Let me tell you something that happened to my neighbor Sara last spring.

She’d been with the same insurer for nine years. Nine years, zero claims, one tiny fender-bender in 2019 that she paid out of pocket just to keep her record clean. And then her renewal showed up. She called me from her driveway, bill in hand, voice doing that thing where someone’s trying not to sound as mad as they are.

Forty-six bucks more. Per month. Same car. Same house on the same street.

I told her: it’s not you. It’s Raleigh.

Because here’s what happened. July 1, 2025 — that date matters more than most NC drivers realize. Two Senate bills went into effect and basically rewrote the rules every driver in this state plays by. The old liability minimums — $30,000 per person, $60,000 per accident, $25,000 property damage — those numbers hadn’t moved since 1999.

Monica Lewinsky was still in the news. Gas was a dollar eleven. And $30,000 felt like real money for a medical bill.

Fast forward to 2025 and that same $30,000 doesn’t cover one bad night in an ICU with a broken femur and a collapsed lung. The state knew it. They finally moved.

New floor is 50/100/50. Mandatory. No exceptions for anyone renewing or getting a new policy after July 2025.

| Coverage Type | What It Was | What It Is Now |

| Bodily Injury — One Person | $30,000 | $50,000 |

| Bodily Injury — Per Accident | $60,000 | $100,000 |

| Property Damage | $25,000 | $50,000 |

More coverage means more exposure for insurers. More exposure means higher premiums. That’s the whole story in one line.

But there’s a second piece that didn’t make the local news much. They killed something called the “liability setoff” rule. Old system: say the at-fault driver had $30K coverage. Your Underinsured Motorist payout got cut by exactly that $30K. Basically punished you for the other driver’s cheap policy. Gone now. Your UIM coverage stacks on top of their payout. For a really bad wreck — think multiple surgeries, totaled car, months off work — that change can double what you actually recover.

The NC Rate Bureau wanted a 22.6% increase to cover all this new exposure. Department of Insurance wrestled it down to 5%. Which, honestly, relative to 22.6%, almost feels like a win. Almost.

Now the rest of the country. National premiums actually dropped about 6% in 2026. Most states caught a break. North Carolina didn’t. We’re running opposite the trend — 5% up while everyone else breathes easier. People call it a “localized bubble.” I call it a catch-up tax for decades of outdated minimums.

The Windshield Thing Is Genuinely Crazy

Okay. Quick story that captures the repair cost problem better than any statistic.

Guy I know — works in IT, drives a 2023 Hyundai Tucson — got a rock chip on I-85 last October. Not even a crack. A chip. His shop quoted him $1,140.

For a chip.

Because the camera system behind his windshield runs his lane-keep assist and automatic emergency braking. Touch the glass, you’ve got to recalibrate the whole system. And recalibration isn’t a guy with a screwdriver — it’s a 90-minute procedure on a specialized alignment rack. That’s where the money goes.

This is playing out across every shop in North Carolina right now. The math is brutal:

Cars with three or more driver-assist features now average 21 days in the shop. Three weeks. That’s three weeks of rental car costs somebody’s paying — and it filters back into your premium whether you crashed or not.

Total loss claims hit 27% of all NC insurance claims in 2026. Four years ago it was 16%. Nearly doubled. Because fixing a sensor-stuffed bumper on a 2024 model often costs more than the depreciated value of the car. So they just write it off.

If you’ve got a newer vehicle and you’re carrying a high deductible to trim your monthly bill — reconsider. A low-speed parking lot hit can spiral into a total loss conversation faster than you’d think.

Eight Years. That’s the Teen Driver Surcharge Now.

Used to be three. Now it’s eight.

Any driver who got their license on or after July 1, 2025 gets tagged with the “inexperienced operator surcharge” for eight years. The percentage does drop as they rack up years behind the wheel — it’s not a flat penalty the whole stretch. But the cumulative hit?

For a family in Charlotte running a 17-year-old on their policy, rough estimates put the extra ten-year spend somewhere that could’ve bought a solid used car instead. It’s that kind of money.

The only real counterpunch is telematics. Programs that watch actual driving behavior and reward clean habits. Not optional extras at this point. If you’ve got a new driver in the house and you’re not using one of these programs, you’re just absorbing a cost that you don’t have to fully absorb.

Who’s Actually Worth Calling in 2026

North Carolina’s Rate Bureau system means every carrier starts from the same base rate the NCRB sets. But they compete hard on deviations from that base — discounts, programs, perks. Shopping isn’t just smart here. It’s the whole game.

Progressive — The Ticket-Resilient One

Starting around $61–$70/month for full coverage on a clean record. Competitive. But the real value shows up when your record isn’t spotless.

Average NC carrier bumps your rate $50/month after a speeding ticket. Progressive bumps it $20. That $30 gap sounds small until you run it out twelve months — that’s $360 you’re keeping that someone with Allstate isn’t.

Their Snapshot telematics is solid. Their “Name Your Price” tool actually works — you put in a dollar amount and it reverse-engineers coverage around your budget instead of showing you a number and hoping you don’t flinch.

Oh, and they cover pets injured in crashes. Sounds like a gimmick. Ask someone whose dog was in the car when something happened.

Reach out if: Your record has a blemish. You’re watching every dollar. You’ve got a dog who rides shotgun.

State Farm — Cheapest Entry Point, Best Family Tools

$56–$77/month for full coverage. Often the lowest base rate in the state. And they’ve got more agents in North Carolina than any other carrier — real humans, local offices, people who pick up the phone.

For the eight-year teen surcharge problem, State Farm’s “Steer Clear” and “Drive Safe & Save” programs are the sharpest tools available. But I want to be honest here — enrolling isn’t enough. You’ve got to actually use it. Check the app. Talk to your teen about what the scores mean. Families who treat it like a game see real savings. Families who sign up and forget? They don’t.

Reach out if: You’ve got a new driver. You want a local agent who knows your name.

Erie — Expensive. Worth It For Some People.

$111–$121/month. Yes, that’s higher. Quite a bit higher than most options here.

But Erie ranked #1 in the Southeast for claims satisfaction in 2026 — J.D. Power, not a press release. When you actually need the insurer to show up, Erie shows up.

Their Rate Lock is the sleeper feature nobody talks about enough. Lock your rate, and it stays flat year over year — even after you file a claim — as long as your car and address don’t change. In a year when the NCRB was swinging for a 22.6% hike, a rate lock isn’t just a perk. It’s armor.

If you’re already with Erie and locked in, do the full math before you chase a cheaper quote. That lock might be shielding you from increases you can’t see yet.

Reach out if: You’ve had a bad claims experience. You want rate predictability over the next few years.

GEICO — Best App, Not the Cheapest

Full coverage around $182/month. Pricier than most options on this list.

Their app is genuinely the best in the industry though. Fast, intuitive, doesn’t feel like it was designed in 2009. If you want a fully digital insurance life — no agents, no hold music — GEICO executes that better than anyone.

Deep discounts for federal employees, military, and students with strong GPAs. For the Research Triangle crowd — government contractors, Duke staff, UNC students — those discounts sometimes make GEICO the math winner despite the higher base rate.

Claims service trails Erie. Just know that.

Reach out if: You’re federal, military-adjacent, or a student. You want a great app above all else.

Nationwide — Built for People Who Drive Less

Liability-only around $61/month. But the real headline is SmartRide — up to 40% off at renewal for safe, low-mileage driving. Highest telematics discount ceiling in the state.

The angle most people miss: remote workers. If your annual mileage dropped from 15,000 to 5,000 when you started working from home — and you never updated your policy — you are overpaying right now. Today. That’s fixable with a phone call. Update the mileage, ask about SmartRide, and you’ll likely see a meaningful drop.

Reach out if: You work from home. You drive less than 8,000 miles a year. Your record is clean and you want to cash in on it.

USAA — If You Qualify, Start Here

$128–$131/month for full coverage. But the rate almost isn’t the point.

North Carolina has the fourth-largest military population in the country. Fort Liberty. Camp Lejeune. Seymour Johnson. Hundreds of thousands of service members and veterans live here. USAA exists for them specifically — deployment discounts that let you pause coverage while overseas, 15% off for garaging on base, and rates that run 20–45% below national averages for comparable coverage.

If you qualify — active duty, veteran, immediate military family — get a USAA quote before you call anyone else. Seriously. Before anyone else.

Reach out if: You’re military or a veteran. Non-negotiable first call.

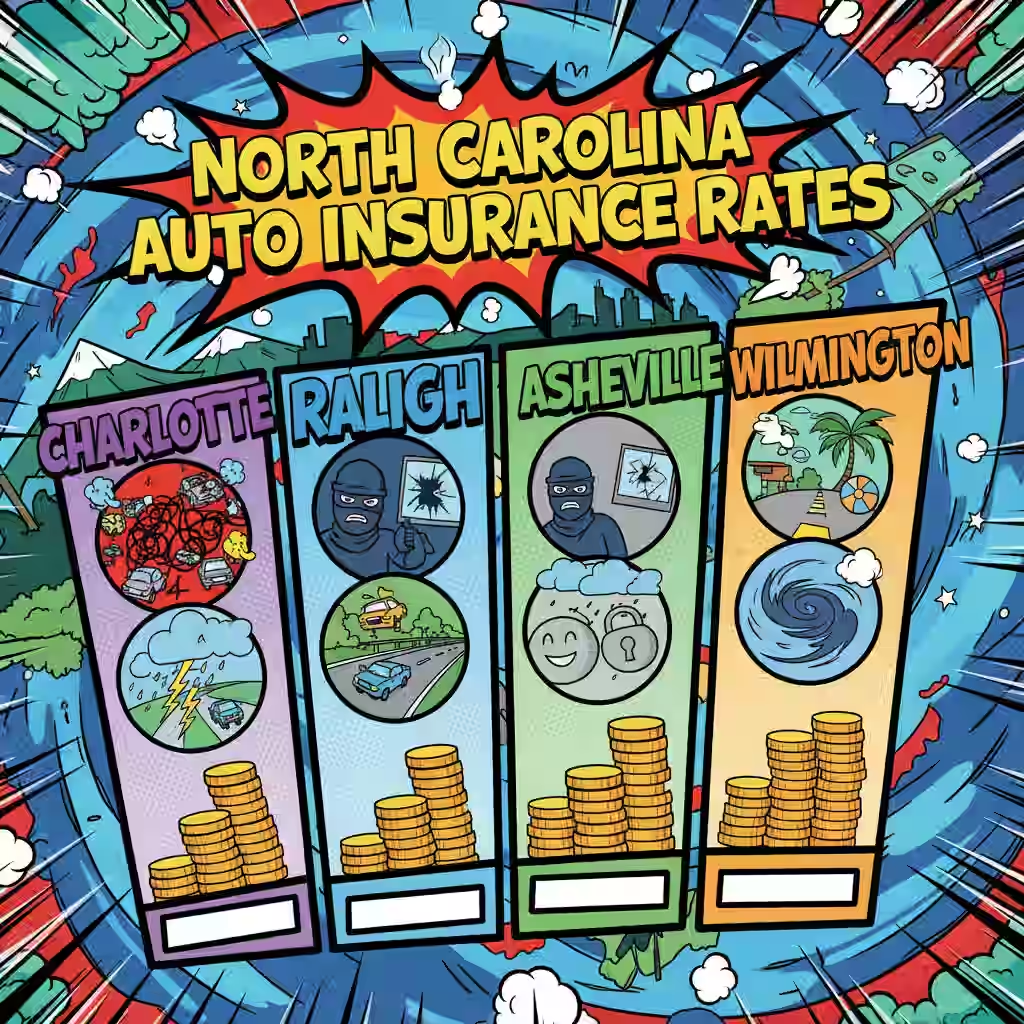

Your Zip Code Matters More Than You Think

Same car. Same record. Same coverage. Different zip code — sometimes $60/month difference. Here’s the rough picture:

| City | Average Monthly — Full Coverage | Main Cost Driver |

| Charlotte | $140–$163 | Theft volume, traffic density, claim frequency |

| Raleigh | $125–$142 | Urban corridors, population growth |

| Chapel Hill | ~$107 | Lower density, fewer serious crashes |

| Asheville | ~$78 | Rural mix, calmer traffic patterns |

Charlotte is the priciest in the state and it’s not close. If you’re insuring a car there and haven’t shopped in two-plus years, there’s a real chance you’re overpaying by $300–$500 annually.

Coastal areas — Wilmington, the Outer Banks — carry hurricane and storm surge risk that pushes comprehensive coverage up noticeably. Liability rates stay fairly stable there, but comprehensive is where coastal drivers feel the pinch.

Four Things You Can Do This Week

Get on a telematics program. UBI enrollment hit 17% in NC in 2026. The people already doing it are capturing savings the rest of us aren’t. If your driving is clean, you’re leaving money out there.

Call an independent agent. Not a captive agent for one brand. An independent who shops across carriers. The 5% statewide average masked huge variation between companies — some filed much lighter 2026 increases than others. A good independent agent finds that spread.

Adjust your deductibles. The 50/100/50 liability floor is fixed — state law. But your comprehensive and collision deductibles aren’t. Moving from $500 to $1,000 on comprehensive can offset a real chunk of the premium increase, as long as you’ve got the savings cushion to back it.

Fix your mileage number. Working from home? Still showing 15,000 annual miles on your policy? That’s somebody else’s risk profile. Update it. Takes five minutes. Shows up in your rate almost immediately.

Who Should Call Who

No single “best car insurance in North Carolina” fits every driver. But here’s my honest read:

Clean record, tight budget — State Farm or Progressive, compare both. Got a ticket — Progressive, hands down, because of how they handle imperfect records. New teen driver — State Farm. Use the programs. Want the best claims experience — Erie. Pay the extra. Sleep better. Low mileage, remote worker — Nationwide SmartRide. Military or veteran — USAA. First call, full stop.

And shop every year. Not every three years when you remember to. Every year. The gap between cheapest and most expensive carrier for the same NC driver can hit 20% or more. In 2026, with rates already climbing, that gap is worth hunting.

Frequently Asked Questions – FAQ’s

- What are the minimum car insurance requirements in North Carolina?

The minimum coverage is 50/100/50: $50,000 bodily injury per person, $100,000 per accident, and $50,000 property damage. - What happens if I drive without insurance in North Carolina?

You may face fines, registration suspension, and plate revocation. Proof of insurance and fees are required for reinstatement. - Does North Carolina require uninsured motorist coverage?

Yes, uninsured and underinsured motorist coverage is mandatory for all policies issued or renewed after July 2025. - How does North Carolina’s at-fault system work?

The at-fault driver is responsible for damages. Their liability coverage pays up to policy limits, and uninsured/underinsured coverage protects you if they lack sufficient insurance. - Why did my car insurance premium increase in 2026?

Premiums rose due to higher liability limits, increased repair costs, and regulatory changes like extended surcharge periods. - Can I use telematics to lower my car insurance in North Carolina?

Yes, programs like SmartRide and Drive Safe & Save reward safe driving habits with discounts of up to 40%. - How long do accidents and violations affect my premium?

Serious violations impact premiums for up to five years, while minor infractions typically last three to five years. - What discounts are available for car insurance in North Carolina?

Discounts include safe driver, multi-policy, telematics, and advanced safety features. Check with your insurer for eligibility. - Can I register a car in North Carolina without insurance?

No, proof of insurance is required to register and maintain vehicle registration. - What should I do if my car insurance claim is denied?

Insurers must provide a reason for denial. You can appeal using the appraisal provision or seek assistance from the NC Department of Insurance.

All rates and details reference 2026 market data and legislative changes that took effect July 1, 2025. Confirm current minimums and coverage terms with a licensed North Carolina insurance professional or the NC Department of Insurance before making any policy changes.