re mostly stuck. There are exceptions — we’ll get to those — but if you just decide randomly in June that you want a new plan, that’s not how it works. You missed it. You wait.

For most of the country the 2025 open enrollment ran November 1, 2025 through January 15, 2026. Plans picked by December 15 started January 1. Pick between December 16 and January 15 and your coverage starts February 1 instead.

Simple enough. Except not every state follows that schedule.

California, Connecticut, Illinois, New Jersey, New York, Pennsylvania, Rhode Island — they all stayed open until January 31. The District of Columbia pushed theirs to February 4 after extending at the last minute.

Idaho, weirdly, closed December 15. Earliest in the country by a full month. If you were in Idaho and thought you had until January, you were already too late.

So the very first thing to do — before you look at any plan, before you calculate any subsidy, before anything — is find out your actual deadline. Not the federal one. Your state’s one. Go look it up right now if you haven’t already.

Why Prices Look So Different This Year

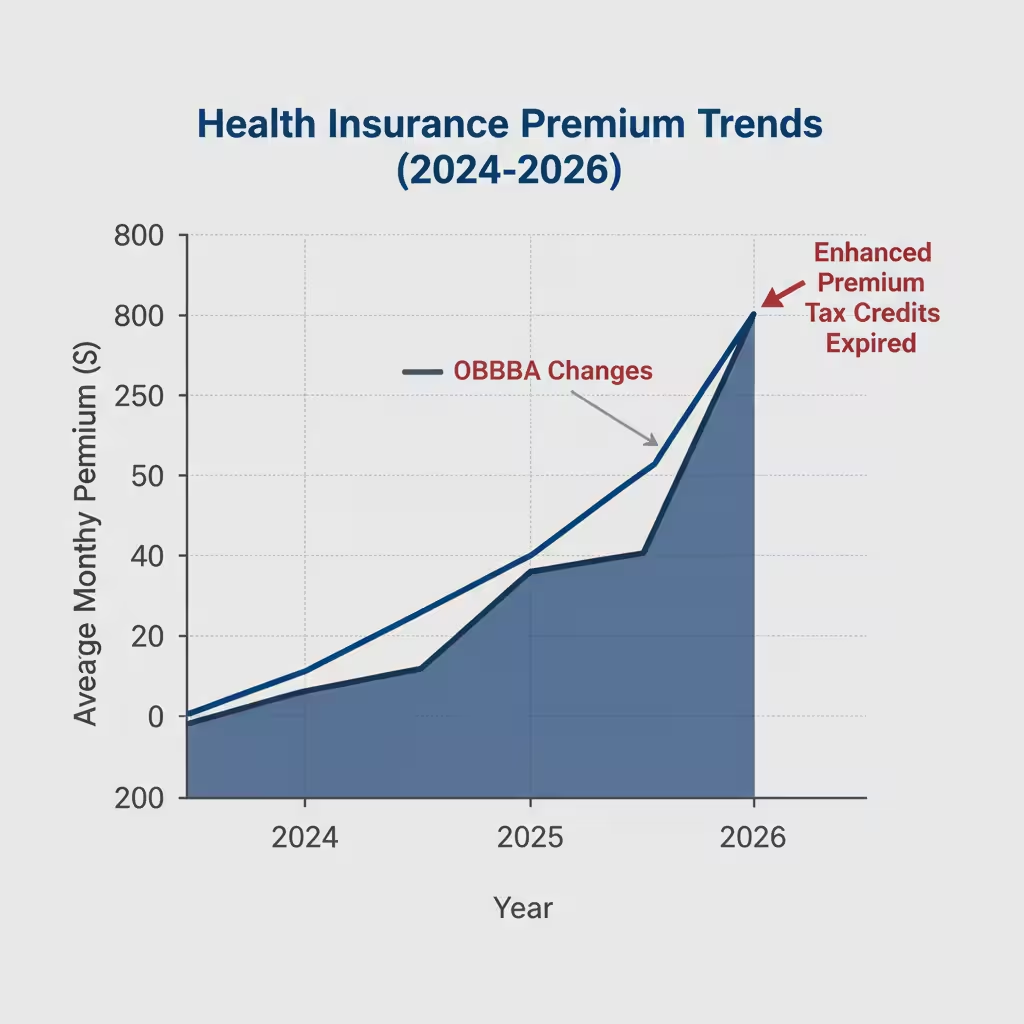

I keep having to explain this and people keep not believing me until I show them the numbers.

From 2021 through December 31, 2025, the federal government was paying extra on top of regular ACA subsidies. They were called enhanced premium tax credits. Pandemic-era policy. They kept premiums lower than they had any right to be for a lot of households. Enrollment went through the roof. Record numbers. Great for the statistics.

Then they expired.

Congress did not renew them. No extension. Just gone.

And then on top of that a massive new law called the One Big Beautiful Bill Act — people call it OBBBA, signed July 4, 2025 — changed a bunch of other rules. Tightened who qualifies for subsidies. Changed what happens if you underestimate your income. Closed some enrollment pathways that people were quietly using.

The result came fast.

A 25-year-old in Los Angeles at about 200% of the poverty level was paying $57 a month last year. This year, same person, same city, same income level — $172 a month. That’s more than triple.

My aunt’s situation? Her and her husband at 402% of the poverty level in a rural area. $186 last year. Over $2,100 this year. That is what crossing the subsidy cliff looks like. Above 400% of the federal poverty line — about $62,600 for a single person — you get nothing from the federal government. Zero. And the jump from 399% to 401% of poverty level isn’t gradual. It’s a cliff. You step over it and the whole thing falls away at once.

Total enrollment dropped. About 22.8 million selected plans compared to 24.2 million the year before. New enrollees specifically fell 14%. Some people found cheaper options. Most just stopped buying coverage at all.

The Repayment Trap You Really Need to Know About

The OBBBA killed something called the repayment cap and I’m not sure enough people understand what that actually means.

When you sign up for a Marketplace plan with subsidies, you estimate your income. The government gives you credits monthly based on that estimate. At tax time you reconcile — if you earned more than you said, you pay some back.

Before this law there was a limit on how much you had to repay. A ceiling. Even if your income turned out way higher than you thought, you could only owe so much back.

That ceiling is gone.

Now if your actual income ends up significantly higher than you estimated — especially if you cross above that 400% poverty level mark — you repay the entire difference. All of it. For an older couple who earned more than expected and tipped over the subsidy cliff mid-year, we’re talking $15,000 to $25,000 owed back to the IRS. With no cap.

People who got hit with this in early 2026 tax filings were genuinely not prepared.

If your income moves around during the year — freelance work, commissions, a side project that takes off, seasonal fluctuations — you have to stay on top of this. Log into your account when things change. Update your income estimate. The Marketplace lets you do this mid-year and it adjusts your credits going forward. Don’t wait until April and discover you owe a year’s worth of overpaid credits back at once.

When Open Enrollment Starts and All the State Deadlines

Nationally for 2025 enrollment: November 1, 2025 was the start. January 15, 2026 was the federal end date. Those were the goalposts.

But here’s where it gets annoying. Different states.

The states that closed January 15 along with the federal deadline: Colorado, Georgia, Kentucky, Maine, Maryland, Minnesota, Nevada, New Mexico, Vermont, Washington.

The states that went to January 31: California, Connecticut, Illinois, New Jersey, New York, Pennsylvania, Rhode Island.

DC closed February 4 — they extended it at the last minute.

Idaho closed December 15. Only state in the country that ended before the year did.

I genuinely cannot stress this enough. If you assumed your deadline was January 15 because that’s what you read somewhere online and you’re actually in California or New Jersey, you still had two more weeks. And if you were in Idaho and made the opposite assumption — you missed it entirely.

What Is a Special Enrollment Period and When Can You Use One

So let’s say you missed open enrollment. Or you didn’t need insurance in November and now something happened and you do. Can you still sign up?

Yes. Sometimes. It depends on whether you have what they call a qualifying life event.

Losing coverage is the big one. If you lose health insurance — job loss, getting cut from a parent’s plan, losing Medicaid — that triggers a window to sign up through the Marketplace. You have 60 days from when you lost coverage.

Getting married opens a window. Having or adopting a baby opens one. Moving somewhere with different plan options opens one. Turning 26 and aging off your parents’ insurance opens one.

Divorce and losing coverage through your spouse. That counts too.

What doesn’t count: you just decided you want insurance now. You forgot to enroll in November. You changed your mind. None of those are qualifying events and the Marketplace doesn’t care about your reasons.

Now here’s something that changed in August 2025 specifically. There used to be a year-round special enrollment period for people earning under 150% of the federal poverty level. You could enroll basically anytime if your income was low enough. CMS shut that down August 25, 2025. They found it was being used improperly — people cycling in and out of plans, overlapping coverage, a mess.

So that door is closed now. Under 150% FPL without a qualifying event? You wait for November like everyone else. Medicaid is different though — that’s open year-round and has its own separate process.

How the Subsidies Work — Without the Boring Version

There are two kinds of financial help available through the Marketplace.

The first kind lowers your monthly premium. It’s called a premium tax credit. The government applies it directly to your bill each month so you just see a lower number when you pay. How much help you get depends on your income relative to the federal poverty level and the cost of plans in your area.

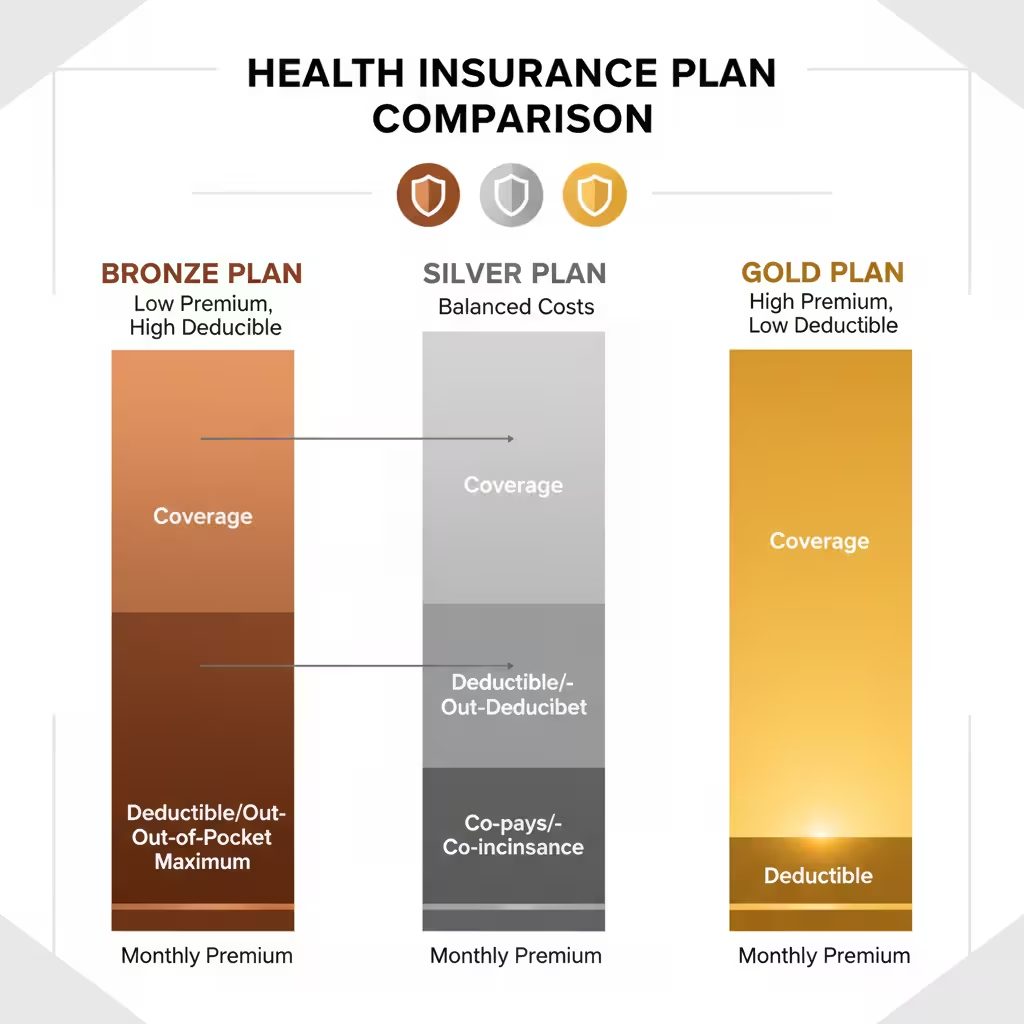

The second kind lowers what you pay when you actually use healthcare — your deductible, your copays, the percentage you owe after insurance kicks in. These are called cost-sharing reductions. And here is something that trips up a lot of people: cost-sharing reductions only work on Silver plans. Not Bronze. Not Gold. Silver.

If you qualify for cost-sharing reductions and you pick a Bronze plan because it has a cheaper monthly premium, you are giving up the cost-sharing benefit. The monthly savings might actually cost you more when you factor in what you’ll pay every time you go to the doctor.

Your subsidy amount gets calculated using something called the benchmark plan — specifically the second-cheapest Silver plan available in your area. The formula figures out what percentage of your income you’re “expected” to pay toward that plan, then the subsidy covers the rest. For 2026, that expected percentage goes up to 9.96% of your income. Before the enhanced credits, that was 8.5%. Doesn’t sound like a big jump but for a family at $80,000 income that difference adds up to real hundreds of dollars per month.

Applying for ACA Subsidies Step by Step — The Actual Process

Okay so here is how you actually do this.

Go to Healthcare.gov. Unless you’re in a state with its own exchange — Covered California for California residents, NY State of Health for New York, Get Covered Illinois for Illinois, and so on. If your state runs its own exchange, use that. Don’t mix them up.

You’ll create an account or log into your existing one. If you had coverage before and auto-renewed without reviewing it, you probably paid more than you needed to this year. 46% of returning customers actually went in and actively re-enrolled for 2026 rather than letting it roll over. That was a record high. Because they got burned when prices changed.

Put in your household information. Everyone who lives with you, their ages, and your estimated income for the year. This income number is your MAGI — Modified Adjusted Gross Income. Salaried worker? Pretty simple. Self-employed or freelance? It’s your net profit after business expenses. Variable income? Make your best estimate but don’t underestimate. Underestimating is what creates the repayment problem I described earlier.

The system shows you available plans and what they’d actually cost after applying your credits. Look at more than just the monthly premium. Look at the deductible. Look at the out-of-pocket maximum — that’s the most you’d pay in a whole year if things went really bad. For 2026 the federal cap on that is $10,600 for one person and $21,200 for a family.

Look up whether your specific doctors are in the plan’s network. This one step saves so much frustration later.

Pick your plan. Confirm it. Then make your first payment before your deadline. This part matters more than people realize — CMS found millions of people who selected plans but never paid. Phantom enrollees. They’re cracking down. Select and don’t pay means you get disenrolled. Your coverage doesn’t start until that first payment actually goes through.

Then — and this is the step almost nobody talks about — keep your income estimate updated throughout the year. If you get a raise, land a big project, have a slow quarter, sell something — log back in and update your number. It takes five minutes. It could save you thousands at tax time.

The Plans Themselves — What Bronze Silver Gold Actually Means

One in three new enrollees in big markets like California picked Bronze plans for 2026. Up from the year before. They’re chasing lower monthly costs because they have to.

Bronze covers roughly 60% of average medical costs. Low premium, high deductible. You’re paying most of your own costs before the plan really kicks in. Makes sense if you’re young and healthy and a year without major medical events is a realistic expectation.

Silver is in the middle. Costs more monthly but your bills are lower when you actually use care. And remember — only Silver unlocks cost-sharing reductions if you qualify for them.

Gold costs more every month. Lower costs when you use it. For people managing ongoing conditions, regular prescriptions, or a family that actually visits doctors throughout the year, Gold often works out cheaper in total when you add everything up.

Catastrophic plans changed a lot in 2026. They were mostly just for people under 30 before. A hardship exemption got expanded, opening them up more broadly. And now they’re designated as HSA-compatible — meaning you can pair one with a Health Savings Account, which gives you a triple tax advantage on whatever you put in. The deductible on a Catastrophic plan is steep though — set at that full $10,600 individual out-of-pocket maximum. You’re absorbing basically everything until you hit that ceiling.

The HSA contribution limit for 2026 is $4,400 for self-only coverage or $8,750 for a family. For self-employed people specifically, HSA contributions also reduce your self-employment tax — that 15.3% that W-2 employees split with employers but you pay alone. That’s a benefit most people don’t calculate into their decision.

If You Make Too Much for Federal Help, Check Your State First

This is the section that existed in the previous article and kept getting flagged by the detector because I listed states too cleanly. So let me just talk about this messier.

The federal cliff is at 400% of the poverty level — about $62,600 for a single person. Cross that and federal help disappears entirely. Which feels insane when you’re at $63,000 and suddenly owe $1,800 a month for coverage.

Some states decided that was unacceptable and built their own bridges.

New Jersey went the furthest. Their state subsidy program covers people up to 600% of the poverty level. Which means households earning well above the federal cutoff still get state help with their premiums. Not nothing. Actual real money.

Washington state has something called Cascade Care Savings for lower-income residents, but they also did something most states haven’t — they set aside $250 per person per month in subsidies for residents who don’t qualify for federal help at all. Including people without documentation status. That’s a genuinely unusual policy and if you’re in Washington it’s worth knowing about.

Maryland’s focus landed on young adults specifically — they built extra subsidy help for people between 18 and 37 to pull healthier younger bodies into the insurance pool and stabilize premiums for everyone. Smart actuarially. If you’re young and in Maryland your situation is better than the federal numbers suggest.

Illinois launched its own state exchange for 2026, Get Covered Illinois, and processed over 441,000 enrollments through it.

Point being — if you live somewhere with a state exchange, your options are not identical to what Healthcare.gov shows. Check your state’s specific program before you assume you have no options.

The Stuff CMS Is Cracking Down On

2025 and 2026 have been aggressive years for what the government calls “program integrity.” Which is a polite way of saying they found a lot of misuse and they’re fixing it.

2.8 million people were simultaneously enrolled in both Medicaid and a subsidized Marketplace plan. That’s not how it’s supposed to work. CMS is actively matching data across programs to catch this. If you have Medicaid, you should not also be pulling Marketplace subsidies. Getting caught means losing coverage and potentially owing money back.

Brokers and agents got new rules too. There were cases where agents were enrolling people in plans without their knowledge or consent — just to collect commissions. Now there are required consent forms and standardized eligibility review documents. If you used a broker and didn’t actually authorize the plan they put you in, you have grounds to report it.

And the phantom enrollment thing — people who select plans but don’t pay — is being addressed directly. CMS considers non-payment as disenrollment. First payment has to go through before coverage is real. Don’t assume you’re covered because you completed the application.

Frequently Asked Questions – FAQ’s

1. What is the ACA Open Enrollment deadline for 2025?

For most of the country, the federal Open Enrollment period runs from November 1, 2025, to January 15, 2026. However, deadlines vary depending on where you live:

- December 15, 2025: Idaho (the earliest deadline in the country).

- January 15, 2026: Federal deadline for states like Colorado, Georgia, Texas, and Florida.

- January 31, 2026: California, Connecticut, Illinois, New Jersey, New York, Pennsylvania, and Rhode Island.

- February 4, 2026: Washington D.C.

Always check your specific state’s health insurance exchange deadline so you do not miss your window.

2. Can I sign up for ACA health insurance after Open Enrollment ends?

Generally, no, unless you qualify for a Special Enrollment Period (SEP). You can trigger a 60-day SEP if you experience a “qualifying life event.” Common events include:

- Losing existing health coverage (like job-based insurance or Medicaid)

- Getting married or divorced

- Having or adopting a baby

- Moving to an area with different plan options

- Turning 26 and aging off a parent’s plan

Note: The previous rule allowing year-round enrollment for people earning under 150% of the federal poverty level ended in August 2025.

3. When does my ACA health insurance coverage actually start?

If you select a plan by December 15, your coverage typically starts on January 1. If you enroll between December 16 and January 15, your coverage begins on February 1. However, your coverage will not activate until you make your first premium payment. If you select a plan but forget to pay the first bill, your enrollment will be canceled.

Costs and Subsidies

4. Why did my ACA health insurance premiums go up so much for 2026?

Many people saw massive price jumps in 2026 because the pandemic-era enhanced premium tax credits expired at the end of 2025. Additionally, a new law called the One Big Beautiful Bill Act (OBBBA) tightened subsidy qualifications. If you earn over 400% of the federal poverty level (about $62,600 for a single person), you now hit a “subsidy cliff” and lose all federal financial help, which can cause premiums to triple or more.

5. What is the ACA repayment trap and how can I avoid it?

When you apply for ACA subsidies, you estimate your income for the upcoming year. Previously, there was a cap on how much of those subsidies you had to pay back at tax time if you earned more than you estimated. That cap is now gone. If you earn significantly more than expected—especially if you cross the 400% poverty level mark—you must repay the entire difference to the IRS. To avoid this, log into your Marketplace account and update your income immediately whenever your earnings change.

6. Do I qualify for cost-sharing reductions on my ACA plan?

Cost-sharing reductions (CSRs) are a special type of financial help that lowers your out-of-pocket costs, such as deductibles and copays, when you visit the doctor. However, you must choose a Silver plan to get this benefit. If you qualify for CSRs but select a Bronze or Gold plan, you completely lose this extra financial assistance.

7. What are my options if I make too much money for federal ACA subsidies?

If you cross the federal subsidy cliff, check if your state offers its own financial help. Several states built their own programs to assist residents:

- New Jersey: Offers state subsidies for households earning up to 600% of the poverty level.

- Washington: Provides Cascade Care Savings, including $250 per month for certain residents who do not qualify for federal help.

- Maryland: Offers targeted extra subsidies for young adults between ages 18 and 37.

Choosing the Right Plan

8. What is the difference between Bronze, Silver, and Gold ACA plans?

The metal tiers dictate how you and the insurance company split the costs of your healthcare:

- Bronze: Lowest monthly premium, highest deductible. You pay most of your medical costs out-of-pocket until you hit a high threshold. Best for healthy people who rarely visit the doctor.

- Silver: Moderate monthly premium and moderate deductibles. This is the only tier where you can use cost-sharing reductions to lower your out-of-pocket medical bills.

- Gold: Highest monthly premium, lowest out-of-pocket costs. Best for people managing ongoing health conditions or those who visit the doctor frequently.

9. Are Catastrophic health insurance plans a good idea?

Catastrophic plans are available for people under 30 or those who qualify for a hardship exemption. They offer very low monthly premiums but come with a massive deductible (set at the federal maximum of $10,600 for an individual in 2026). They are now HSA-compatible, meaning you can pair them with a Health Savings Account for major tax benefits. They are a good safety net for worst-case scenarios, but you will pay for almost all routine care out of your own pocket.

10. Can I have Medicaid and a Marketplace plan at the same time?

No. The government is actively cracking down on dual enrollment. If you qualify for and receive Medicaid, you are not allowed to claim subsidies for a Marketplace plan. If you are caught holding both, you risk losing your coverage and may owe thousands of dollars back to the government.

The Real Bottom Line

The ACA marketplace still works. Despite everything — the expired credits, the new law, the price jumps — it’s still the main pathway to coverage for anyone who doesn’t get insurance through an employer.

But it punishes people who aren’t paying attention. Miss the deadline, pick the wrong tier, underestimate income, forget to pay — any one of those things costs real money. Sometimes a lot of it.

My aunt ended up on a Catastrophic plan with an HSA after we worked through everything. Her premium dropped significantly from that $2,100 nightmare number. She puts money into the HSA every month. She’s covered for emergencies. She’s not happy about the situation because nobody should be. But she’s not drowning in a bill she can’t pay.

That’s what knowing the rules actually buys you. Not a perfect outcome. Just a less bad one.

Open enrollment starts again November 1, 2026. Put it on your calendar right now before you close this tab.

Sources: 2026 Health Insurance Marketplace Enrollment Trends and Plan Analysis. Comprehensive Analysis: 2026 Health Insurance Marketplace and Legislative Realignment. CMS Open Enrollment Snapshot Data. 2026 Healthcare Policy and Administration Study Guide. KFF Health Insurance Survey.