Last Updated: April 2026

Mark thought he was covered.

He’d paid his homeowners insurance premium every year without missing one. He had what his agent called “solid coverage.” Then a hailstorm ripped through his Dallas suburb in the spring of 2025, and his roof was done. The adjuster came out, confirmed the damage, and cut him a check for $4,200.

The roof cost $19,000 to replace.

Mark wasn’t a victim of fraud or a rogue insurer. He was a victim of a policy clause he’d never read — a wind and hail deductible written as a percentage of his home’s insured value, not a flat dollar amount. On a $380,000 home, that 2% deductible meant he owed the first $7,600 before the insurance kicked in. And because his policy used actual cash value instead of replacement cost for his aging roof, the payout was cut again for depreciation.

He paid for insurance every month. He still paid $14,800 out of pocket.

Mark’s story is not unusual. It is, in 2026, practically the default experience for homeowners who haven’t updated or reviewed their policy in the last few years. This guide breaks down exactly what home insurance covers, how much you need, and what the fine print costs you when you don’t read it.

What Is Home Insurance and What Does It Actually Cover?

Home insurance — also called homeowners insurance or house insurance — is a contract between you and an insurance company. You pay a premium. They agree to cover certain financial losses tied to your home and belongings.

Most standard policies are built around four core protections.

Dwelling coverage pays to repair or rebuild the physical structure of your home if it’s damaged by a covered event. This includes the walls, roof, floors, and built-in appliances. If a tree falls on your house or a fire guts your kitchen, dwelling coverage handles the rebuild cost — up to your policy limit.

Personal property coverage protects your belongings. Furniture, electronics, clothing, appliances. If your stuff is stolen or destroyed in a covered loss, this pays to replace it.

Liability protection covers you if someone is injured on your property and decides to sue. It also covers damage you, your family members, or your pets cause to someone else’s property. Most standard policies start at $100,000 in liability — but many financial advisors say $300,000 is the bare minimum for a homeowner today.

Additional living expenses (ALE) — sometimes called loss of use — pays for a hotel, meals, and temporary housing if your home becomes uninhabitable after a covered event. If your house burns down on a Tuesday, ALE means you’re not sleeping in your car on Wednesday.

That’s the foundation. What most homeowners miss is what sits on top of — and underneath — that foundation.

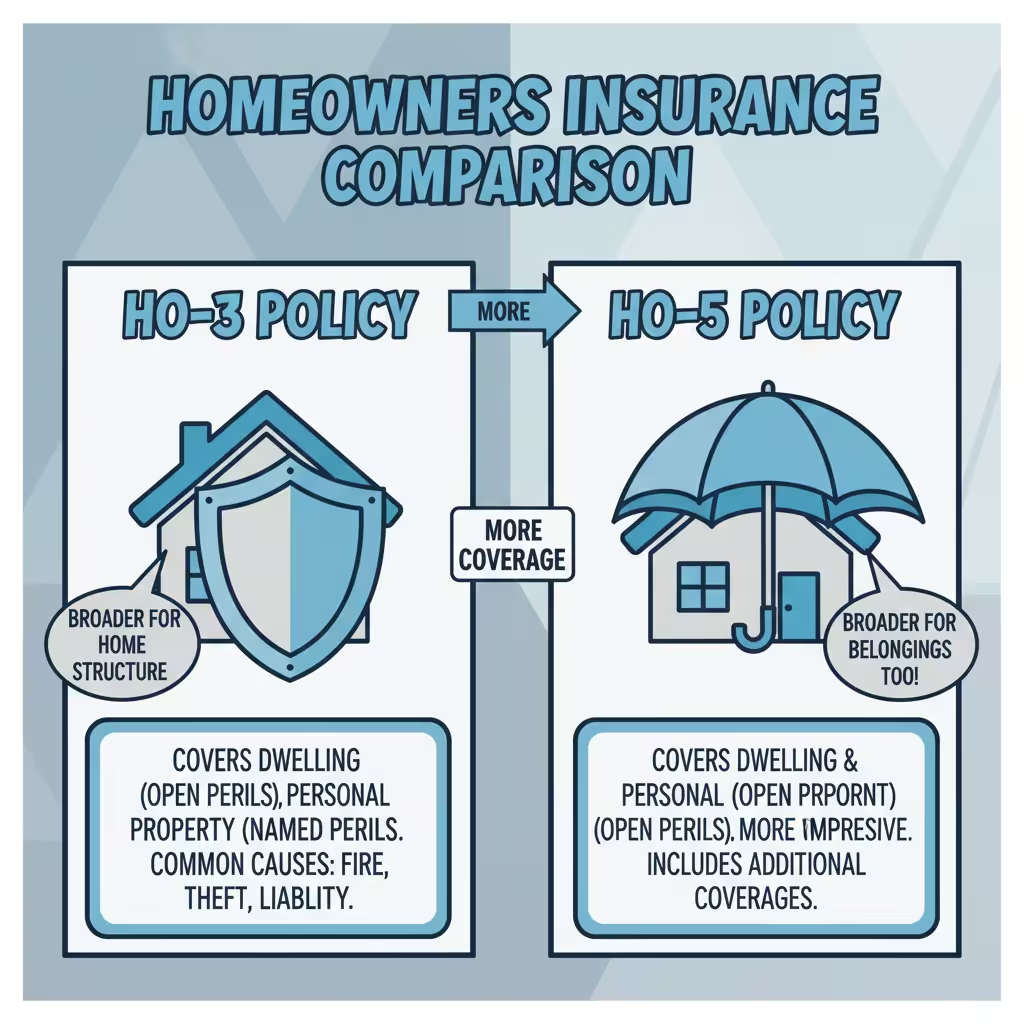

HO-3 vs. HO-5: The Policy Form Nobody Explains

When you buy homeowners insurance, you’re buying a specific policy form. The form determines what’s covered, how it’s covered, and who carries the burden of proof when you file a claim.

The most common is the HO-3 policy, also called the Special Form. It’s what roughly 80% of American homeowners carry. The HO-3 covers your dwelling on an “open perils” basis — meaning damage is covered unless the cause is specifically excluded in the policy. That sounds good. The problem is that your personal property gets much narrower treatment. Under the HO-3, your belongings are only covered for 16 named perils listed in the policy. If the cause of loss isn’t on that list, the claim is denied. And the burden of proof falls on you to show the cause was a covered event.

The HO-5 policy — the Comprehensive Form — covers both the structure and your personal belongings on an open perils basis. Accidental damage is included. Spill red wine on a $4,000 rug? Covered. Drop your laptop? Covered. The burden of proof flips: the insurer must prove the cause was specifically excluded to deny the claim.

Top carriers like Amica and Chubb typically write HO-5 policies. They cost more — but in a world where claims disputes are rising, the HO-5 shifts the fight back to the insurer’s court.

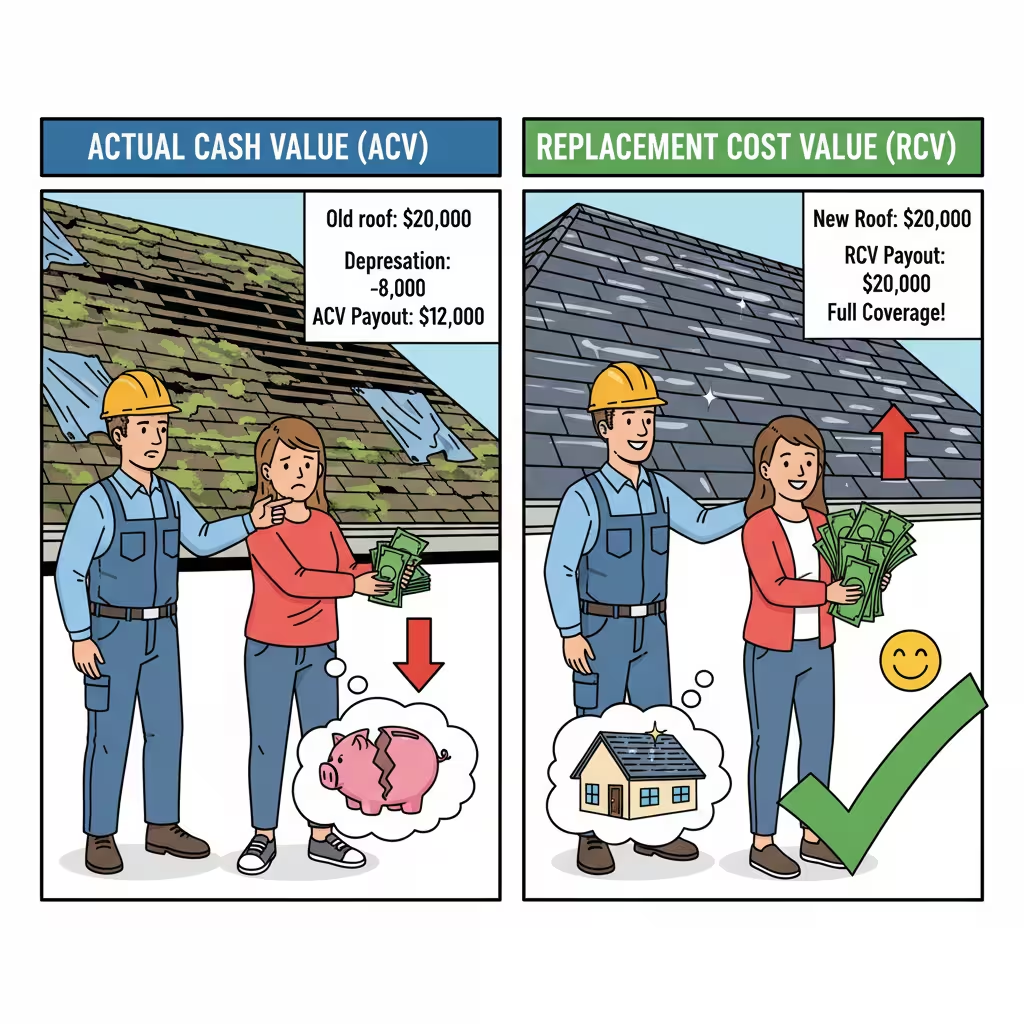

Replacement Cost vs. Actual Cash Value: The Gap That Ruins Claims

This is where Mark’s story went wrong. And it’s where most homeowners get blindsided.

Actual Cash Value (ACV) pays out what your property is worth today — after depreciation. A roof installed ten years ago isn’t worth what a new roof costs. The insurer calculates the age, wear, and expected remaining life of the item, then reduces the payout accordingly. In an environment where structural replacement costs have risen nearly 30% over the last five years, ACV settlements are leaving homeowners with payouts that cover only 30% to 50% of what the actual repair costs.

Replacement Cost Value (RCV) pays what it costs to buy or build new, at current prices. No depreciation deduction. If lumber costs more this year than it did when your house was built, RCV covers that gap.

The difference isn’t trivial. On a $25,000 roof claim, the gap between ACV and RCV can easily be $8,000 to $12,000 out of your pocket. If your policy doesn’t specify RCV, assume you have ACV. Call your agent today and ask directly.

If you want to understand how to calculate your actual replacement cost — not just accept what your insurer estimates — the Insurance Information Institute provides a free home replacement cost estimator that’s worth running annually.

How Much Home Insurance Do You Actually Need?

This is the question most homeowners never ask clearly enough. The answer has three parts.

Dwelling coverage should equal the full cost to rebuild your home from the ground up — not the market value, not what you paid for it, and not what you owe on the mortgage. Rebuilding costs have risen sharply. Supply chain disruptions, skilled labor shortages, and recent tariffs on imported materials have pushed structural replacement costs up nearly 30% since 2021. Ask your insurer for a component-based valuation — not just a flat estimate.

Personal property coverage is typically set at 50% to 70% of your dwelling limit by default. That may not be enough if you own high-value electronics, jewelry, or musical equipment. Run a home inventory — even a rough one — and compare it to your coverage limit.

Liability protection should be at least $300,000 for most homeowners. If you have significant assets, consider an umbrella policy that extends your liability coverage to $1 million or more.

One hard truth: the “right amount” of home insurance is almost always more than the default number your policy was written at three or four years ago. Costs have moved. Your coverage limits haven’t.

The Perils That Are Changing Everything in 2026

Here’s what’s reshaping the insurance market right now — and what it means for your premium and your coverage.

Severe Convective Storms — hail, tornadoes, and high winds — have quietly become the dominant loss driver in the US. These storms caused more than $50 billion in insured losses in each of the last three years. Because they hit the Midwest and Southeast repeatedly, insurers have started writing separate wind and hail deductibles into policies in those regions. These are often percentage-based, not flat dollar amounts. A 2% deductible on a $400,000 home is $8,000 before your insurer pays a dime.

Wildfires remain a top concern, particularly in California and the West. The 2025 Los Angeles fires destroyed more than 16,000 structures and triggered $22.4 billion in insurance payments. Following those fires, California passed the “Eliminate The List” Act (SB 495), which now requires insurers to pay a 60% advance on personal property limits — up to $350,000 — for total loss wildfire survivors, without requiring a full itemized inventory upfront. That’s a real win for homeowners caught in catastrophic events.

Roof age has become a major underwriting factor everywhere. U.S. roof claims hit nearly $31 billion in 2024. Insurers are now using AI-driven satellite imagery to verify roof condition. Homeowners with roofs older than 15 years in hail-prone areas are increasingly being declined by standard carriers and pushed into the Excess & Surplus (E&S) market, where premiums are higher and consumer protections are weaker.

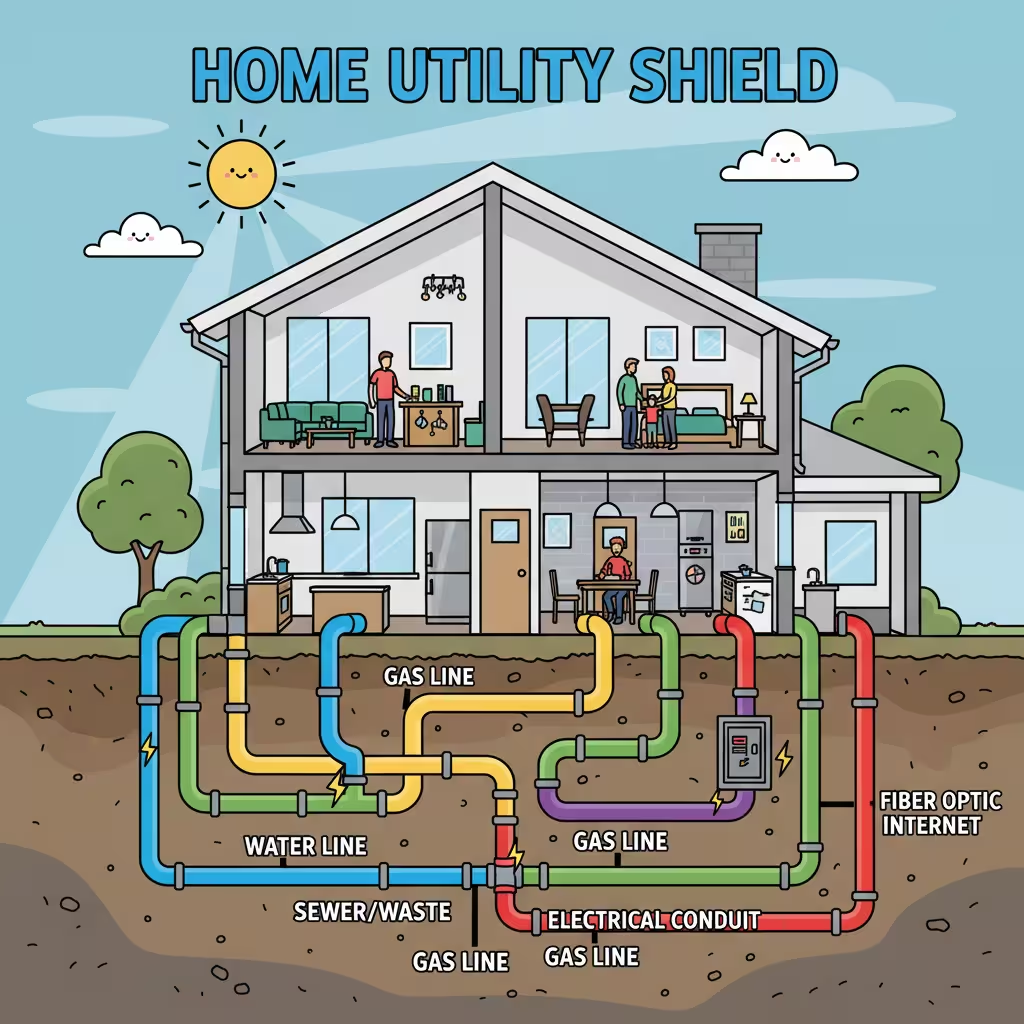

Essential Endorsements Worth Adding Right Now

Standard property insurance policies have gaps. These three endorsements close the most common and most expensive ones.

Service Line Coverage protects the underground utility pipes that run from your house to the street — water lines, sewer lines, power conduits. Standard policies exclude these entirely. When a tree root collapses your sewer line or corrosion breaks a water main underground, the repair runs $8,000 to $12,000. Service line coverage costs about $30 to $80 per year and is, dollar for dollar, one of the best values in residential insurance today.

Equipment Breakdown acts as a warranty for your home’s sophisticated systems — HVAC units, smart home arrays, emergency generators. Standard policies don’t cover mechanical failure. This endorsement does. Cost: roughly $25 to $50 per year.

Building Code Upgrade Coverage pays for the additional cost of rebuilding to current code standards, which can be required even if you’re just repairing part of your home. In California, new laws require at least 10% of the dwelling limit be allocated to this coverage in certain policies. Other states are moving in the same direction.

None of these endorsements are expensive. All three can prevent five-figure out-of-pocket costs that a standard policy would simply deny.

Is Home Insurance Required?

Technically, no federal law requires you to carry homeowners insurance. But if you have a mortgage, your lender almost certainly does. It’s written into your loan agreement — and if you let coverage lapse, your lender has the right to purchase “force-placed” insurance on your behalf and add the cost to your mortgage. Force-placed policies are expensive, limited in scope, and protect the lender’s interest, not yours.

If you own your home outright, you’re free to go without insurance. That’s a risk calculation that is almost never worth making. In 2026, home insurance now accounts for approximately 9% of the average monthly mortgage payment — the highest share ever recorded. It feels expensive because it is expensive. But the alternative, in a world of $10,000 deductibles and $30 billion in annual hail claims, is catastrophic exposure.

FAQ: Common Questions About Home Insurance

What does homeowners insurance cover? Standard policies cover dwelling damage from fire, wind, hail, and other listed perils; personal belongings; liability if someone is injured on your property; and additional living expenses if your home is uninhabitable after a covered loss. Floods and earthquakes require separate policies.

How much home insurance do I need? Your dwelling coverage should equal the full cost to rebuild your home from scratch — not its market value. Personal property coverage should reflect the actual value of your belongings. Liability should be a minimum of $300,000. Verify your limits annually, not just at renewal.

What is escrow and how does it relate to home insurance? If you have a mortgage, your lender typically collects home insurance premiums as part of your monthly escrow payment. The lender then pays the insurer directly. This ensures coverage stays in force. If your premium increases at renewal, your escrow payment adjusts — often with little warning.

Is homeowners insurance required by law? No. But mortgage lenders require it as a loan condition. Without a mortgage, you’re not legally required to carry it — but going uninsured on a property worth hundreds of thousands of dollars is a risk few financial advisors would endorse.

What’s the difference between property insurance and homeowners insurance? Property insurance is a broad term that covers any insurance on physical property — commercial real estate, rental properties, land. Homeowners insurance is a specific type of property insurance designed for owner-occupied residences. It bundles dwelling, personal property, and liability coverage in one policy.

The Bottom Line

Mark eventually got his roof replaced. He paid $14,800 out of his own savings — money he’d planned to use for his kids’ college fund. The insurer followed the policy. The policy was technically fine. The problem was that Mark had never asked the right questions when he bought it.

In 2026, home insurance is not a passive purchase. The market has shifted. Costs have changed. The perils that drive losses look different than they did four years ago. The policies that were “solid coverage” in 2021 may have serious gaps today.

Check your dwelling limit against current rebuild costs. Ask whether your policy uses ACV or RCV for personal property. Look for percentage-based wind and hail deductibles buried in the declarations page. Add service line coverage before you need it.

The homeowners who come out ahead in this market aren’t the ones who found the cheapest policy. They’re the ones who read it.

About the Author

This guide was researched and written by a financial content team specializing in personal insurance, property markets, and consumer protection policy. Sources include the Insurance Information Institute, J.D. Power 2026 Claims Satisfaction rankings, California Department of Insurance regulatory filings, and publicly available industry loss data from AM Best and Verisk Analytics.

Disclosure: This article contains general educational information about home insurance. It is not legal or financial advice. Always consult a licensed insurance professional before making coverage decisions. Some links in this post may be affiliate links; we may earn a small commission at no cost to you if you use them.

Disclaimer: Coverage terms, premium ranges, and state-specific regulations described in this article reflect publicly available data as of April 2026. Insurance products vary by state and carrier. Verify current terms directly with your insurer or a licensed agent.