My cousin Derek rear-ended someone on a Tuesday. Not badly. Low speed. Nobody got hurt. The other car had a scratch on the bumper, maybe a small dent. He filed the claim, got it handled, moved on with his life.

Then his renewal came.

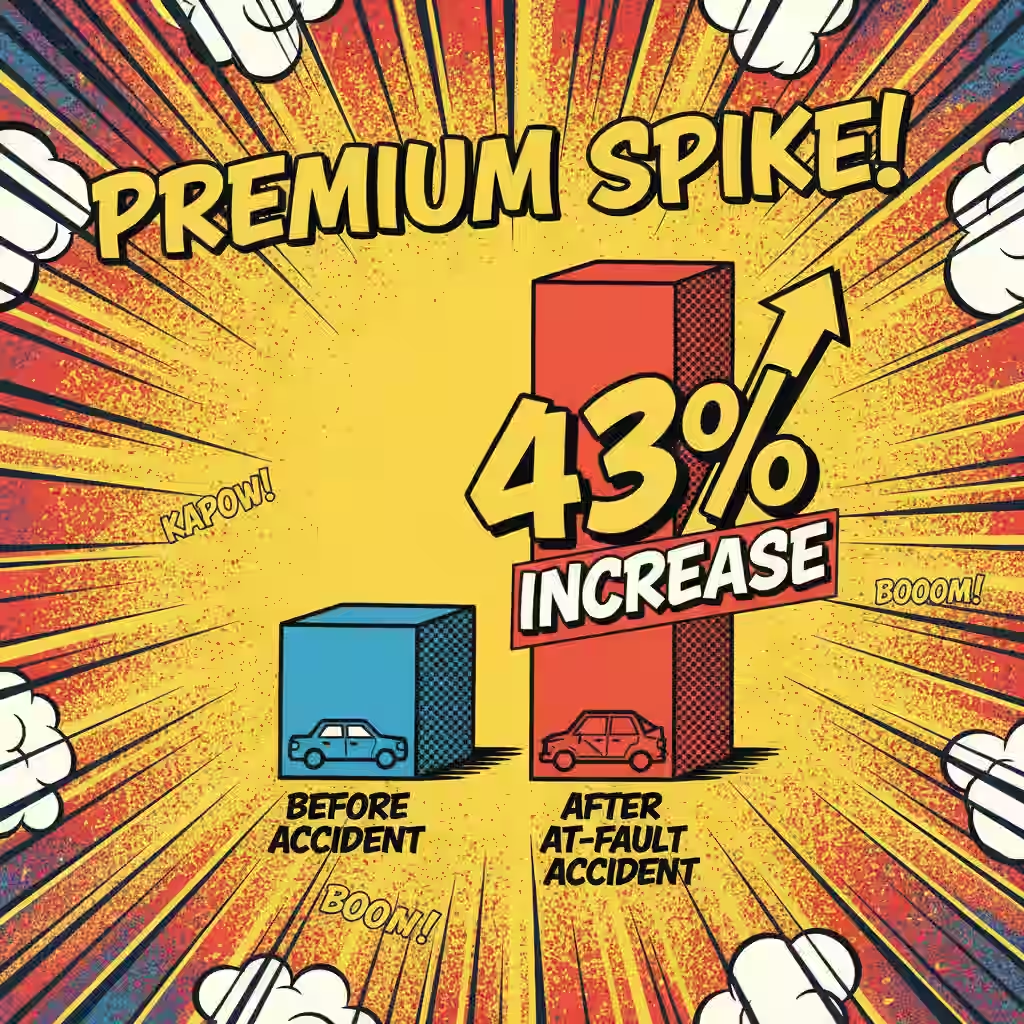

$94 more per month. Same car. Same neighborhood. Same everything — except now he had one at-fault accident on his record, and his insurer treated him like a completely different person.

That’s the part nobody tells you before the accident happens.

Here’s what actually goes on behind the scenes when you file a claim. Insurers pull something called your “claims history.” It’s basically a running tab of every accident, every claim, every incident connected to your name and your vehicle. The moment an at-fault accident hits that file, your risk profile jumps. You move from one pricing bucket to a more expensive one. And the new rate reflects that — immediately, at your very next renewal.

The average premium spike after a single at-fault accident? Around 43% nationally. In some states it’s worse. California drivers with a bodily injury accident on record can see premiums nearly double — up to 97% in some documented cases.

Ninety-seven percent. On top of what you were already paying.

How Long Does an Accident Affect Car Insurance Rates?

Three to five years. That’s the window most people are looking at.

But I want to be precise here because “three to five years” can mean different things depending on where you live and what carrier you’re with. Most accident-related surcharges stay active on your policy for three years minimum. In states like North Carolina, major violations now carry a five-year lookback period following 2025 legislative changes. And here’s the part that surprises people — even after the surcharge drops off your policy, the accident can still sit on your driving record for seven to ten years.

Those are two different clocks running at the same time.

Your insurer’s surcharge clock: three to five years. Your DMV record clock: seven to ten years.

When you go shopping for a new policy, carriers pull your driving record — not just your current insurer’s file. So an accident from six years ago might not be surcharging you anymore, but a new carrier could still see it and factor it into their quote. Not always a dealbreaker. But worth knowing.

What “At-Fault” Actually Means for Your Rate

Not every accident hits your rate the same way.

A minor at-fault accident — say, under $1,000 in property damage — triggers a different surcharge than one involving bodily injury, multiple vehicles, or a fatality. Insurers assign what’s called “claims severity” to each incident. Higher severity equals higher surcharge. Simple math, painful reality.

And then there’s the at-fault question itself. Some accidents are genuinely disputed. If your insurer determines you’re partially at-fault — even 20% — that can still trigger a surcharge in most states. North Carolina is an interesting case here. It runs under “contributory negligence,” meaning if you’re found even 1% at fault, you can be blocked from any compensation from the other driver. But your own insurer? They’re still watching that 1%.

The distinction between “at-fault” and “not-at-fault” matters enormously. Not-at-fault accidents — where you were hit, documented, police report filed — typically don’t trigger rate surcharges. Typically. Some carriers in high-cost markets do look at claim frequency regardless of fault, especially if you’ve filed two or three not-at-fault claims in a short window. The logic, as unfair as it sounds: if accidents keep finding you, statistically you’re a higher risk.

Will My Insurance Drop Me After 2 Accidents?

Straight answer: maybe.

One accident — most standard carriers keep you. They surcharge you, yes. But they don’t drop you.

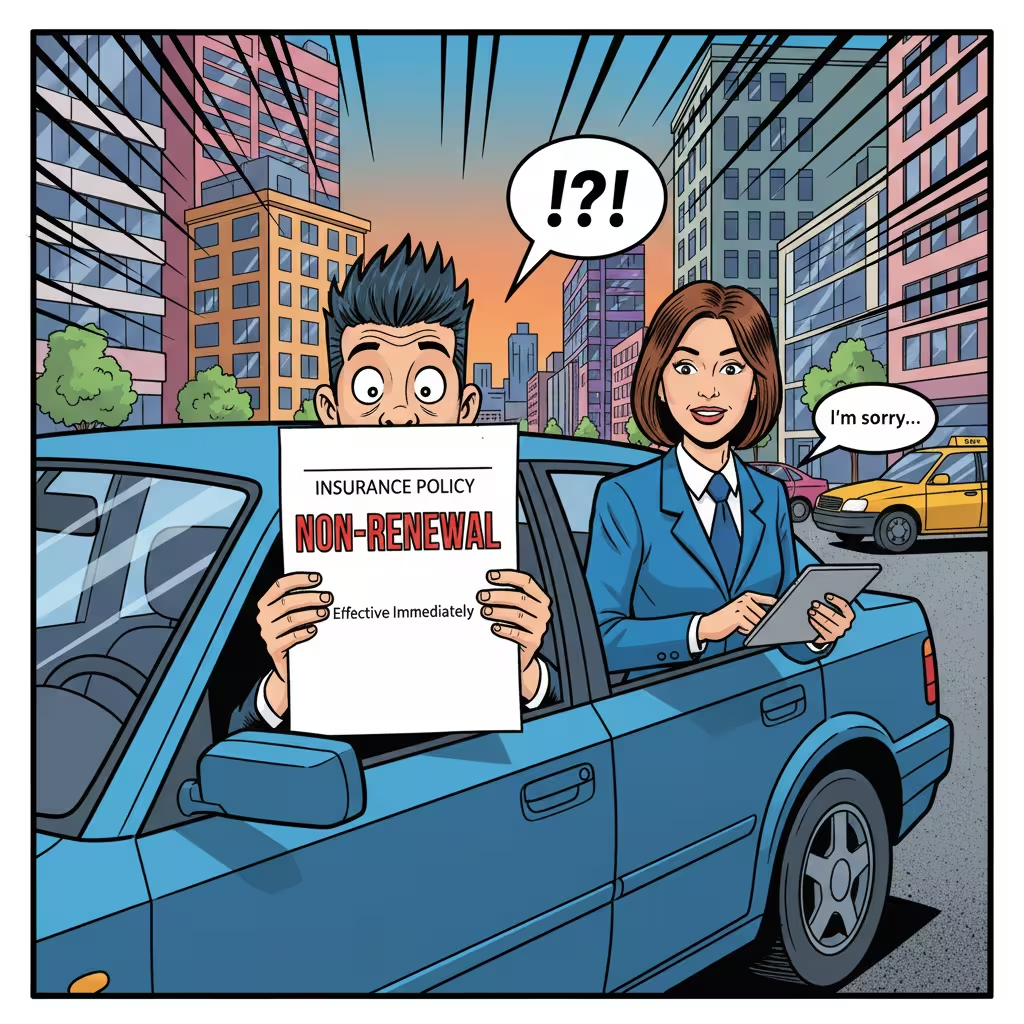

Two accidents in three years? That’s where it gets dicey. Some carriers have internal thresholds. Two at-fault accidents within a policy period can push you out of their “preferred” tier into a “non-standard” tier — or out of the company entirely at renewal. They don’t have to tell you why in most states. The non-renewal notice just shows up.

Three accidents? You’re almost certainly looking at a non-standard carrier or possibly the state’s assigned risk pool — a last-resort program where coverage is guaranteed but priced accordingly, and “accordingly” means expensive.

I’ve talked to people who’ve been through this. The assigned risk pool isn’t a death sentence, but it’s not fun either. Rates in those pools run significantly above market. And you typically stay there until you’ve rebuilt enough clean years on your record to qualify for voluntary market coverage again.

High-Risk Auto Insurance: What It Actually Looks Like

“High-risk” is a label, not a life sentence. But it does change your options.

Once an insurer classifies you as high-risk — whether from accidents, a DUI, multiple violations, or poor credit in states that allow credit scoring — your carrier pool shrinks. The big national names get selective. Some won’t quote you at all. Others will quote you at rates that feel punitive.

But here’s what I’ve found actually works in that situation: shop aggressively, and know which carriers specialize in imperfect records.

In 2026, State Farm holds the top value position for high-risk profiles according to MoneyGeek data. Their average annual rate for drivers with one violation sits around $715 — roughly $38/month cheaper than comparable top-rated insurers. Travelers scores highest overall (93 out of 100) for coverage options and claims handling quality in the non-standard space. Progressive is the go-to specifically for DUI situations — they’ve built products around violation-specific pricing that’s more transparent than most.

The rate differences between carriers for the same high-risk profile can hit 35% or more. That’s not a small gap. That’s the difference between a manageable premium and one that breaks a monthly budget.

Accident Forgiveness — Real Protection or Marketing Fluff?

Real protection. When it actually applies.

Here’s how it works: accident forgiveness is a policy endorsement — sometimes built-in, sometimes an add-on — that waives the surcharge after your first qualifying at-fault accident. Your rate doesn’t jump. Your risk tier doesn’t change. The accident gets noted but not penalized.

Allstate offers it. GEICO offers it. Liberty Mutual offers it. Most require you to have three to five years of clean driving before you’re eligible. Some make you buy it proactively as an add-on. And the “qualifying” part matters — not every accident meets the threshold. High-damage or injury claims sometimes fall outside the forgiveness window even with the endorsement active.

The honest take: if you’ve got a clean record and you’ve been with your carrier for a few years, call and ask whether accident forgiveness is active on your policy or available to add. It’s not expensive. And if you ever need it, it’s worth every penny of the add-on cost.

The Credit Score Angle Nobody Mentions

Your driving record isn’t the only thing that changes your rate after an accident. In most states, insurers also use something called a credit-based insurance score — distinct from your regular credit score, though it pulls from the same credit history data.

Here’s why this matters after an accident: accidents are stressful. Financially stressful. And if that stress leads to late payments, higher credit card balances, or any financial disruption — your insurance score can move. Not drastically. But enough to compound the rate increase from the accident itself.

California, Hawaii, Massachusetts, and Michigan don’t allow credit scoring in auto insurance. Everyone else is fair game. If you live in one of the 46 states where it’s allowed, your credit behavior after an accident can either stabilize your rate or quietly push it higher.

Pay your bills on time. Keep balances reasonable. Boring advice. But it’s the kind of boring that saves money.

The Telematics Play for Post-Accident Drivers

This is the most underused tool available to drivers with accidents on record.

Telematics programs — Snapshot from Progressive, Drive Safe & Save from State Farm, SmartRide from Nationwide — monitor your actual driving. Braking. Speed. Time of day. Mileage. And they price based on what they see, not on what happened two years ago.

For a driver with one at-fault accident on their record, telematics is a genuine path back toward lower rates. You can’t undo the accident. But you can demonstrate — in real time, month over month — that your current driving behavior is low-risk. Some programs offer up to 40% savings at renewal for safe driving patterns.

The catch: if your driving habits aren’t great, telematics can work against you. Most programs let you opt out before your renewal if the data would hurt you. But you have to pay attention. Set a reminder. Check the app score monthly. Don’t sign up and forget it.

Defensive Driving Courses — Small Discount, Real Signal

Five to fifteen percent. That’s the typical discount range for completing a state-approved defensive driving course.

It’s not life-changing money. But here’s why I think it’s worth doing anyway: it sends a signal. To your carrier. To new carriers you might shop with. That you took a step after the accident to actively reduce your risk. Some states also let a course reduce license points, which matters for the DMV-side of your record separately from the insurance-side.

Check your state’s DMV website for approved courses. Most can be done online now. A few hours, a modest fee, a small discount — and a paper trail that shows you’re not just waiting out the clock.

How to Actually Shop Car Insurance With an Accident on Record

Don’t just call your current carrier and ask for help.

I mean, call them — but don’t stop there. Rate differences for identical profiles between carriers can reach 35% in 2026. Your current insurer has your accident baked into their pricing model. A competitor might weigh it differently.

A few things to do right now if you’ve got an accident on record:

Get quotes from at least three carriers. Include at least one that specializes in non-standard or high-risk profiles — Progressive and State Farm are solid starting points. Ask specifically about accident forgiveness status on any new policy. Ask whether telematics enrollment changes the quoted rate.

Talk to an independent agent. Not a captive agent who sells one brand. An independent who shops multiple carriers. They see the spread between quotes that you’d have to call six companies to find yourself.

And don’t wait until renewal. You can switch mid-policy in most states. If you find a significantly better rate right now, you can move. Your current carrier refunds the unused premium. There’s no loyalty bonus for overpaying.

The 3-5 Year Game Plan

You’ve had an accident. The rate went up. Here’s the honest timeline.

Year 1: Surcharge hits at renewal. Shop hard. Enroll in telematics. Take a defensive driving course. Monitor your credit-based insurance score.

Year 2: Keep your record clean. Check in with your agent about whether any discounts have changed. If you enrolled in telematics and your scores are solid, ask about renewal pricing.

Year 3: For many carriers, this is where a minor accident starts to lose weight on your rate. Some surcharges drop off entirely. Re-shop your policy — the market has likely shifted and your profile is meaningfully cleaner.

Year 5: For most drivers, this is full reset territory. A single at-fault accident from five years ago carries very little weight with most standard carriers. You may be back to preferred pricing.

The key is not making it worse in the meantime. One more at-fault accident restarts that clock. A DUI extends it dramatically. A lapse in coverage — even a few weeks — can requalify you as high-risk with a new carrier and erase the progress you’ve made.

Stay insured. Drive clean. Work the timeline.

Frequently Asked Questions – FAQ’s

- Does car insurance always increase after an accident?

Not always. Rate increases depend on fault, claim severity, and your insurer’s policies. - How much does car insurance go up after an accident?

On average, rates increase by 43%, but it varies by state and insurer. - How long does an accident affect car insurance rates?

Typically 3-5 years, but accidents may stay on your driving record for up to 10 years. - What is accident forgiveness in car insurance?

It prevents rate increases after your first at-fault accident, if eligible. - Can I switch insurers after an accident?

Yes, you can shop for better rates even with an accident on your record. - Do not-at-fault accidents affect car insurance rates?

Usually no, but frequent claims may still impact rates with some insurers. - What is considered an at-fault accident?

Any accident where you’re partially or fully responsible, as determined by your insurer. - Can defensive driving courses lower my insurance after an accident?

Yes, they can provide small discounts and show insurers you’re reducing risk. - What is high-risk auto insurance?

Coverage for drivers with accidents, violations, or poor credit, often at higher rates. - How can I lower my car insurance after an accident?

Enroll in telematics programs, shop for quotes, and maintain a clean driving record.

Bottom Line

An accident changes your rate. That’s just true. But it doesn’t have to change it forever, and it doesn’t have to change it as much as your current carrier wants you to think.

The drivers who manage this best do three things: they shop aggressively instead of just accepting the renewal, they use telematics to demonstrate their actual risk level, and they stay clean for the years it takes the record to thin out.

Derek — my cousin from the opening — ended up saving $41 a month by switching carriers three months after his accident. Same coverage. Different company. The new carrier still saw the accident. They just priced it differently.

That gap exists for most drivers. You just have to go find it.

Rates and data referenced reflect 2026 market conditions. Always verify current premiums and state-specific rules with a licensed insurance agent or your state’s Department of Insurance before making coverage decisions.