Let me tell you what happened to my friend Tony.

Tony does video editing. Freelance. Has for about five years now. Good clients, steady work, makes decent money. Last spring he called me out of nowhere asking if I knew anything about health insurance because his bill had just jumped from $240 a month to $510 and he had no idea why.

I asked him when he last actually read anything about his plan.

Long pause.

“When I signed up,” he said.

That is most freelancers. They sign up once, set up autopay, and never look at it again until something forces them to. Then they are stuck.

If you work for yourself in any capacity — freelance, consulting, 1099 contracts, gig work, you name it — finding the right health insurance for freelancers is genuinely one of the harder parts of the job. Not because it is complicated in theory. Because nobody explains it straight and there is a lot of money riding on the decisions you make.

I am going to try to fix that here. Everything I know about health insurance for self-employed people in 2026, written the way I would explain it to Tony over coffee.

Here is why Tony’s bill doubled and why yours probably did too.

From 2021 until the end of 2025, the government was quietly paying part of your Marketplace premium. It was called Enhanced Premium Tax Credits. Most people getting this help had no idea. The subsidy was applied automatically. Your bill just looked manageable.

It ended December 31, 2025. Nobody extended it.

A 40-year-old earning $50,000 went from about $220 a month to $550 or more. Same plan. Same network. Same everything except that invisible government contribution stopped coming.

That is roughly $3,960 more per year coming straight out of your pocket.

January 2026 enrollment numbers showed 14 percent fewer new sign-ups compared to the year before. People did not find better plans. A lot of them just stopped having insurance.

On top of that, a law called the One Big Beautiful Bill Act was signed on July 4, 2025. It changed several things about how the Marketplace works and who qualifies for help. The Congressional Budget Office figured the law could leave 10 million people without coverage by 2034. If the extra credits stay gone permanently, that number goes past 14 million.

So yes. 2026 is a genuinely rough year to be buying your own health coverage. But you still have real options. Let me walk through them.

The ACA Marketplace is where most of the health insurance for freelancers people should start. Healthcare.gov for most of the country. Covered California if you live in California. NY State of Health for New York. A handful of other states run their own exchanges too — if yours does, use that one instead of the federal site.

Plans come in four levels. Bronze, Silver, Gold, Platinum. I want to explain what these actually mean for your money rather than just list them.

Bronze costs the least each month but your deductible is high — somewhere in the six to nine thousand dollar range usually. You pay most of your own medical costs before insurance starts helping. If you are genuinely healthy and you maybe see a doctor once a year for a physical, Bronze can work. But one unexpected thing — a kidney stone, a broken bone, an infection that needs imaging — and you are paying thousands before your coverage does anything.

Something changed in 2026 that makes Bronze more interesting. All Bronze plans on the individual market are now HSA-eligible. I will explain what that means below and why it matters a lot for freelancers specifically.

Silver is the middle option. Not the cheapest, not the most expensive. But Silver is the only level that qualifies for something called Cost-Sharing Reductions. If your income falls under 250 percent of the federal poverty level, this extra benefit lowers your deductibles and out-of-pocket costs throughout the year — not just your monthly premium. The real value of a Silver plan with CSRs is hidden. It shows up when you actually use care.

Gold costs more per month but your costs are lower when you use it. If you take prescription medications regularly, see any kind of specialist, or have kids who actually visit doctors, Gold often costs less in total once you add everything across the year. Comparing only monthly premiums gives you a misleading picture every time.

Platinum is the most expensive monthly option. Lowest out-of-pocket costs. Small portion of the market. Usually only worth it for people expecting genuinely heavy medical use throughout the year.

Now. About subsidies in 2026.

Your subsidy eligibility is based on MAGI — Modified Adjusted Gross Income. For freelancers that is basically your net profit after you deduct business expenses. The lower your income relative to the poverty line, the more help you get.

Two changes under the new law hit 1099 workers specifically hard.

The repayment cap is gone. Before, if you enrolled estimating $45,000 income and actually made $60,000, there was a limit on how much subsidy you had to pay back. That limit no longer exists. You repay the full difference. No ceiling.

Freelance income moves around. Great months, slow months, one big project that lands in December and wrecks your estimate. If your income shifts significantly during the year, update it in the Marketplace. Log in and change your income estimate. Do not wait until April and discover you owe thousands.

Automatic re-enrollment is also dead now. Your plan does not carry over by itself anymore. You have to actively re-enroll every single year. Open enrollment runs November 1 through January 15 for most states. Miss it without a qualifying life event — marriage, a baby, losing other coverage — and you wait until the next year.

COBRA is something most people only think about the day they leave a job. I want you to understand it before that day comes.

If you had insurance through an employer and you leave — quit, get laid off, whatever — COBRA lets you stay on that exact plan for up to 18 months.

Same doctors. Same network. No interruptions to anything you have going on medically.

The problem is the price. Your employer was paying a big portion of your premium every month without you ever seeing it. On COBRA you pay all of it — their share, your share, and a 2 percent administrative fee tacked on.

People regularly go from $150 a month as an employee to $900 or more on COBRA for the exact same plan.

Use it as a bridge. Two or three months while you figure out a Marketplace plan. Or if you have surgery coming up and cannot afford to mess with your network right before it. Beyond that it is almost always cheaper to move to a Marketplace plan. Month six on COBRA is usually just throwing money away.

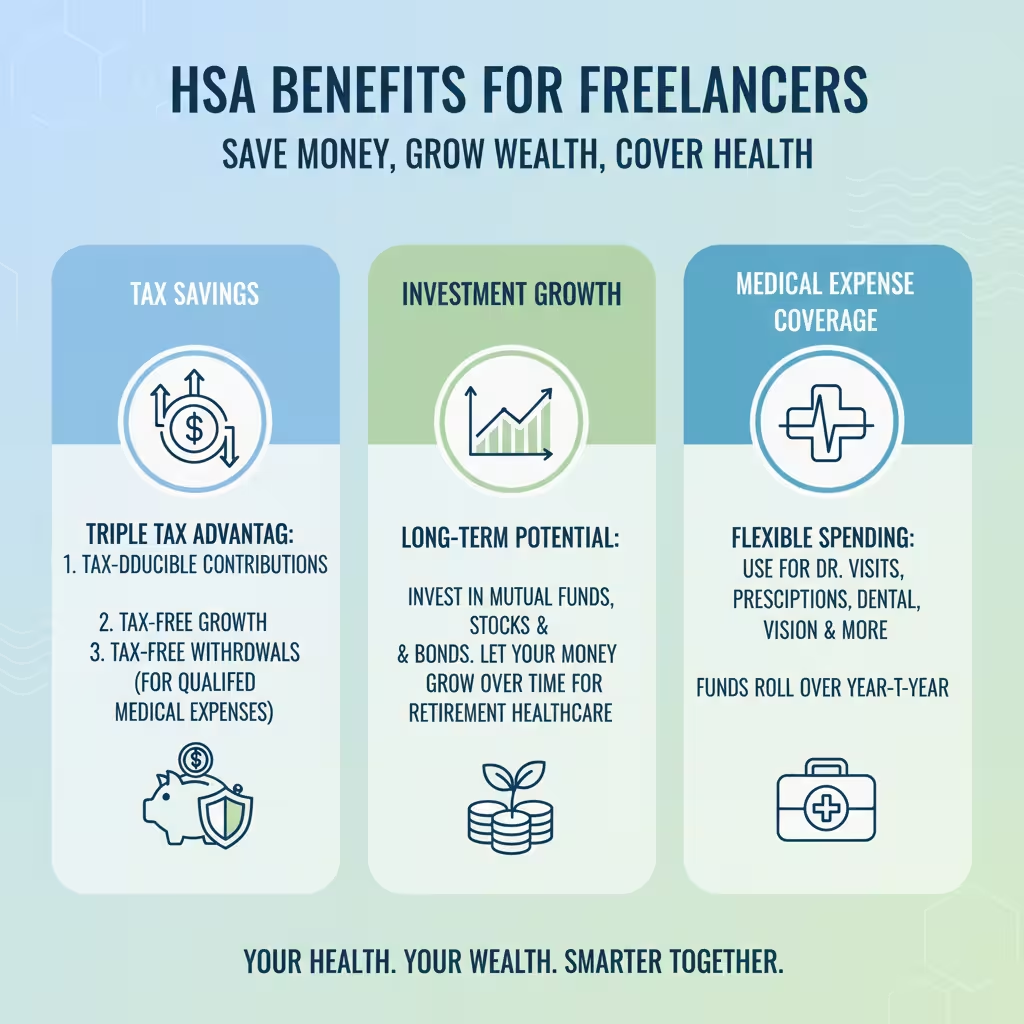

The HSA setup is the thing I wish more freelancers understood because it genuinely changes the math.

An HSA is a Health Savings Account. You can only open one if you are on a qualifying high-deductible health plan. But combine those two things and you get tax benefits that do not exist anywhere else in the US tax code.

Money you put in is not taxed going in. It grows inside the account without being taxed. And when you pull it out to pay for medical expenses it is not taxed then either. Three separate tax advantages from one account. That does not exist anywhere else.

Now here is the thing that is specific to self-employed people and almost nobody talks about it.

You pay self-employment tax. It is 15.3 percent. That covers your Social Security and Medicare. A regular salaried employee splits this cost with their employer. You pay the entire thing yourself.

HSA contributions lower that 15.3 percent tax too. Not just your regular income taxes. Both.

Put $4,400 into your HSA this year. You save about $673 just from self-employment tax — before even counting your income tax savings. At the 22 percent income tax bracket your combined savings on that $4,400 contribution is about $1,644 total. You put in $4,400 and it effectively costs you around $2,756 after taxes.

The 2026 IRS numbers: self-only coverage limit is $4,400, family is $8,750, and if you are 55 or older you can add $1,000 extra.

For the plan itself in 2026: minimum deductible of $1,700 for one person, $3,400 for a family. Out-of-pocket max of $8,500 for one person, $17,000 for a family.

New in 2026: Bronze plans and Catastrophic plans are now HSA-eligible even if they do not technically meet standard HDHP deductible requirements. Brand new this year. More freelancers can now access HSA benefits at lower monthly premium levels.

The money never disappears. Never expires. It rolls over every year. Follows you when you change plans or move states. A lot of self-employed people invest their HSA balance and treat it like a second retirement account. Start in your 30s and by your 60s that balance matters.

One thing you need for this to work: enough savings to cover your deductible if something goes wrong in a bad month. If a $1,700 emergency would empty your account, the higher deductible is real risk. But if you have a financial cushion behind you, this setup usually beats everything else for a healthy freelancer.

Catastrophic plans deserve a mention because 2026 changed who can get them.

Before, these were mostly for people under 30. A new hardship exemption now lets people of any age enroll if their income falls below 100 percent of the poverty level or above 250 percent. That covers a real chunk of middle-income freelancers who earn too much for decent subsidies but cannot stomach a $550 Silver plan every month.

Premiums run lower than Bronze. But the deductible is brutal — $10,600 for one person, $21,200 for a family. You pay almost everything yourself until you clear that number. You do get three free primary care visits per year and preventive care is covered. Beyond that it is mostly on you.

These are now HSA-eligible in 2026. Pair the lower premium with HSA contributions and the tax math can work well for someone healthy who has savings behind them.

Not for most people. But a legitimate new option for a specific group.

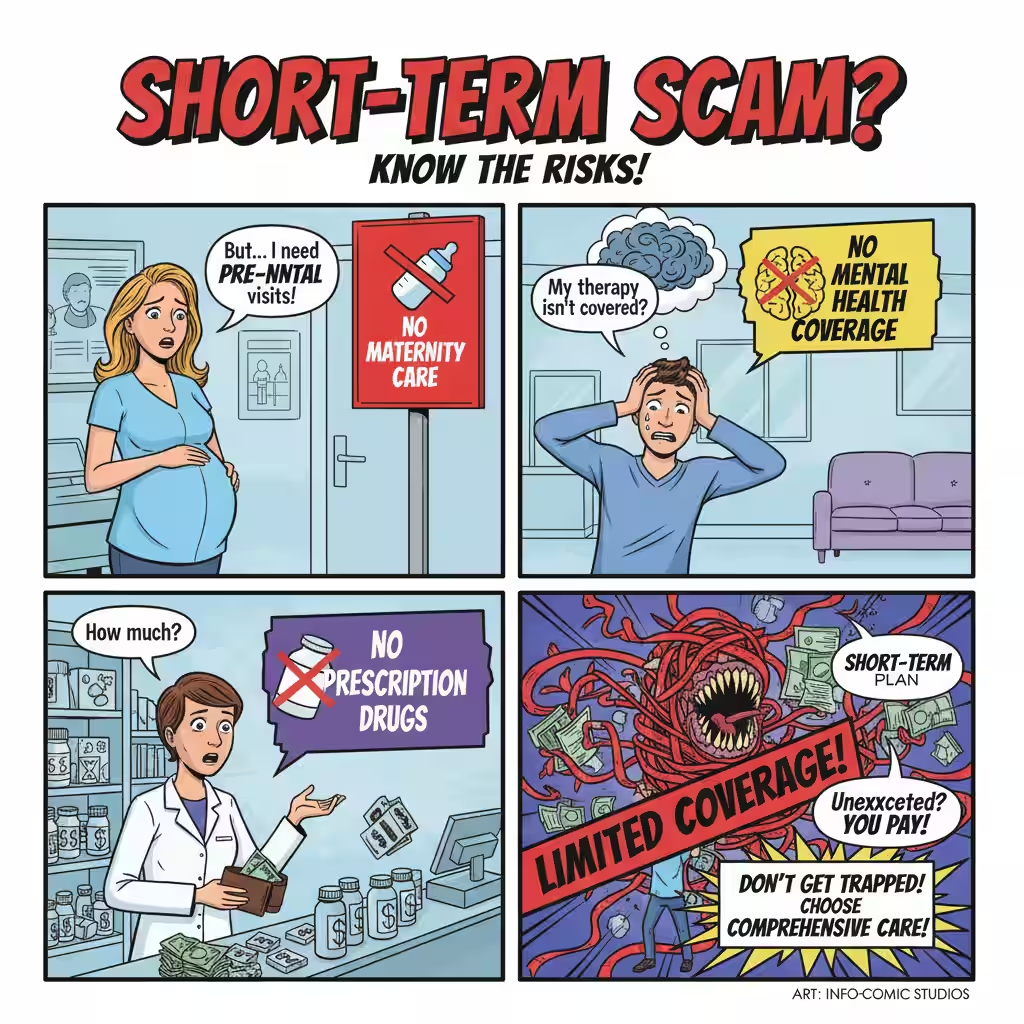

Short-term plans. I want to be honest here because these get marketed aggressively to freelancers.

They are cheap. $80 to $120 a month sometimes. Compared to $500 on the Marketplace that sounds incredible.

Here is what you are actually getting based on what major providers actually cover.

98 percent of these plans exclude maternity care entirely. 94 percent do not cover adult vaccines. 48 percent have no prescription drug coverage. 40 percent exclude mental health treatment. Most have no out-of-pocket maximum at all — meaning no ceiling on what you could owe.

They check your health history before selling to you. They can say no. They can exclude conditions you already have. ACA plans cannot do any of that. Short-term plans do it routinely.

They are legally capped at three months with one one-month extension. Four months maximum. That is the federal limit.

They are designed to fill a short gap. A few weeks between jobs. A month waiting for something else to start. That is it.

Using one as your main insurance for the whole year is a gamble that looks fine until you actually need it.

Health sharing plans come up in nearly every freelancer Facebook group and forum. Low monthly cost. Sounds appealing.

Know exactly what they are before you consider one.

They are not insurance.

Members pay into a pool each month. When someone has a medical bill the organization helps coordinate payment. It sounds similar to insurance but is fundamentally different in ways that matter.

State insurance departments do not regulate them. They are not required to cover any specific treatment. They can and do deny claims that fall outside their internal guidelines. They can exclude pre-existing conditions. There is no government fund protecting you if they run low on money.

Some of these organizations pay claims consistently. Others have left members with $80,000 in unpaid bills after a major health event. The difference is not visible on their website.

Before joining one ask for the actual member guidelines document — not the marketing overview, not the FAQ, the full document. Read what happens if you get cancer. Read what happens with a serious surgery. Get answers before you sign anything.

Something people overlook constantly: if your spouse or partner gets insurance through their job you can often join that plan as a dependent.

Employer group plans almost always cost less than individual plans. The employer contributes to the premium. The coverage is solid. Nothing complicated.

Before spending two hours comparing Marketplace plans, spend 20 minutes looking at your partner’s plan. Add up the real annual cost and compare it directly. Most people who actually do this are surprised at how much better the employer plan looks.

If this option exists for you it should be the first thing you check, not the last.

If your freelance operation has grown into a small business with actual employees, a Professional Employer Organization is worth knowing about.

PEOs co-employ your workers alongside employees from other small businesses. The combined pool lets everyone access group-rate health coverage that no single small employer could get alone.

Justworks is IRS-certified and works well for remote teams. TriNet is strong in tech and finance. Rippling is modular and tech-forward. Insperity offers more personal support for businesses without internal HR. ADP TotalSource handles multi-state operations well for companies with five or more employees.

Solo freelancer with no staff? Not relevant yet. But worth knowing if you are growing.

One more thing I want to make sure you know about because most freelancers leave money on the table here.

If you are self-employed and not covered through a spouse’s employer, you can deduct 100 percent of your health insurance premiums from your taxable income. Every single dollar.

This is called the self-employed health insurance deduction. It reduces your income before anything else is calculated. You do not need to itemize to claim it.

Real numbers: $550 a month is $6,600 a year. At the 22 percent federal tax bracket that saves you $1,452 in taxes. Your real cost drops to $5,148.

Then if you put $4,400 into an HSA on top of that, your combined tax savings on the contribution is about $1,644. The $4,400 effectively costs you around $2,756 after taxes.

The sticker price on your coverage is not your actual price. Run the real numbers. They look considerably better when you account for both deductions together.

A CPA who works with self-employed clients will make this concrete for your specific situation. Most freelancers doing this math for the first time are genuinely surprised.

Picking a Health Insurance Plan for Self-Employed without losing your mind.

Check what subsidies you qualify for before you look at any plan prices. Log into Healthcare.gov, enter your estimated income, see what comes up. This changes everything.

Be honest with yourself about how much care you actually use. A physical once a year is very different from monthly specialist visits and three prescriptions. Your real medical life drives the tier decision, not your monthly budget preference.

If you are in decent health and have savings behind you, do the HDHP plus HSA math before defaulting to Silver. The tax savings are real and most healthy freelancers come out ahead.

Check your doctors in the plan directory before you confirm. Losing a provider you trust does not show up in any premium comparison but it costs you in real ways.

And look hard at the out-of-pocket maximum. That is the worst-case number for your year. Ask yourself if you could cover it if things went badly in November. If the honest answer is no, you need a richer plan than your monthly instinct says.

Tony ended up on an HSA-eligible Bronze plan after we talked through everything. He puts $300 a month into the HSA and invests it. His premium dropped by $160 a month from what he was paying. His real after-tax cost on the whole setup is lower than anything he had before.

He called me last month just to say that.

That is what knowing your options actually does. It is not just about picking the right plan. It is about not paying more than you have to for something you absolutely cannot go without.

Go figure out your options before the next open enrollment. November comes faster than it feels like it should.

Sources: 2026 Healthcare Policy and Administration Study Guide. OBBBA Regulatory Briefing. IRS 2026 HSA and HDHP Limits. CBO Coverage Projections. KFF Health Insurance Survey.