Last Updated: April 2026

Quick note: A couple links here are affiliate links. I earn a small cut if you buy — costs you nothing extra, changes nothing I recommend.

My neighbor Greg called me on a Sunday afternoon, voice cracking a little.

Pipe burst in his basement. Water everywhere. He’d already started mopping. What he really wanted to know — and I could hear the dread sitting underneath that question — was does, home insurance cover water damages.

I told him it probably would. Burst pipe from a sudden failure? That’s usually covered.

Then I asked him one thing: “How old was the pipe?”

Long pause.

“I think it was original to the house,” he said. “1987.”

That changed everything. By end of that week, Greg had a denied claim and a $6,200 repair bill he hadn’t planned on and hadn’t saved for.

Look — does homeowners insurance cover water damage is technically the right question. But it’s also kind of the wrong one. What really matters is which kind of water damage, from where, caused by what. Because those three things swing the answer from “fully covered” to “completely on you” — and the gap between those two outcomes can be enormous.

Here’s what I’ve pieced together about how this actually works.

The One Rule That Controls All of This

I’ll say it plainly: everything in water damage coverage hinges on one thing.

Fast damage — yes. Slow damage — no.

If water flooded your space suddenly (burst pipe, appliance blowout, storm tearing open your roof), your homeowners policy almost certainly covers it. If water seeped, dripped, or crept in over weeks or months (slow leak behind drywall, corroded pipe weeping into insulation, shower pan that’s been soft for two years), your policy almost certainly doesn’t. That’s a maintenance issue. Your insurer will call it negligence, write it up that way, and send you a denial letter that feels polite and is completely final.

That’s what hit Greg. His pipe didn’t fail the way a healthy pipe fails. It had been corroding since probably the late 2000s. The inspector found rust deposits, old staining, mineral buildup — signs of slow moisture intrusion that predated Greg’s ownership of the place. Gradual damage. Not covered.

That one distinction — sudden and accidental versus gradual and foreseeable — is the foundation every water claim is built on. Every other thing I’m going to tell you flows from it.

Burst Pipes and Frozen Lines — the Covered Scenarios (With Traps)

Does homeowners insurance cover a burst pipe? Most of the time, yes. But “most of the time” has real edges you should know about.

Pipe blows out overnight from a hard freeze? Covered. Appliance hose snaps mid-cycle and drowns your laundry room? Covered. Water heater gives out without warning and puddles across your utility floor? Covered.

Here’s where the freeze scenario gets complicated though. If your pipes froze because you left for a two-week trip and turned the heat way down to save on your gas bill — a lot of carriers will fight that claim. Hard. Most policies have language requiring you to maintain reasonable temperatures in the home. Left it unattended in January with the heat at 45 degrees? That’s the kind of detail adjusters are trained to ask about. It’s ammunition for a denial.

Vacation properties and rental homes run into this constantly. Owners cut utilities between stays. A cold snap hits. Pipes burst. They file the claim expecting standard coverage. What they get instead is a letter citing the vacancy clause and maintenance obligations.

My take on this, for what it’s worth: if you own a second property anywhere that gets real winters, keep the heat at 55 minimum and have someone physically checking the place every week or two. That paper trail — documented evidence that the property was being maintained — is often what decides whether a freeze claim survives adjuster scrutiny or dies in review.

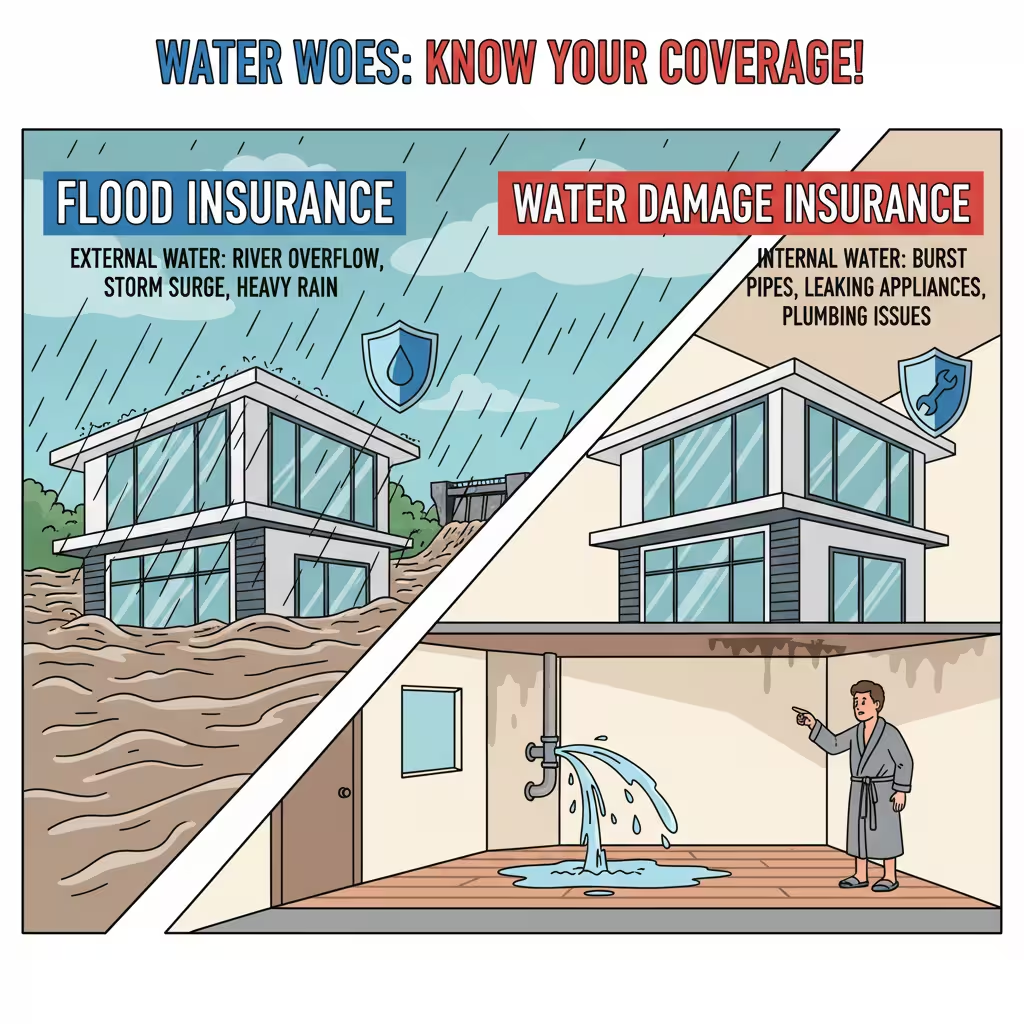

Flood vs. Water Damage Insurance

This is the most expensive mix-up in residential insurance. I’m not exaggerating that.

Home insurance water leak coverage handles water that starts inside your home. Pipe failure. Appliance overflow. Storm rips a hole in your roof and rain pours through. Bathtub overflow. Your standard homeowners policy was designed for those scenarios.

Flooding is a different animal entirely.

Water that rises from outside — storm surge, an overflowing river, rain that sheets off saturated ground and pushes into your basement — is excluded from every standard homeowners policy. Not limited. Not partially covered. Excluded. Flat. Doesn’t matter how long you’ve had the policy, how much you pay, how good your carrier is. External rising water is not in the contract.

Flood insurance is its own separate product. Most of it runs through FEMA’s National Flood Insurance Program, though private flood carriers have grown fast and now cover well over a million properties.

I’ve watched homeowners argue with their insurers after major storms about this and lose every single time. The exclusion clause on flood has no wiggle room. It was written to be categorical, and it is.

So — does your address land in or near a FEMA flood zone designation? Check the FEMA flood maps at msc.fema.gov. Look up your exact address. It takes maybe five minutes. If you’re in a high-risk zone (Zone A or Zone V on the map), flood insurance isn’t just smart — it may be required by your mortgage lender. If you don’t have it and they find out, they can force-place their own flood policy on your loan and charge you for it at a much steeper price.

And don’t assume moderate-risk zones are safe. FEMA’s own data puts about 25% of flood claims coming from properties outside designated high-risk zones. Low-risk doesn’t mean no-risk. It just means cheaper premiums if you go ahead and buy the coverage.

Nobody Warns You About Sewer Backup

Until you’re ankle-deep in it.

Sewer backup — the city main surges, or your own drain line clogs, and raw sewage pushes back up through your floor drains — is not covered by a standard homeowners policy. It’s not classified as flood. It’s not a burst pipe. It’s its own specific peril, excluded by default.

The fix: a sewer backup rider. Some carriers call it a water backup endorsement. You add it onto your existing policy. Runs $40 to $120 a year, usually gets you $10,000 to $25,000 in coverage.

That is a very cheap fix for a very expensive problem. Sewage remediation isn’t regular water cleanup — it’s biohazard work. Professional crews, industrial equipment, sometimes complete demo of affected materials. Bills routinely hit five figures before you’ve started rebuilding anything.

If your home was built before 1980, or you’re in a neighborhood where the municipal pipes have been in the ground for decades, this endorsement is not optional. It’s just the cost of being covered for something that actually happens. Get it added.

Mold — the Coverage People Assume They Have

Short answer: mold coverage is narrow, conditional, and capped lower than most people realize.

A standard homeowners policy will cover mold removal if — and this is a specific if — the mold grew directly from a covered sudden water event. Pipe bursts, soaks your drywall, mold colonies show up within 72 hours. In that scenario, most carriers treat the remediation as part of the covered loss.

Mold from a slow leak? Excluded. You had a chance to find the leak and fix it. The mold is downstream of your own deferred maintenance. That’s how the denial letter reads, and it holds up.

Mold from flooding? Also excluded — because the flooding itself wasn’t covered to begin with.

Here’s the part that really stings: mold moves fast and hides well. It grows inside walls, under floors, behind tile. By the time you smell it or see it, it’s probably been spreading for a while. One room of mold remediation runs $3,000 to $8,000. A serious whole-house problem — the kind where it’s been going quietly for months — can run $30,000 or beyond.

And most standard policies cap mold coverage at $5,000 to $10,000. Even when they cover it at all.

I’d argue that if you’re in Florida, the Gulf Coast, the Pacific Northwest, or honestly anywhere that gets sustained humidity and wet weather, you need to have a direct conversation with your agent about what your mold cap actually is. Some carriers offer a mold endorsement that raises or removes that cap entirely. Ask for it. A $5,000 ceiling on a $22,000 remediation job is not coverage — it’s a partial reimbursement.

The Add-Ons That Fill the Gaps

Your standard policy has holes. These four close the ones that actually matter.

Sewer backup rider — $40 to $120 a year. Covers sewage and drain overflow your standard policy won’t touch. I already said this above and I’ll say it again: not having this is a decision you’ll regret exactly once, in the worst possible circumstances.

Service line coverage — different from the sewer rider. This one covers the underground pipes running between your house and the street — water supply lines, sewer laterals. Tree roots. Corrosion. Ground shifting. When one of these fails, the repair runs $5,000 to $12,000 and your standard policy doesn’t touch it. This endorsement costs $30 to $80 a year.

Mold endorsement — not every carrier has this, but ask directly. If yours does and you live somewhere with real humidity, add it. The default cap on mold remediation coverage in most standard policies is genuinely inadequate for serious cases.

Separate flood insurance — this isn’t an endorsement. It’s its own policy, through NFIP or a private carrier. If you’re in any FEMA flood zone designation, stop reading this and go price it. If you’re near water and not technically in a flood zone, consider it anyway. Flood damage without flood insurance is a financial event that wipes people out completely.

Frequently Asked Questions – FAQ’s

Does homeowners insurance cover water damage from a burst pipe?

Usually yes, with conditions. The burst needs to be sudden and accidental, and the home needs to show signs of reasonable maintenance. Before you touch anything — document everything. Photos, video, timestamps, written notes about when you first noticed any signs of moisture. That timeline becomes the core of your claim. If the pipe was old, visibly corroded, or showing prior damage, the adjuster will look hard at whether this was really “sudden” or just the eventual failure of a neglected system.

What’s the difference between flood and water damage insurance?

They’re two completely separate products, and mixing them up is one of the most expensive mistakes homeowners make. Water damage — from a pipe, appliance, or storm breach from above — is covered under a standard homeowners policy. Flood damage — from any external rising water source — is excluded from every standard homeowners policy and requires its own standalone flood insurance policy. One does not cover what the other misses. They don’t overlap at all.

Is mold removal covered by home insurance?

Only if the mold traces directly back to a covered sudden water event. Mold from slow leaks, from flooding, or from humidity and deferred maintenance is excluded. And even in the cases where it is covered, most standard policies cap the payout at $5,000 to $10,000 — which doesn’t go far when a serious remediation job runs $15,000 to $30,000. Check your cap before you have a problem, not after.

What is a sewer backup rider and do I need one?

It’s an endorsement — usually called a water backup endorsement — that covers sewage and drain overflow that standard policies exclude. Costs $40 to $120 per year depending on your carrier and coverage limit. If you’re in a home older than 1980, or in any neighborhood where the municipal infrastructure has seen better days, this one is not optional. The cost of sewage remediation without it is brutal.

How do FEMA flood maps affect my coverage?

They determine your official flood risk designation, which directly affects whether flood insurance is required by your mortgage lender. High-risk zones (Zone A or V) trigger mandatory requirements for federally backed loans. Moderate and low-risk zones don’t require it, but still experience regular flooding — about 25% of all flood claims come from outside high-risk zones. Check your property at msc.fema.gov. Maps update periodically, so a zone change could affect your requirements without warning.

Does homeowners insurance cover gradual water damage?

No. Full stop. Gradual leaks, slow seepage, and damage that accumulated over time fall under the maintenance exclusion in virtually every standard policy. Coverage only applies to sudden, accidental damage. This is the rule that catches the most homeowners off guard — especially in older homes where pipes and fixtures have been quietly failing in the walls for years before anything visible shows up.

What Greg Did Next

He paid the $6,200. It hurt. He didn’t have a great month after that.

But before the contractor even finished the repair, he called his agent and added a water backup rider. He ordered a four-pack of leak detectors off Amazon and stuck one behind the washing machine, one under the kitchen sink, one near the water heater, one by the refrigerator. And he paid his plumber to run a camera through the rest of the original supply lines so he’d know what else was quietly corroding in the walls.

He also checked the FEMA flood maps for the first time in the eleven years he’d owned that house. Turned out his address sits in a moderate-risk zone. He hadn’t known. He’s pricing flood insurance now.

None of that gets him his $6,200 back. But the next claim goes differently.

Water damage is the single most common source of homeowners insurance claims in this country. Mold is expensive, hides well, and mostly excluded. Flooding — completely separate product, completely separate problem — ruins families financially every year specifically because people assumed their homeowners policy handled it.

Read your exclusion clause. Add the sewer backup rider. Pull your address on the FEMA map. Ask your agent what your mold cap is before you ever need to know.

The gap between “I thought I was covered” and “I’m actually covered” is exactly where the painful surprises live.

About the Author Written by a financial content team covering personal insurance, residential property claims, and US consumer protection. Research draws from the Insurance Information Institute, FEMA National Flood Insurance Program data, AM Best carrier ratings, and publicly available claims data from Verisk Analytics.

Disclaimer: Coverage terms, exclusions, and endorsement availability described here reflect publicly available information as of April 2026. Insurance products vary by state and carrier. Always consult a licensed insurance professional before making coverage decisions.