Okay so I’m gonna be real with you for a second.

When I first had to pick my own health insurance plan I genuinely stared at the screen for like 45 minutes. HMO. PPO. EPO. POS. It looked like someone just threw a bunch of random letters at me and said “good luck, figure it out.”

I picked wrong, by the way.

Picked a PPO because my coworker said PPOs were “the good ones.” Paid way more than I needed to that whole year. Barely went to the doctor. Could’ve had a perfectly fine HMO for like $150 less every month and honestly would not have noticed a single difference in my actual life.

So here’s what I wish someone had told me before I wasted that money. A plain, no-fluff breakdown of HMO vs PPO and where EPO fits in. No insurance jargon. No corporate-speak. Just what these things actually mean for your wallet and your life.

Let’s Start With the Big Picture First

There are really only a few questions that matter when picking a plan type.

Do you want to pay less each month or do you want more freedom to see whoever you want?

That’s basically it. That’s the whole game.

Every plan type is just a different answer to that question. HMOs lean hard toward saving money. PPOs lean hard toward freedom and flexibility. EPOs are kind of in the middle and most people have never even heard of them which is a shame because they’re actually pretty solid.

The 2026 marketplace data tells you what’s happening out there right now. Total enrollment dropped 5% from last year. New signups fell 14%. Nearly a million people fewer than the year before. People are struggling with the cost. Premiums jumped after the government stopped padding them with extra credits that expired December 31, 2025. Ohio dropped 20%. North Carolina dropped 22%.

People are either picking cheaper plans or skipping coverage entirely. Neither of those is great. But understanding what each plan type actually does helps you make a smarter call than most people are making right now.

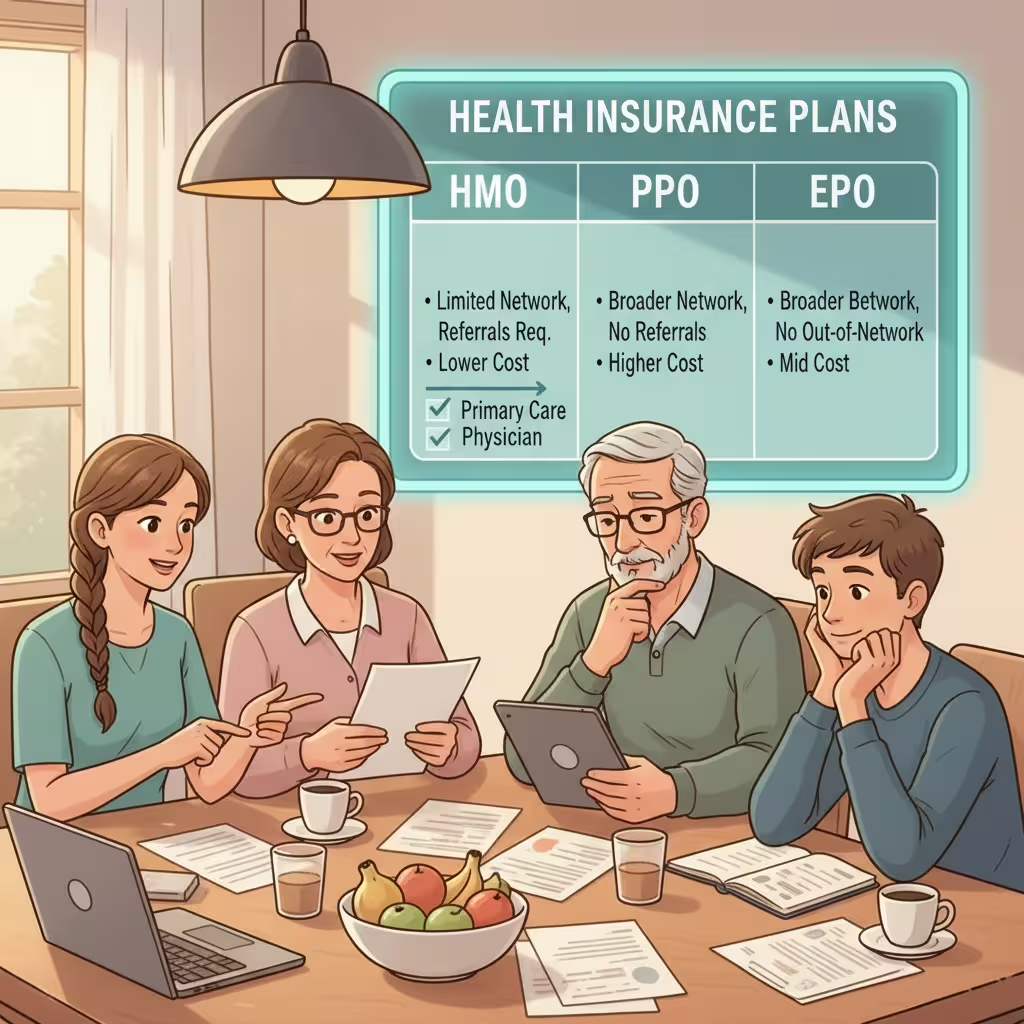

HMO Plans — The “Stay In Your Lane” Option

HMO stands for Health Maintenance Organization. That name tells you almost nothing useful so forget it.

Here’s what actually matters about an HMO.

You pick one doctor. One. That is your primary care physician — your PCP. They are the gatekeeper to basically everything else. Wanna see a specialist? Your PCP has to refer you. Wanna see a dermatologist? Cardiologist? Orthopedist? Your PCP sends you there first or the HMO doesn’t pay.

And you have to stay in network. Full stop. If you go to a doctor outside the HMO’s approved list, you’re usually paying 100% of that bill yourself. Emergency situations are an exception. But regular care, planned visits, anything you schedule yourself — it better be in network.

Why would anyone want that kind of restriction?

Because HMOs are cheap. Like genuinely the most affordable option month to month. Lowest premiums of any plan type. Most predictable costs. You know pretty much exactly what you’re going to spend.

If you’re young and healthy and your main medical activity is one physical a year and maybe an urgent care visit when you get strep throat, an HMO is probably all you need. You’re not using a specialist. You’re not traveling for care. You’re not managing five conditions with five different doctors.

The HMO works perfectly fine for you. And you save real money.

Where HMOs get frustrating is when you actually get sick. Like really sick. The referral process adds time. Waiting for your PCP to send you somewhere can feel slow when you’re not feeling well. And if the specialist you actually want isn’t in network — tough. You either use who they say or you pay out of pocket.

That’s the trade. Lower cost, less control.

PPO Plans — The “Do Whatever You Want” Option

PPO is Preferred Provider Organization. Again, the name is useless. Here’s what matters.

No referrals. Ever. You want to see a spine surgeon? You book it yourself. You want a second opinion from a completely different hospital system? Go ahead. You want to see someone out of state? Most PPOs cover that.

You can go out of network too. You’ll pay more — like your coinsurance gets worse and your deductible might be higher for out-of-network care — but you’re covered. Some of it at least.

That flexibility is genuinely valuable for certain people.

If you have an ongoing condition and you’ve built relationships with specific specialists you trust, a PPO means you never have to worry about whether those doctors are “approved” by a gatekeeper. You just go. If you travel a lot for work or live in one city part of the year and another city another part, PPOs give you coverage that follows you. If you’re managing something complicated with multiple doctors involved, you can coordinate your own care without waiting on a PCP referral for every single step.

The catch is price. PPOs cost more. A lot more sometimes. Higher monthly premiums. Often higher deductibles. And if you go out of network, you’re dealing with worse cost-sharing.

Here’s where I see people mess up with PPOs. They get a PPO because they like the idea of having options. But then they never actually use those options. They see the same two in-network doctors they’ve always seen. They never go out of network. They never visit a specialist without it being totally routine.

That person paid hundreds of extra dollars a month for freedom they didn’t use.

The PPO is the right call when you actually need that flexibility. Not just when it sounds nice.

EPO Plans — The One Nobody Talks About

EPO stands for Exclusive Provider Organization. You don’t hear about these as much and I think that’s kind of unfair because EPOs hit a sweet spot that a lot of people would actually like.

Here’s the deal with EPOs.

No referrals needed. So you can see a specialist whenever you want — just like a PPO. You don’t need your primary care doctor to send you anywhere. You just book it.

But you have to stay in network. So you can’t go to out-of-network doctors like you can on a PPO. That restriction is there, same as an HMO.

So what does that actually give you?

Lower premiums than a PPO because of the network restriction. But more flexibility than an HMO because you don’t need referrals.

For a lot of self-employed people or freelancers who are comfortable sticking with one provider network but hate the idea of needing a referral before seeing a specialist, an EPO is kind of perfect. You get the freedom of direct specialist access. You get a monthly price that doesn’t destroy your budget.

The early retirement crowd — people who are under 65 and not on Medicare yet — does pretty well with EPOs too. You need solid coverage for potentially many years before Medicare kicks in but you’re probably not running around to out-of-network providers all the time.

The research actually recommends EPOs specifically for people in that early retirement window. Manageable costs with solid comprehensive coverage until you hit 65.

POS Plans — The Weird Hybrid Nobody Fully Understands

Point-of-Service plans. POS.

These are like if an HMO and PPO had a baby and that baby could not decide what it wanted to be.

You have a primary care doctor like an HMO. You need referrals for the lowest-cost care like an HMO. But you can also go out of network if you want, like a PPO — you just pay more for it.

So it’s flexible but also kind of complicated. The cost can go up fast if you’re bouncing between in-network and out-of-network care without tracking it carefully.

I’ll be honest. Most people don’t need to overthink POS plans. If you find one that fits your situation, great. But for most freelancers and self-employed people comparing plan types, you’re usually choosing between HMO, PPO, and EPO in practice.

The 2026 Market Context You Need to Know

Here’s why all of this matters more right now than it did two or three years ago.

The government’s extra help paying for Marketplace premiums — Enhanced Premium Tax Credits — expired December 31, 2025. Congress didn’t renew them. And the One Big Beautiful Bill Act passed in July 2025 changed how subsidies work and added new eligibility requirements.

The result is ugly. Premiums are up. Enrollment dropped. Nearly 1.2 million fewer people bought plans this year than last year. Fourteen percent fewer new customers in 2026 than 2025.

Some states are doing okay. New Mexico actually went up 14% — the best in the country — because the state started its own subsidy program to replace the expired federal credits. Smart move.

Other states are getting hammered. Ohio lost 20%. North Carolina lost 22%. Georgia dropped 14%. These are people who couldn’t make the new premium numbers work and either downgraded to cheaper plans or walked away entirely.

What that means for you: picking the right plan type matters more now because you can’t afford to overpay for flexibility you won’t use. But you also can’t afford to underbuy and get stuck with massive out-of-pocket costs if something happens.

HMO vs PPO: The Honest Comparison

Let me put these two head to head because that’s what most people are actually trying to figure out.

Cost: HMO wins. Not close. Lower monthly premiums, lower deductibles typically, more predictable costs throughout the year.

Specialist access: PPO wins. No referrals, go whenever you want, see who you want.

Out-of-network coverage: PPO wins. HMOs basically don’t cover out-of-network care except emergencies.

Simplicity: HMO wins in a weird way. One doctor manages your care. Less coordination to figure out on your own. Some people actually like that.

Good for families? Depends. Families with young kids who mostly need pediatric care and don’t need specialists constantly — HMO can work great and saves significant money. Families managing complex health situations with multiple specialists — PPO is worth the extra cost.

Good for travelers? PPO. Hands down. If you work across state lines, travel frequently for work, split time between cities — you want the out-of-network coverage a PPO gives you. An HMO could leave you without real coverage depending on where you are when something happens.

Good for the self-employed? Honestly? The research suggests PPOs specifically for freelancers because you don’t have an HR department scheduling your appointments or managing referrals. Direct specialist access fits the freelancer lifestyle. But if cost is the main pressure — and in 2026 it usually is — an EPO is worth a serious look.

Can I See a Specialist Without a Referral on a PPO?

Yes. Full stop.

On a PPO you book specialist appointments yourself. You don’t ask anyone’s permission. You don’t wait for your primary care doctor to send paperwork somewhere. You find the specialist, you call, you go.

That’s genuinely one of the most useful things about PPOs and it’s the main reason people pay extra for them.

On an HMO you cannot do this. Your primary care doctor has to refer you first. If they disagree that you need the specialist, that can slow things down considerably. On an EPO — no referral needed either, but you must stay in network.

What About HDHPs?

High-Deductible Health Plans are their own category but they can be structured as HMOs, PPOs, or EPOs underneath.

The defining feature is the deductible. High. In 2026, minimum deductible of $1,650 for an individual, $3,300 for a family. You pay a lot before insurance really helps.

But HDHPs unlock Health Savings Accounts. And HSAs are genuinely one of the best financial tools available if you’re self-employed. Triple tax advantage — money goes in untaxed, grows untaxed, comes out untaxed for medical expenses.

For gig workers with variable income, an HDHP plus HSA can work really well. When money is tight you contribute less to the HSA. When a good month hits you top it up. The flexibility matches the income pattern.

If you’ve got three to six months of expenses saved up as a buffer, you can generally handle the higher deductible risk that comes with an HDHP. Without that cushion it’s riskier.

How to Actually Pick Between Them

Stop looking at just the monthly premium. Seriously. That’s the mistake everyone makes and it costs people real money.

Look at the worst case instead. Add up your annual premium plus your out-of-pocket maximum. That’s the most you’ll ever spend in a year on that plan. Compare that number across the plans you’re considering. Sometimes the “cheap” plan has such a high out-of-pocket max that it’s actually more expensive in a bad health year than the “expensive” plan.

Then ask yourself these questions honestly.

Do I have a doctor I really like who I’d be upset about losing? Check if they’re in each plan’s network before anything else. Losing your doctor is a real cost that never shows up in the premium comparison.

Do I travel a lot or live somewhere part-time? You want PPO or at minimum POS if you need coverage across different regions or states.

Do I have ongoing conditions that require regular specialist visits? PPO or EPO — no referral delays, direct access when you need it.

Am I pretty healthy and mostly just need basic coverage for emergencies and checkups? HMO. Save the money.

Do I have an irregular income that goes up and down month to month? HDHP with HSA lets you adjust contributions. That flexibility has real value.

The Quick Cheat Sheet

Just to make this stupidly simple.

HMO — cheapest monthly, need referrals, stay in network, best for healthy people who rarely see doctors.

PPO — most expensive monthly, no referrals, can go out of network, best for frequent travelers, complex health needs, and people who want maximum control.

EPO — middle price, no referrals, must stay in network, best for people who want specialist freedom without the PPO price tag.

POS — hybrid, need referrals for cheapest rates, out-of-network available at higher cost, works but complicated.

HDHP — high deductible, low premium, unlocks HSA, best for healthy people with emergency savings who want tax advantages.

Frequently Asked Questions – FAQ’s

1. What is the difference between HMO and PPO health insurance plans?

HMO plans are more affordable but require you to stay in-network and get referrals for specialists. PPO plans offer more flexibility, allowing you to see out-of-network providers and specialists without referrals, but they come with higher premiums.

2. Which health insurance plan is best for freelancers?

Freelancers often benefit from PPO plans for their flexibility and direct access to specialists. However, if cost is a concern, EPO plans offer a balance of affordability and specialist access without referrals.

3. Can I see a specialist without a referral on an HMO plan?

No, HMO plans require a referral from your primary care physician to see a specialist. Without a referral, the HMO typically won’t cover the visit.

4. What is an EPO health insurance plan, and how does it compare to HMO and PPO?

EPO plans don’t require referrals to see specialists, like PPOs, but you must stay in-network, similar to HMOs. They are a middle-ground option with lower premiums than PPOs but more flexibility than HMOs.

5. Are PPO plans worth the higher cost?

PPO plans are worth it if you need flexibility, travel frequently, or require ongoing specialist care. However, if you don’t use these features, you might be overpaying for benefits you don’t need.

6. What is the cheapest health insurance plan type for self-employed individuals?

HMO plans are typically the most affordable option, offering the lowest monthly premiums and predictable costs. They are ideal for healthy individuals with minimal healthcare needs.

7. Can I use out-of-network doctors with an HMO plan?

No, HMO plans generally do not cover out-of-network care except in emergencies. You’ll need to stay within the network for regular and planned visits.

8. What is the main advantage of an EPO plan for self-employed people?

EPO plans provide direct access to specialists without referrals while maintaining lower premiums than PPOs. They are ideal for those who don’t need out-of-network coverage but want more flexibility than an HMO.

9. How do I choose the right health insurance plan for my needs?

Consider your healthcare usage, budget, and lifestyle. If you travel or need specialist care, a PPO or EPO might be best. If you’re healthy and want to save money, an HMO could be the right choice.

10. What happens if I pick the wrong health insurance plan?

Choosing the wrong plan can lead to higher out-of-pocket costs, limited access to preferred doctors, or paying for flexibility you don’t use. It’s essential to evaluate your needs and compare total annual costs before deciding.

One Last Thing

The 2026 market is hard. Prices are up. More people are going without coverage than at any point in recent years. Ohio lost 20% of its marketplace enrollees. That’s a lot of people walking around uninsured right now.

Picking the right plan type won’t fix every problem. But picking the wrong one — paying for PPO flexibility you never use, or getting stuck with an HMO that can’t handle your actual health needs — that cost is real and it comes out of your pocket directly.

Know what you actually need. Compare total annual cost, not just monthly premium. Check that your doctors are in the network. And pick the plan that fits your real life, not the one that sounds most impressive at a dinner party.

That’s it. That’s the whole thing.

Sources: 2026 Health Insurance Marketplace Enrollment Trends and Plan Analysis. CMS Open Enrollment Data. 2026 Healthcare Policy and Administration Study Guide. KFF Health Insurance Survey.