My neighbor called me last fall in a full panic.

She had just turned 26, aged off her mom’s health plan, and was staring at a stack of enrollment options from her new job. “I don’t know what any of this means,” she said. “What’s a deductible? Do I need a PPO? What’s a copay versus coinsurance?” She’s a smart woman with a college degree. And she was completely lost.

Here’s the thing — she’s not alone. Most Americans don’t fully understand how health insurance works. Nobody teaches it in school. Your HR department hands you a packet during orientation week when you’re already drowning in paperwork. And then you’re expected to make a decision that could cost you thousands of dollars if you get it wrong.

So let’s fix that.

This guide is written for real people. Not for insurance professionals, not for policy wonks — for someone who just needs to figure out what they’re signing up for. We’ll go through everything from the basics to what’s changed in 2026, and by the end, you’ll feel a whole lot better about this stuff.

First Things First — Why Health Insurance Even Matters

Some people, especially younger folks, wonder if health insurance is really worth the monthly cost. If you’re healthy and barely go to the doctor, it can feel like throwing money away.

Then your appendix bursts at 2 a.m. on a Tuesday.

An emergency appendectomy in the US can run anywhere from $15,000 to $30,000 without insurance. A broken arm — just a regular broken arm — can cost $7,000 or more after X-rays and a follow-up visit. Even a short ambulance ride in most cities costs between $1,200 and $2,500.

Medical bills are actually the number one cause of personal bankruptcy in this country. Not bad investments. Not student loans. Medical bills.

Health insurance is what stands between you and that kind of financial wreckage. It doesn’t make healthcare free, but it puts a hard cap on how much damage one bad health event can do to your bank account.

The Words That Trip Everyone Up

Before anything else, you need a handle on the language. Health insurance has its own vocabulary, and once you get these terms down, everything else starts clicking.

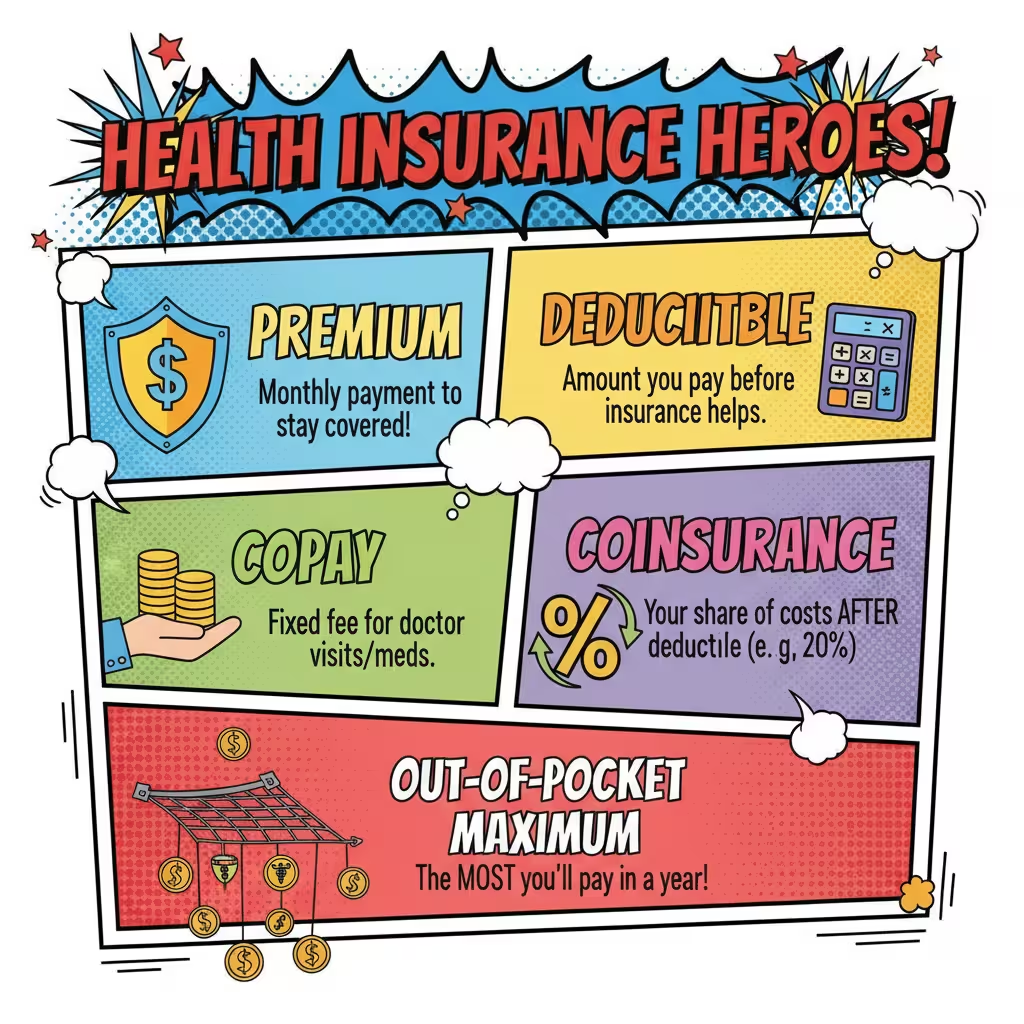

What Is a Premium?

Your premium is the monthly bill you pay to keep your insurance policy active. It doesn’t matter if you saw a doctor that month or not — the premium gets paid either way. Think of it like your phone bill. You pay it every month whether you made a hundred calls or none.

In 2026, if you’re buying coverage through the ACA Marketplace and you’re somewhere between 31 and 45 years old, you’re probably looking at around $687 a month on a mid-level Silver plan. For adults over 60, that average climbs to about $1,448 a month. Those numbers aren’t cheap, and we’ll talk later about ways to lower them.

What Is a Deductible?

This one confuses a lot of people. Your deductible is the amount you personally have to pay for medical care before your insurance company starts sharing the costs.

Say your deductible is $2,500. You go in for knee surgery. The bill is $9,000. Until you’ve paid the first $2,500 yourself, your insurer isn’t contributing a dime. After you hit that threshold, they start chipping in.

Here’s something worth knowing: family plan deductibles have tripled since 2002. They’ve gotten dramatically higher over the past twenty years, and that trend hasn’t stopped.

What Is a Copay?

A copay is a flat fee you pay at the time of a visit. Your plan might charge you $25 every time you see your primary care doctor, or $15 when you pick up a generic prescription. You know the number going in. It’s simple and predictable.

What Is Coinsurance?

Once you’ve met your deductible, your insurer doesn’t just start paying everything. You and the insurance company split the remaining costs. That split is called coinsurance.

A typical arrangement is 80/20. Your insurer covers 80% of costs, and you cover 20%. So if you have a $500 bill after meeting your deductible, you’re paying $100 and the insurance company picks up the rest.

What Is an Out-of-Pocket Maximum?

This is the most important number on your entire plan, and a lot of people don’t pay enough attention to it.

Your out-of-pocket maximum is the absolute ceiling on what you’ll spend in a year for covered, in-network care. Once you hit that number — whether it’s $6,000 or $9,000 — your insurer pays 100% of everything else for the rest of that plan year.

This is what stops one catastrophic illness from bankrupting you. Even if you get cancer or need major surgery, you know the most it will cost you in a single year. After that, the insurer takes over completely.

A Real-World Example to Tie It Together

Let’s walk through an actual scenario. Say you slip on ice, break your wrist, and need surgery.

The total hospital bill comes to $11,000. Here’s how your costs break down:

Your deductible is $3,000, and you haven’t spent anything yet this year. So you pay the first $3,000 yourself.

After that, your 80/20 coinsurance kicks in on the remaining $8,000. You owe 20% of that — which is $1,600. Your insurer pays the other $6,400.

Your total out of pocket for this whole ordeal: $4,600.

Your out-of-pocket maximum for the year is $7,000. So you’re nowhere near that cap, and you’d still pay coinsurance on future medical costs this year until you hit it.

Without insurance? That same $11,000 hospital bill lands entirely on you — and that’s before any follow-up care.

The Main Types of Health Insurance Plans

Plans aren’t all built the same way. There are a few main structures, and the right one for you depends heavily on your lifestyle and health needs.

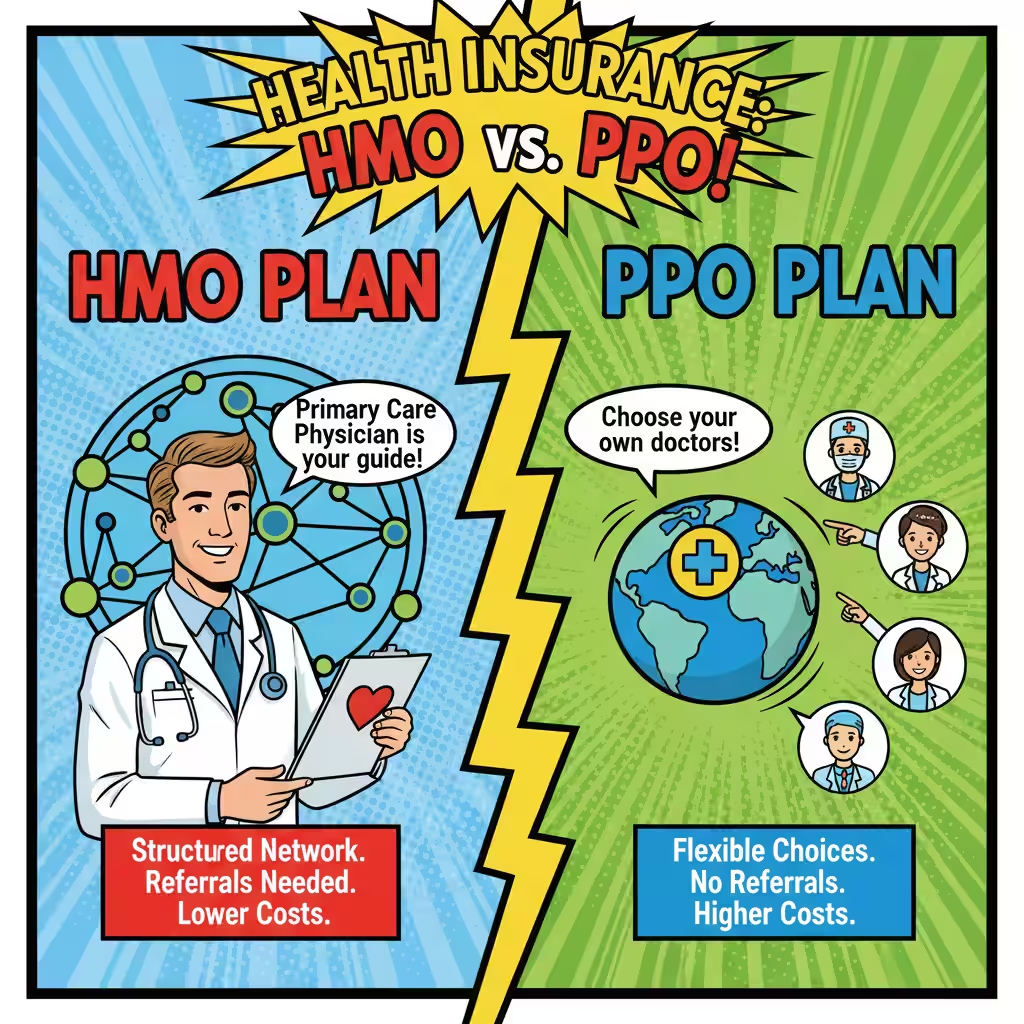

HMO Plans

HMO stands for Health Maintenance Organization. These plans tend to cost less per month, which makes them popular with people who are watching their budget.

The trade-off is structure. With an HMO, you have to pick one primary care doctor who becomes your “home base.” If you need to see a cardiologist or an orthopedist, your primary doctor has to refer you there first. And you have to stay within the plan’s network — if you go outside it, the plan won’t cover the cost.

In 2026, HMO plans average around $674 per month on the ACA Marketplace. For people who are generally healthy and don’t mind working within a defined system, an HMO can save real money over the course of a year.

PPO Plans

PPO stands for Preferred Provider Organization, though most people just say “PPO.” These plans give you a lot more room to move.

You can see any doctor you want, at any time, without needing a referral first. You can go out of network if you want — it’ll cost you more, but the plan still covers some of it. This kind of flexibility is great if you have specialists you already see, or if you travel a lot and need care in different places.

That freedom costs more. PPO plans average closer to $789 per month in 2026. If you’re managing a chronic condition or you really value being able to choose your own doctors, that extra monthly cost often makes sense.

High-Deductible Health Plans

An HDHP has lower monthly premiums and a higher deductible. The idea is that you pay less every month but take on more financial exposure if you actually need care.

These plans get a lot more interesting when you pair them with something called a Health Savings Account. More on that in a bit — because the HSA piece changes the math in a pretty significant way.

Where Americans Actually Get Their Health Insurance

There are a few main pipelines for coverage in this country, and which one applies to you depends on your situation.

Through Your Job

Employer-sponsored insurance is by far the most common way Americans get covered. Your employer pays a chunk of your premium — sometimes a very large chunk — and takes your share out of your paycheck before taxes. If your job offers this, it’s almost always your best option. The employer contribution alone can be worth thousands of dollars per year.

The ACA Marketplace

If you’re self-employed, work a job that doesn’t offer coverage, or lost your employer coverage, the ACA Marketplace at Healthcare.gov is where you shop for an individual or family plan.

Plans are organized into four metal tiers:

Bronze plans have the lowest monthly premiums but the highest deductibles and out-of-pocket costs. These make the most sense if you’re young, healthy, and confident you won’t need much care.

Silver plans split the difference between premium costs and out-of-pocket exposure. They’re the most popular option on the Marketplace, and they’re also the only tier where you can get Cost-Sharing Reductions — a special discount on your out-of-pocket costs available to people earning under 250% of the federal poverty level.

Gold plans charge higher premiums but your out-of-pocket costs are lower. If you use healthcare regularly, a Gold plan can actually save you money when you add everything up.

Platinum plans are the most expensive per month but have the lowest deductibles and out-of-pocket costs. These work best for people who expect significant ongoing medical needs.

Medicare

Medicare covers Americans 65 and older, along with some younger people who have qualifying disabilities. It’s broken into parts:

Part A handles hospital care and is typically free if you’ve paid into the system while working. Part B covers doctor visits and outpatient services, with a 2026 monthly premium of $203 — up $18 from last year. Part D adds prescription drug coverage. Medicare Advantage bundles all of this into one private plan.

The Medicare Advantage market had a rough stretch heading into 2026. Roughly 2.6 million people — about 13% of the individual Medicare Advantage market — had their plans terminated at the end of 2025. Insurers pulled back to stabilize their finances, and rural areas got hit hardest. Rural enrollees make up only about 14% of the Medicare Advantage market, but they accounted for 23% of plan terminations. In Vermont, a staggering 93% of enrollees were in plans that got cut.

Medicaid

Medicaid is the program for Americans with lower incomes, jointly funded by the federal government and individual states. If your income falls below a certain level, you might qualify for free or very low-cost coverage through Medicaid. Eligibility rules vary a lot by state.

Big Changes in 2026 You Need to Know About

The healthcare landscape shifted pretty dramatically this year, and these changes directly affect what coverage costs and who qualifies.

Premiums Jumped Hard

The enhanced premium tax credits that made Marketplace coverage much more affordable from 2021 through 2025 expired at the end of last year. The result was a roughly 26% average increase in Marketplace premiums in 2026.

A KFF survey of people who had enrolled in 2025 plans found that 80% of those who came back in 2026 reported paying more — and over half said their costs were “a lot higher.” Even worse, 55% of enrollees said they had cut back on food and basic household expenses just to keep their health coverage. About one in four people who switched plans moved down to a cheaper bronze plan, accepting higher out-of-pocket risk in exchange for a lower monthly bill.

The One Big Beautiful Bill Act

Signed into law on July 4, 2025, this massive budget legislation — officially called the One Big Beautiful Bill Act, or OBBBA — brought major changes to Medicaid, Medicare, and the ACA.

For Medicaid, the law added a work requirement. Adults between 19 and 64 who receive Medicaid under the expansion now need to complete at least 80 hours per month of qualifying activity — paid work, job training, community service, or school enrollment. Exemptions exist for people who are pregnant, caring for young children, dealing with a serious disability, or classified as medically fragile.

Eligibility redeterminations are also getting more frequent. Starting at the end of 2026, expansion-group enrollees will have their eligibility checked every six months instead of once a year. That’s a meaningful change — more paperwork, more chances for administrative gaps to knock someone off coverage they’re entitled to.

The law also tightened access to premium tax credits on the Marketplace by requiring strict income verification before enrollment, which ended automatic re-enrollment for a lot of people.

HSAs: The Tax Trick Most People Are Sleeping On

If you sign up for a High-Deductible Health Plan, you become eligible for a Health Savings Account. And honestly, the HSA might be the most underused financial tool in America.

Here’s why it’s special. An HSA gives you three separate tax breaks, which is almost unheard of in the tax code:

Your contributions go in tax-free, reducing your taxable income for the year. The money grows inside the account without being taxed on the gains. And when you take money out to pay for a qualified medical expense, that withdrawal isn’t taxed either.

On top of all that, the money never expires. It rolls over from year to year. If you open an HSA at 30 and stay healthy for a decade, that money just keeps sitting there and growing. A lot of people use their HSAs as a secondary retirement account — investing the balance and letting it compound until they need it later in life.

Compare that to a Flexible Spending Account, which works through your employer. FSAs let you set aside pre-tax money for medical expenses, but they come with a catch: most of that money disappears if you don’t spend it by the end of the plan year. They’re still useful, but they require planning. You have to estimate how much you’ll spend in advance and use it or lose it.

What the “Great Healthcare Plan” Means for Consumers

The current administration has been pushing a set of healthcare priorities under the banner of the “Great Healthcare Plan.” A few pieces of it are worth knowing about as a consumer.

One initiative calls for all providers and insurers that accept Medicare or Medicaid to prominently display their prices. The idea is that you should be able to walk in somewhere and know what things cost before they happen — not find out six weeks later when a bill shows up in your mailbox.

There’s also a new “Plain English” standard being pushed for insurers. Instead of burying rate and coverage comparisons in fine print and technical language, companies would have to publish that information in language regular people can actually understand. The goal is to make shopping for insurance less like reading a legal contract and more like comparing phone plans.

Insurers are also being pushed to publicly report how often they reject claims, how long patients wait for routine appointments, and what percentage of premium revenue actually goes toward paying for care — a metric called the Medical Loss Ratio. Higher MLR means more of your premium money is going to healthcare rather than overhead and executive salaries.

Whether these measures fully take hold depends on implementation, but the direction is toward more transparency than the system has had historically.

How to Actually Choose the Right Plan

Here’s a framework that cuts through the noise.

Start by asking yourself one honest question: how much healthcare did I actually use last year?

If the answer is “barely any” — a couple of routine checkups, maybe one urgent care visit — you’re probably a good candidate for a High-Deductible Health Plan. Your monthly premium will be lower, and you can build up your HSA over time as a safety net. The risk is manageable if you have enough savings to cover that higher deductible in a bad year.

If the answer is “quite a bit” — you take regular medications, you see specialists, you have an ongoing health condition — a Gold or Silver plan often works out cheaper in total when you factor in all your out-of-pocket costs throughout the year. The higher monthly premium buys down your exposure when you actually use the coverage.

Before you commit to anything, run through this short checklist:

Is your current primary care doctor in the plan’s network? Losing your doctor is a real cost that doesn’t show up in the premium number.

Are your prescriptions covered, and at what cost? Drug formularies vary widely between plans.

Can you realistically afford the out-of-pocket maximum if something goes seriously wrong this year? If the answer is no, you might need a richer plan than your premium instincts suggest.

Does the plan require referrals to see specialists? If you already see a specific specialist regularly, an HMO requiring referrals adds friction and potential delays.

Quick Reference: Terms You’ll See Everywhere

| Term | Plain English Meaning |

| Premium | What you pay monthly to keep your insurance |

| Deductible | What you pay first before insurance helps |

| Copay | Flat fee per visit or prescription |

| Coinsurance | Your share of costs after deductible is met |

| Out-of-Pocket Max | The most you’ll pay in one year — then 100% covered |

| HSA | Tax-triple-advantaged savings paired with HDHPs; rolls over forever |

| FSA | Pre-tax employer savings for medical costs; mostly use-it-or-lose-it |

| HMO | Cheaper, requires referrals, network-only |

| PPO | More expensive, total flexibility, no referrals needed |

| HDHP | Low premium, high deductible, unlocks HSA |

| Silver Plan | Mid-tier Marketplace plan; only tier eligible for CSR discounts |

| CSR | Out-of-pocket discount on Silver plans for lower-income enrollees |

| MLR | What percentage of your premium actually goes to healthcare |

| Prior Authorization | Insurance company must approve certain services before you get them |

| ESI | Health insurance through your employer |

Wrapping It Up

If you made it this far, you already understand more about health insurance than most Americans do. Seriously.

The system is genuinely complicated, and it’s not set up to make things easy on consumers. In 2026, with premiums up across the board, new Medicaid requirements taking effect, and Medicare Advantage plans disappearing in some markets, there’s more riding on your coverage decisions than ever before.

But here’s what I want you to take away from all of this:

You don’t have to understand every corner of the system. You just have to understand your plan. Know your premium. Know your deductible. Know your out-of-pocket max. Know whether your doctors are in network. Check whether your medications are covered.

Do those five things, and you’re already making smarter decisions than most people who just click “re-enroll” every year without reading anything.

Health insurance isn’t exciting. Nobody gets passionate about coinsurance percentages. But getting this right protects your health, your family, and your financial future all at once. That makes it worth a few hours of your time — and hopefully, this guide made that time a whole lot shorter.

Research sourced from: 2026 Healthcare Policy and Insurance Study Guide, Briefing Document on 2026 Healthcare Landscape and Legislative Reforms, KFF consumer surveys, and CMS Medicare data.