Last Updated: March 2026

Two Tuesdays ago, a guy in my networking group — runs a four-person bookkeeping firm outside Nashville — told me he skips cyber insurance because “we’re not big enough for anyone to bother with.”

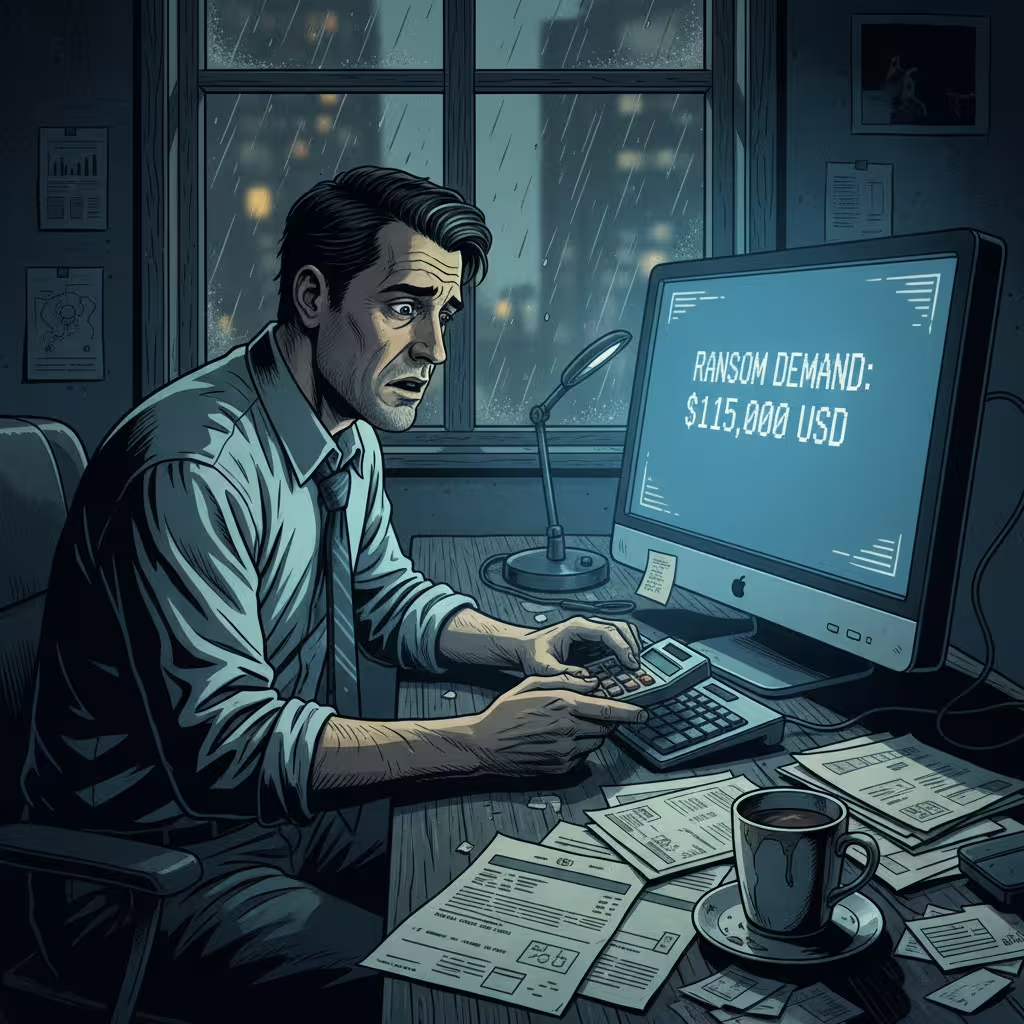

I didn’t push back. But I kept thinking about the flooring company owner I know who said the same thing. Right up until his systems locked on a Monday morning and someone wanted $80,000 to hand them back.

Paid $47,000 after negotiating. No Cyber liability insurance. Sold his work truck.

That’s the whole thing, honestly. But let me give you the full picture.

The “Too Small to Hack” Thing Is a Trap

Nobody’s picking your business by hand. That’s not how this works anymore.

Criminals run software. Automated tools crawling millions of IP addresses, 24 hours a day, flagging anything weak. No MFA on your login? Flagged. Software three years out of date? Flagged. Same password on your admin account since 2019? You’re already in a queue somewhere.

Your revenue is invisible to those tools. Your headcount means nothing. What shows up is whether your door is unlocked.

Small businesses have unlocked doors constantly — not out of laziness, but because there’s no IT person whose only job is to watch for this stuff. You’re doing payroll, managing vendors, handling customers. Nobody’s checking your firewall logs at 2 a.m. on a Wednesday.

Gallagher’s 2026 market data shows 88% of small business breaches involve ransomware. Median demand hitting these businesses: $115,000. That number would wipe out most of the business owners I know. And that’s before forensics, legal fees, customer notifications, and weeks of lost revenue start stacking on top.

So What Does Cyber Liability Insurance for Small Businesses Actually Cover

Insurance people love to make this sound complicated. It’s not.

Two buckets.

Bucket one: your own losses. Everything that hits your business directly.

Ransom negotiations — so you’re not Googling “how to buy Bitcoin” at midnight. A forensics team to figure out how they got in and what they grabbed. The revenue you didn’t make while your systems were dark. Legal notifications to every customer whose data got exposed — required by law, costs $160 to $168 per person. PR help if this ends up on the local news and your reputation takes the hit.

Bucket two: what you owe other people. Because your breach becomes their problem too.

When a customer’s payment info gets stolen from your system, they can sue. When a state agency decides your security was negligent, they can fine you. And then there’s the one that really blindsides people — privacy lawsuits that have nothing to do with a hack at all.

CIPA. California Invasion of Privacy Act. A 1967 wiretapping law lawyers are now swinging at businesses over website cookies, tracking pixels, session replay tools. No breach needed. Just having standard tracking code running on your site. Penalties between $250 and $10,000. Per user. Per violation. You do that math yourself.

Here’s the Thing That Actually Closes Businesses

Everyone talks about stolen data. The thing that ends companies is the shutdown.

When ransomware locks your systems, nothing works. No transactions, no records, no orders. Restaurant, retail, medical office, service shop — doesn’t matter. Revenue stops the second your systems go offline. Then the clock runs.

Business interruption losses — the money you’re not making while you’re down — run on average 650% higher than incidents where the business stays operational. Not 65%. Six hundred and fifty. Average BI loss for small businesses crossed $1 million in 2025. Year before it was $611,000.

Ransomware triggers 81% of those shutdowns.

And modern ransomware doesn’t just lock files. That was the old version. Now they steal the data first — your customer records, your employee files, your financial data — then they lock everything. So even if you’ve got backups, they’ve still got your customers’ information and they’re threatening to dump it publicly unless you pay. Double extortion. Pay to unlock your systems AND to keep your data off the internet. Two separate levers.

No coverage? You’re making that call alone.

What It Actually Costs

$1,500 a year for most small e-commerce shops. Around $1,800 for software businesses. Most other small businesses somewhere in that range. That’s from Gallagher’s 2026 pricing data.

$125 to $150 a month.

Compare that to $115,000 in ransom. Or $1 million gone while your business sits offline. Or $160 times however many customer records are sitting in your system right now.

I’m not dressing that up. The math isn’t interesting. It’s just lopsided.

Getting a Policy in 2026 Takes More Than a Credit Card

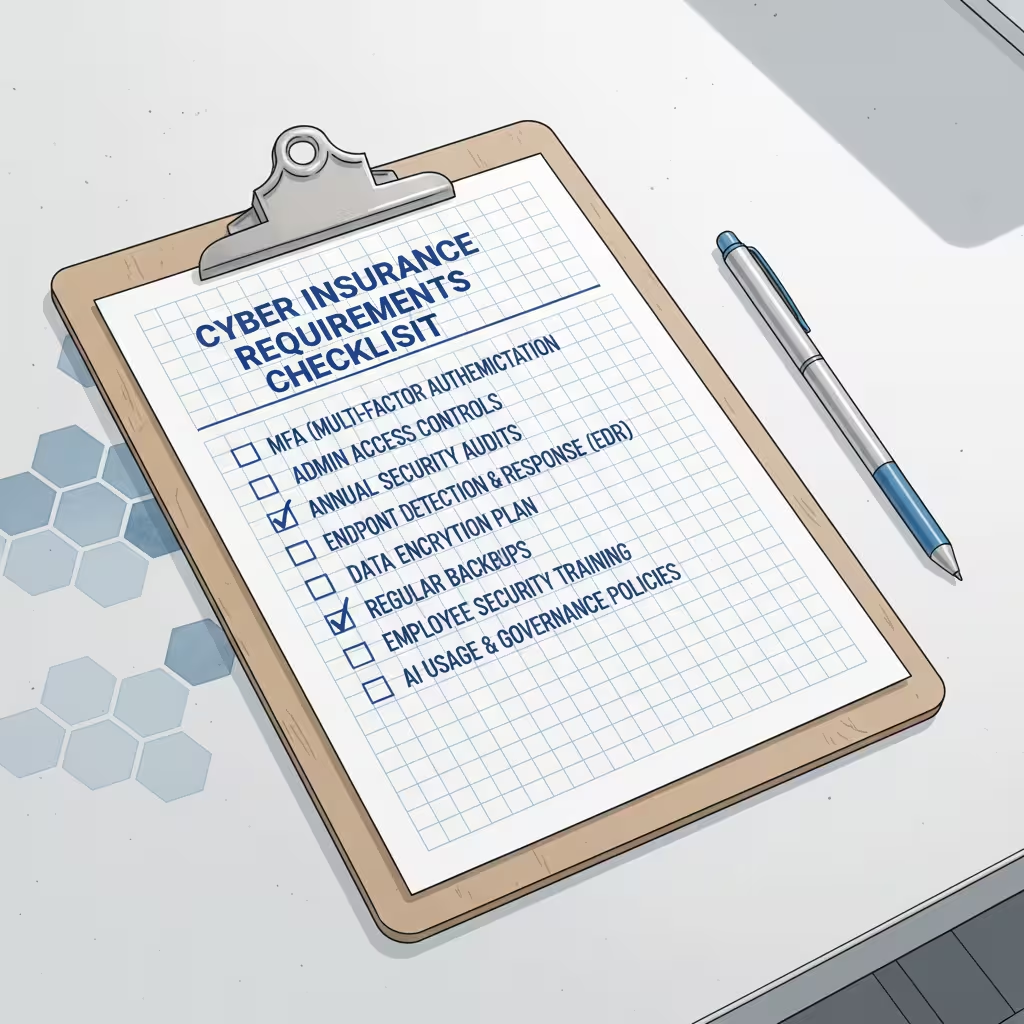

Insurers got hammered on claims the last few years. Businesses with basically zero security controls filing six-figure claims. So now there’s a checklist. Non-negotiables before they’ll write you a policy.

Multi-factor authentication. Every remote login — email, accounting software, your POS, anything accessed outside the office — needs more than a password. Carriers have cited missing MFA in 35% of denied claims. It’s free on most platforms. Not a negotiation point anymore.

Locked-down admin access. Your front desk person doesn’t need the same system permissions as whoever manages your server. Giving everyone admin rights because it’s easier is the kind of thing that turns a minor incident into a full breach. Insurers call it privileged access management. Call it whatever you want, just set it up.

A real annual security audit. California’s updated CCPA rules that kicked in January 2026 now require formal cybersecurity risk assessments for businesses with California customers. Insurers want to see it documented. Doesn’t have to be a massive production — a proper third-party assessment once a year handles it for most small businesses.

Something written about AI. This one catches people off guard. If anyone on your team uses ChatGPT, Copilot, anything — for work tasks — and they paste client data into it, your insurer might call that uncovered negligence when the claim comes in. Two pages of policy. “Approved tools only. No client or customer data in public AI tools.” That’s genuinely most of what you need.

The AI Exclusion Nobody Mentioned When You Bought Your Last Policy

Insurers are rewriting language right now to cut out what they’ve started calling “silent AI” coverage. Incidents that used to slide under standard cyber policy language are getting their own explicit carve-outs.

Three to know:

Deepfake fraud. Someone calls your bookkeeper or your operations manager. Sounds exactly like your voice — same rhythm, same word choices. Says there’s an urgent wire transfer, $55,000 to a vendor, needs to happen today. She sends it. AI voice cloning in 2026 is good enough that people who know you well can’t reliably catch it. And whether that wire transfer counts as a “direct computer crime loss” under your policy is actively being fought in courts. Some carriers are paying. Some aren’t.

Unauthorized AI use. Employee uses a free public AI tool for a work task and pastes in client data. It leaks. Insurer pulls the policy, sees no written AI governance on file, calls it uncovered employee negligence. Claim denied.

Prompt injection. If your business uses any AI chatbot or automation tool facing customers or vendors, attackers can craft inputs that make the tool behave in ways it shouldn’t — exposing data, taking actions outside its intended scope. Niche for most small businesses today. But it’s in the exclusion language already.

Before your next renewal: ask your broker exactly what the policy says about AI incidents. Get it in writing.

The $5 Million Claim That Got Denied

- City of Hamilton. Ransomware attack. Recovery bill: $5 million.

Insurer denied the claim. All of it.

Why? The city hadn’t finished rolling out multi-factor authentication. Investigation found that gap was the root cause of how attackers got in. Policy voided. Five million dollars, absorbed by the municipality.

A city with a legal department, a risk team, and IT staff. Denied. Over a checkbox.

If you’re assuming your cyber policy pays out regardless of what controls you had running — that story should give you pause. These are contracts. They have conditions. The controls aren’t optional extras you implement later when you get around to it. They’re what makes the policy valid when you need it.

Premiums Are Down. Coverage Is Too. Read the Fine Print.

Cyber insurance premiums dropped roughly 7% in late 2025. More competition, more capacity, buyer-friendly market. Sounds straightforwardly good.

It mostly is. But carriers are simultaneously shrinking what they’ll pay for. Systemic outage coverage — narrowed. State-sponsored attack coverage — excluded or sub-limited. AI incidents — carved out. You might renew this year for less money and end up with a policy that covers less than the one you had in 2023.

Industry people call it the soft market paradox. The price looks better. The product quietly isn’t.

Don’t choose on premium alone. Sit with your broker and go through what’s excluded, line by line. Out loud.

And if you’re uninsured right now — uninsured small businesses are seeing a 48% higher ransomware rate than insured ones. Because getting insured forced those businesses to implement actual controls. The uninsured ones skipped that process entirely.

The controls are the protection. The policy is what’s there when the controls fall short.

Questions People Actually Ask About Cyber Liability Insurance Policy

How much does cyber liability insurance for small businesses run in 2026? Most pay $1,500 to $1,800 a year. Healthcare, financial services, and e-commerce businesses land toward the top of that. What you pay depends on revenue, what kind of data you hold, and whether your security controls are actually in place.

What won’t a cyber policy cover? Right now: AI-related incidents where there’s no written AI policy, state-sponsored attacks, major cloud outages causing systemic disruption. Read the exclusions before you sign. Don’t skim them.

Am I seriously a target if I’m small? The scanning tools don’t know you’re small. They know your software is unpatched or your login has no MFA. That’s the whole criteria.

First-party vs. third-party — what’s the difference? First-party is your losses — the ransom negotiation, the forensics bill, the revenue you didn’t make while you were down, the notification letters. Third-party is what you owe everyone else — customer lawsuits, regulatory fines, privacy violation claims.

No MFA, no policy? Getting there. Some carriers flat-out won’t quote you. Others will but at higher premiums with reduced limits. MFA is in 35% of denied claims as a factor. Just set it up.

What is CIPA and why does it matter to my business? It’s a California wiretapping law from 1967 that lawyers are using to sue businesses over tracking pixels and website cookies today. No hack required. If California users hit your website and you’ve got tracking code running, the liability is real. Penalties hit $10,000 per violation.

What is double extortion? They steal your data, then they lock it. You restore from backups — great. They still have your customer records and they’re threatening to post them. Two separate demands. Having backups doesn’t make this go away.

What is cyber liability insurance? It protects businesses from financial losses due to cyberattacks, data breaches, and privacy violations.

Why do small businesses need cyber insurance? Small businesses are frequent targets of automated cyberattacks due to weak security controls, making insurance essential.

What does cyber liability insurance cover?

It covers ransom negotiations, forensics, business interruption losses, legal notifications, and third-party liabilities.

What is double extortion in ransomware attacks? Attackers steal data and lock systems, demanding payment to unlock systems and prevent data leaks.

How much does cyber liability insurance cost in 2026?

Most small businesses pay $1,500–$1,800 annually, depending on industry and security measures.

What are common exclusions in cyber insurance policies?

Exclusions include AI-related incidents, state-sponsored attacks, and systemic cloud outages.

What is the role of MFA in cyber insurance?

Multi-factor authentication (MFA) is often mandatory for coverage and prevents many breaches.

What is the California Invasion of Privacy Act (CIPA)?

CIPA is a law targeting businesses for privacy violations like tracking cookies, with penalties up to $10,000 per user.

What happens if a business lacks cyber insurance?

Without coverage, businesses face full financial responsibility for ransom payments, legal fees, and lost revenue.

What should businesses check in their cyber insurance policy?

Review exclusions, AI-related clauses, and ensure compliance with security requirements like MFA and audits.

That bookkeeper from my networking group — the one who said nobody would bother with him — sent me a message nine days ago. His email account got hijacked. Whoever had it sent fake invoices to three of his clients. Two paid. $22,000 gone. He’s lawyering up now.

He had no cyber coverage.

His actual question to me was: who do I call to get a policy right now.

Don’t get there by that road. It’s a bad road.

This article is for general information only. It’s not legal, financial, or insurance advice. Coverage terms, pricing, and eligibility change by state, insurer, and business type. Work with a licensed broker for guidance that applies to your actual situation.

Sources: Gallagher 2026 Cyber and Technology State of the Market Report · IBM-Ponemon Cost of a Data Breach Report 2025 · FBI Internet Crime Complaint Center Annual Report · Chainalysis 2025 Ransomware Report