Last Updated: April 2026

A few links here are affiliate links. Small commission if you click through — zero extra cost to you, doesn’t change anything I say.

Marcus moved into his first Columbus apartment last fall. Signed the lease, bought a secondhand couch, called it done.

Three weeks later his landlord emailed. Renters insurance required. Proof within 30 days.

He panicked. Assumed it meant $80 a month — money he didn’t have. Spent a weekend on hold with carriers, running quotes, texting his one friend who actually understood cheap renters insurance stuff.

Final policy: $11 a month. Laptop, TV, clothes, $100,000 in liability. Done.

The panic was the problem. Not the price.

Most renters either overpay or go without because they never ran a real comparison. This piece does it for you. Here’s who’s cheapest in 2026, what the coverage does, and where things quietly go wrong.

Before You Compare Prices, Know What You’re Actually Buying

A standard renters policy — technically called an HO-4 — bundles three things. Worth understanding before the quotes, because people who buy the cheapest option without reading it tend to discover the gaps at the worst possible moment.

Personal property coverage is the core of it. Your stuff — laptop, TV, clothes, bike, furniture — gets reimbursed if it’s stolen, burned, burst-pipe-soaked, or wind-wrecked. 16 named perils. That specific list is what defines the coverage. Cause of your damage isn’t on it? Claim denied.

Liability coverage handles the situation where someone faceplants on your floor and their family hires a lawyer, or you accidentally flood your downstairs neighbor’s unit. Legal costs, damages, up to your policy limit. Starts at $100,000 on most cheap renters insurance. Worth bumping to $300,000 — usually a dollar or two more a month. Do it.

Loss of use — also called additional living expenses — pays hotel bills and food costs if a covered event makes the apartment unlivable. Your place catches fire Tuesday night, you’re not sleeping in your car Wednesday. This typically runs 10% to 30% of your personal property limit.

Standard policies don’t cover flooding from outside. They don’t cover earthquakes. They don’t cover your roommate’s stuff unless you name them specifically. Those require separate products.

What Cheap Renters Insurance Actually Costs

National average sits at $15 to $23 a month. For $20,000 in personal property with $100,000 liability, you’re often under $120 a year. But those averages are almost meaningless because the swings by location are massive.

State Farm in Alaska starts at $13. Alabama starts at $18. Detroit averages $79. Jackson, Mississippi: $43. Delaware: $15. Same coverage, different zip code, sometimes three times the price. Your insurer isn’t looking at state averages anymore — they’re pricing your specific neighborhood, your specific block’s crime history, how close you are to a fire hydrant.

Credit score is the second biggest pricing factor and the one people find most aggravating. In 47 states, poor credit can push renters insurance up by 76% or more. Genuinely unfair. Still legal. Still how it works.

Deductible is the lever you actually control. Jumping from $500 to $1,000 cuts your annual premium by 10% to 20%. That math only makes sense if you’ve got $1,000 sitting around when something goes wrong. If you don’t, a higher deductible is a trap, not a deal.

One more thing most people don’t think about until it bites them: claims history. One claim in the last five years bumps rates at most carriers. Two claims and some won’t renew you at all. If the repair is close to your deductible anyway, paying out of pocket and keeping your record clean is often the smarter move.

The Cheapest Companies in 2026 — What the Data Actually Shows

Amica — $9/Month

Cheapest national option in 2026. $9 a month for $20,000 in property coverage with $100,000 liability — $107 annually. But here’s the thing about Amica that gets overlooked: they also earned the highest J.D. Power customer satisfaction score of any major carrier this year. Cheapest and best-rated at the same time doesn’t happen often.

They’re also genuinely forgiving if your credit is rough. Around $15/month for poor-credit applicants versus $20-plus at most competitors. Had a prior claim? Amica post-claim averages $118 a year. Nobody else in the cheap renters insurance bracket comes close on that number.

Catch: not available everywhere. Check your state before you build your whole comparison around them.

State Farm — $14/Month

Most affordable option in 31 states. 19,000-plus local agents if you want to sit across from a human. Claims-free discounts that compound if you stay lucky.

Their bundling discount is only 17% — lower than Allstate and Liberty Mutual. But their base rates are competitive enough that the bundled total usually wins anyway. Best pick for anyone who wants low cost and a real local agent they can actually reach.

Lemonade — $5 to Start, $16 Average

Built from scratch around the idea that insurance should feel like an app, not a phone tree. Quotes in 90 seconds. Straightforward claims — stolen bike, water-damaged laptop — sometimes paid out in under 30 seconds. Not an exaggeration.

The $5 starting price is real but gets you bare minimum. Average policy runs $16. Cheapest in 15 states and D.C. Add-ons most carriers don’t offer: mold coverage, pet damage, identity theft.

Where it breaks down: 31 states only. Claims above $10,000 hit a handoff point where the AI passes to a human team and resolution stretches to 7–14 days. No physical agents anywhere. If you’re 24, hate phone calls, live in a covered state, and your claim is uncomplicated — Lemonade is hard to beat. If your life is messy, know where its ceiling is.

USAA — $15/Month, Military and Families Only

If you or an immediate family member served, stop reading the other options and price USAA first.

Average $15 a month. But the real edge is what they include as standard: flood and earthquake coverage. Every other carrier makes you buy those separately or skip them entirely. In high-risk areas, that hidden value runs hundreds of dollars a year. USAA is the only carrier in the cheap renters insurance conversation where “cheapest” and “most complete” are the same answer.

Liberty Mutual — Around $30/Month

Pricier as a standalone. The reason to consider them: 25% bundling discount, highest among major carriers. If you’re pricing renters and auto together, run the Liberty Mutual bundled number before crossing them off. The combined total sometimes beats cheaper individual policies from other carriers.

Allstate — $23 to $28/Month

Not the first call for pure price comparison. But solid financial ratings, up to 25% bundling, and better customization options than budget-only carriers. If you’re already an Allstate auto customer, the bundled renters rate is worth checking.

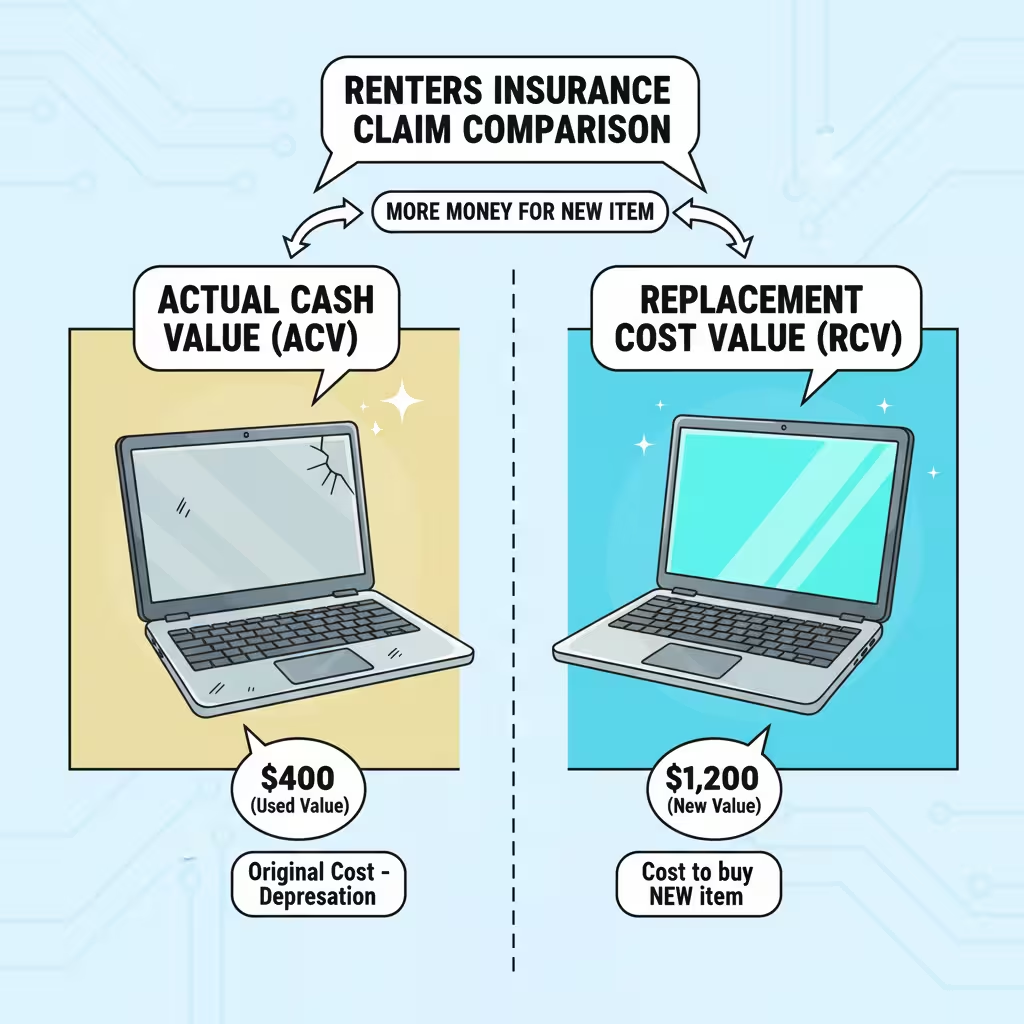

ACV vs. Replacement Cost — This One Question Changes Everything

Most people buy a policy without asking this. Then they file a claim and find out the difference the hard way.

Actual Cash Value pays what your stuff is worth today — after depreciation. MacBook you bought three years ago for $1,400? ACV check might be $550. The insurer doesn’t care what you paid. They care what a used, three-year-old MacBook is worth on the secondhand market. That’s the number.

Replacement Cost pays what it costs to buy the same item new right now. Same laptop, same loss — maybe $1,300 instead of $550.

ACV policies cost less per month. Replacement cost costs more. For anyone with electronics, decent furniture, or anything worth properly replacing — the extra monthly cost is not a hard decision. Ask your carrier specifically which valuation method your policy uses before you finalize anything. Don’t assume. Ask.

College Students — Read This Before You Pay for Anything

Living in a campus dorm? Check your parents’ homeowners policy before buying renters insurance. Students in on-campus housing are often already covered under the family policy for personal property. You might have it and not know.

Off-campus apartment changes that. Coverage usually doesn’t extend. You need your own, and with Lemonade at $5 and Amica at $9, this shouldn’t be a budget fight. We’re talking about protection for a laptop and a semester of textbooks.

The thing college students skip most: liability coverage. A friend hurts themselves in your apartment, their family sues. It’s happened. The $100,000 liability on a basic renters policy costs almost nothing and exists for exactly this. Don’t waive it to save $2.

Dog Owners — Ask One Question Before You Buy

Renters insurance liability coverage usually covers dog bites. The complication is breed.

Pit Bulls, Rottweilers, German Shepherds, Dobermans, Akitas — a lot of carriers either surcharge these breeds significantly or exclude dog bite liability outright. You won’t find this in the headline rate. You find it when you file a claim.

Ask every carrier before you commit: does my dog’s specific breed affect my liability coverage? Write down the answer. State Farm and Nationwide are generally more flexible than most on this. Lemonade offers a pet damage add-on. If your dog is the complicating factor, start your quote there.

Under $10 a Month — What’s Real and What Isn’t

Amica at $9 is the real answer here. Not a teaser rate. Not a first-month promotional price. But it applies to lower coverage limits in lower-risk areas. Your actual ZIP code, credit score, and coverage needs determine whether that number applies to you — not a headline on a comparison site.

Lemonade at $5 also exists. 31 states only. And $5 a month gets you bare minimum coverage. Not nothing, but not enough for someone with $15,000 worth of stuff in their apartment.

Honest take: hunting for the lowest possible number is the wrong goal. Cheap renters insurance that doesn’t actually cover what you’d lose isn’t cheap — it’s a monthly fee for a false sense of security. For most renters, $11 to $16 gets real coverage. The sub-$10 options can work, but require a real quote against your actual situation to find out.

Bundling — Fastest Way to Drop the Total Bill

Own a car? Renters plus auto from the same carrier cuts the bill significantly.

Allstate, Geico, Liberty Mutual, and American Family all advertise up to 25% off bundled policies. Progressive averages $750 in annual savings for switchers who combine. State Farm’s 17% bundling is lower — but their base rates are cheap enough that the bundled total often wins anyway.

Price renters and auto together at every carrier you quote. Never get them as separate quotes from the same company — the bundled number is always lower. This one habit, applied consistently, can close the gap between the cheapest standalone and the best overall deal.

Frequently Asked Questions – FAQ’s

What’s actually the cheapest renters insurance in 2026?

Amica at $9/month nationally. Lemonade at $5 in 31 states. State Farm around $14, available in the most locations. None of those numbers apply to you automatically — your real rate depends on ZIP code, credit history, deductible choice, and coverage limit. Run actual quotes, don’t trust headline numbers.

Do I legally have to have renters insurance?

No. No federal law requires it. But landlords can — and many do, especially in newer buildings and larger complexes. Showing up to sign a lease without proof of coverage delays your move-in. And protecting $15,000 or $20,000 worth of belongings for $15 a month is just arithmetic.

What does cheap renters insurance actually not cover?

Flooding from outside your unit — storm surge, groundwater, overflowing rivers. Earthquakes. Your roommate’s stuff. Your car. Business equipment if you freelance from home. Every one of those needs a separate product or endorsement.

Does it cover theft that happens outside my apartment?

Typically yes, up to a cap — usually 10% of your total personal property limit. Laptop stolen at a library, bag grabbed from your car — generally covered. Look up the specific cap in your policy before assuming you’re covered for the full value.

ACV or replacement cost — which one?

Replacement cost. Always, if you can afford the slightly higher premium. ACV on a three-year-old laptop pays you secondhand market value — maybe $550 on a $1,300 item. Replacement cost pays what it costs to actually replace it. The monthly difference is usually a few dollars. The claim difference can be hundreds.

Does standard renters insurance cover dog bites?

Liability coverage usually includes dog bites, yes. The catch is breed-specific exclusions — Pit Bulls, Rottweilers, German Shepherds, Dobermans, and Akitas are flagged by a lot of carriers. Find this out before you buy. Discovering the exclusion after a bite claim is expensive and avoidable.

Marcus, Six Months Later

He set up autopay the same day he got the policy. Sent proof of insurance to his landlord that afternoon. Hasn’t thought about it once since — except for the one time someone cut his bike lock off a rack outside his building and walked away with it.

Filed the claim on his phone while standing on the sidewalk outside the building, annoyed, staring at where the bike used to be. Check hit his account two days later.

Not dramatic. Not complicated. The product just worked.

Fifteen minutes of comparison. Three quotes. One question about ACV versus replacement cost. That’s the whole process. The policy you end up with won’t feel like an important purchase — it’ll feel like a boring line item right up until the moment you actually need it.

Marcus would tell you $11 a month was the easiest decision he made all year.

About the Author Written by a financial content team covering personal insurance, residential property, and US consumer protection. Research draws from 2026 J.D. Power U.S. Property Claims Satisfaction Study data, AM Best carrier ratings, Amica and Lemonade published rate data, and national premium benchmarks from the Insurance Information Institute.

Disclaimer: Premium estimates and carrier details reflect publicly available information as of April 2026. Rates vary by state, ZIP code, and individual risk profile. Always get a direct quote from the carrier before making a coverage decision.