My coworker Karen — not her real name but she knows who she is — landed in Rome last spring with a carry-on, a fully booked itinerary, and absolutely zero international travel insurance.

She was fine with that. She’s been to Europe before. She had a decent credit card. What was the worst that could happen?

Day three, her appendix decided Rome was a good place to become a medical emergency. Surgery. Three nights in an Italian hospital. And then — the part nobody thinks about — a medical evacuation flight home because her regular doctor wanted her back stateside for follow-up.

Total bill: north of $40,000. Her US health insurance: paid almost none of it. Because her employer plan has approximately zero international coverage, which she did not know until she was lying in a hospital bed trying to figure out how to call her HR department from a different time zone.

She’s fine now. Financially it took a while.

I’m telling you this story not to scare you but because it’s the most efficient way I know to answer the question “do I really need travel insurance for an international trip.” Yes. You do. And here’s how to pick the right one.

First Thing: Does US Health Insurance Work Abroad

This is the question I get more than any other when people are planning international trips. And the answer is almost always no — or at best, barely.

Medicare? Zero international coverage. Full stop. The CDC says it clearly: Medicare will not pay for services received outside the United States. For American seniors traveling abroad, this isn’t a gap in coverage. It’s a complete absence of coverage.

Most employer-sponsored health plans are the same story. Some have limited emergency coverage abroad — like a $10,000 medical benefit that sounds okay until you realize a serious hospitalization in a Western European country can run $30,000 to $50,000 before you even think about getting home.

And medical evacuation — the cost of flying you home on a medical transport or getting you to a better-equipped hospital — that’s a completely separate cost that can hit $100,000 to $250,000 or more on its own. Your regular health insurance almost certainly doesn’t cover that at all.

So yes. When you cross the US border, your domestic health coverage basically stops working. That’s not me being dramatic — that’s the actual structure of how these plans are built. Travel health insurance abroad isn’t a nice-to-have for international trips. It’s filling a real and significant gap.

What International Travel Insurance Actually Covers

Let me just lay this out cleanly because there’s a lot of confusion about what you’re actually buying.

Emergency medical coverage. Hospital bills. Doctor visits. Medications. Diagnostic stuff. For a serious illness or injury abroad, this is the one that saves you from the Karen situation. Look for at minimum $50,000 in coverage. Ideally $100,000 or more for most international destinations.

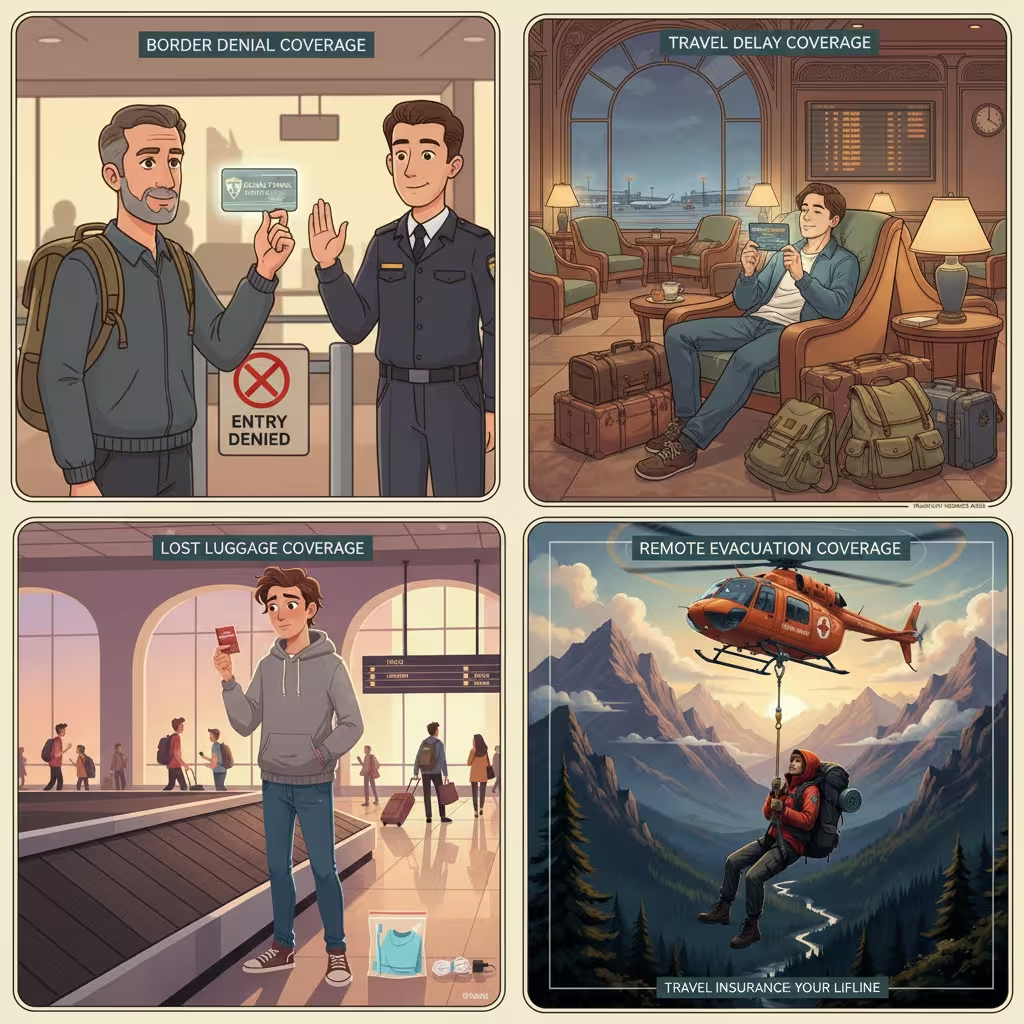

Emergency medical evacuation. Getting physically moved when you need to be. Airlifted from a remote area. Transported to a better hospital. Flown home for care. In 2026, experts recommend at least $500,000 for evacuation limits. For cruises or remote travel — Antarctica, parts of Africa, Southeast Asian islands — the recommendation goes up to $1,000,000. An airlift off a cruise ship can clear $250,000 on its own.

Trip cancellation. You paid for the trip. Something covered happens — illness, injury, death in the family, jury duty — and you can’t go. Trip cancellation reimburses those non-refundable costs. For expensive international trips this matters a lot.

Trip interruption. You’re already there when something goes wrong. You have to fly home early. This covers the extra cost of changing your flights and reimburses the unused portion of what you already paid for.

Baggage loss and delay. Airline loses your bag, or it shows up four days late. Covers essential replacements.

Travel delay. Stuck overnight because of a canceled flight. Hotel and meals while you wait.

24/7 emergency assistance. A real phone number. Real humans. Accessible from wherever you are, whatever time it is.

That’s the core package. Now let me tell you which companies actually do this well.

The Best Travel Insurance for Americans Traveling Internationally in 2026

Tin Leg Gold — Best Overall for International Trips

Tin Leg Gold is the best-selling plan on Squaremouth — the largest US travel insurance marketplace — accounting for 13% of all policy sales. That’s not a coincidence.

What makes it stand out for international travel specifically: it offers primary medical coverage, which means when you show up at a hospital abroad, Tin Leg pays first. You don’t have to go through your useless-internationally domestic plan and get a denial before Tin Leg will act. Primary coverage is the standard you want for overseas travel insurance, and Tin Leg Gold has it.

Medical evacuation limits go up to $500,000. That’s double what a lot of plans offer. For serious international travel — not a weekend in Cancun but a real trip to places with real medical infrastructure gaps — that limit matters.

They also use a 60-day lookback period for the pre-existing condition waiver, which I’ll explain in a minute because it’s important.

Seven Corners Trip Protection Choice — Best for Medical Limits

If evacuation limits are your main concern — and they should be if you’re going anywhere remote — Seven Corners Trip Protection Choice goes up to $1,000,000 for medical evacuation. That’s the benchmark number recommended for extreme or remote travel in 2026.

They also offer Interruption For Any Reason (IFAR) as an add-on. That’s rarer than Cancel For Any Reason and honestly underappreciated. IFAR lets you cut a trip short for any reason — not just covered reasons — and still get partial reimbursement for what you didn’t use. For people who travel to unstable regions or have unpredictable work schedules, that flexibility is real.

Travelex Insurance Services — Best for Families

Travelex is the name that keeps coming up when families are the focus. Their structure is built around multi-person coverage in a way that makes the math work better for groups.

They’re also one of the top-rated overall for 2026 based on financial stability and coverage depth. Not the cheapest. But for a family planning a significant international trip where something going wrong would be genuinely expensive, Travelex’s reputation and coverage structure earns the premium.

Travel Insured International FlexiPAX — Best for Multi-Generational Groups

This one is specific but important. FlexiPAX allows one adult to cover up to nine children under 18 at no additional cost. For multi-generational family trips — grandparents, parents, multiple kids — this structure saves real money versus plans that charge per child.

It also offers primary medical coverage, which as I mentioned above is what you want for international travel.

For anyone coordinating a big family international trip, this plan deserves a serious look before you start adding up per-person premiums at other companies.

Allianz Travel Insurance — Best for Seniors and Annual Plans

American seniors are in a genuinely unique situation when it comes to international travel insurance. Medicare stops at the border. Period. So for anyone 65 and up traveling internationally, travel health insurance abroad isn’t optional — it’s the only coverage they have.

Allianz stands out here for two reasons. First, they have no maximum issue age on many of their plans — a lot of insurers start declining or severely limiting coverage above 75 or 80. Second, their IMG GlobeHopper Senior program is specifically designed for Medicare-eligible travelers as supplemental international coverage.

For seniors doing multiple international trips a year, Allianz’s annual multi-trip plans are worth the math. You pay one flat premium and you’re covered for every trip you take over 12 months, up to a per-trip day limit. For someone doing two or three international trips a year, the annual plan usually wins on cost versus buying separate policies every time.

Trawick International — Best Value / Most Affordable

Here’s the honest budget answer. Trawick International’s Safe Travels Voyager plan consistently benchmarks $4 to $16 below the industry average for basic comprehensive coverage. For younger travelers or trips where the total non-refundable costs are lower, Trawick is where the affordable overseas travel insurance conversation usually starts.

Not the highest limits. Not the most add-ons. But solid, reliable coverage at a price point that makes sense for budget-conscious international travelers.

IMG iTravelInsured Travel LX — Best for Pre-Existing Conditions

If you or anyone on your trip has a pre-existing medical condition, this is the conversation you need to have before you pick any policy.

IMG’s iTravelInsured Travel LX is specifically built for this. Medical limits go up to $1,000,000 on certain tiers. They use a 60-day lookback period for the pre-existing condition waiver. And they have a strong track record with the senior and health-compromised traveler segment specifically.

Speaking of which — let me explain the waiver thing because it’s the most misunderstood part of international travel insurance.

The Pre-Existing Condition Waiver — Read This Part

This is the thing that catches people off guard more than almost anything else in travel insurance. Especially for international trips where the medical stakes are higher.

Most standard travel insurance policies exclude pre-existing conditions. Meaning if you have diabetes and something diabetes-related happens on your trip — that could be denied.

But. If you buy your policy within 10 to 21 days of your first trip deposit — that’s the time-sensitive window, also called the golden window — you can qualify for a pre-existing condition waiver. This waiver basically erases the exclusion. Your pre-existing conditions are covered as if they were anything else.

Miss that window? The insurer uses a lookback period — usually 60 to 180 days before you bought the policy — to check your medical history. If anything changed during that window (new prescription, new diagnosis, new symptom, pending test), anything related to that is excluded.

So here’s the practical rule: the same day you make your first trip payment — flights, hotel deposit, tour booking, whatever — that’s the day you should be thinking about buying travel insurance. Not a month before departure. The day you book.

Two specific things to know about the waiver:

First — if your condition has been stable for 60 days (no change in medication, no new symptoms, no pending tests) before you buy, some plans like Tin Leg Gold and IMG iTravelInsured may not even classify it as pre-existing. Worth checking.

Second — CFAR, the Cancel For Any Reason upgrade, also has to be purchased within that same early window. So if you want both the pre-existing waiver and CFAR, buying early is doubly important.

How Much Does International Travel Insurance Cost for Americans

Let me give you real numbers from 2026 data instead of vague percentages.

For a $5,000 trip:

- Ages 20 to 50: around $197, roughly 3.9% of trip cost

- Age 65: around $394, about 7.9% of trip cost

- Age 75: around $552, about 11% of trip cost

For a $10,000 trip:

- Ages 20 to 50: around $360, roughly 3.6%

- Age 65: around $720, about 7.2%

- Age 75: around $1,100, about 11%

International coverage runs about 22% more expensive than domestic coverage on average. The destination also matters a lot. Travel to regions with limited medical infrastructure or where evacuation costs are high — parts of Africa, remote islands, Antarctica — can push premiums significantly higher because the potential evacuation cost is much higher.

For most Americans visiting Europe, the basic benchmark is somewhere in the 4% to 8% of total trip cost range. And for that, you’re getting medical coverage that your actual health insurance doesn’t provide at all internationally.

The New Stuff That’s Changed in 2026

A few things are genuinely different this year compared to even a couple years ago, and they’re worth knowing.

AI has made claims way faster. The old timeline for a claim was 30 days average. In 2026, AI-assisted claims resolution averages 7.5 days. Some straightforward claims process in minutes. That matters when you need money to rebook a flight or pay a hospital and you can’t wait a month.

Smart contracts are a real thing now. About 15% of European insurers and a growing slice of US providers use blockchain-based contracts for flight delays. The system monitors your flight data in real-time. If your delay hits six hours, a reimbursement automatically gets triggered to your mobile wallet before you’ve even asked for it. No receipts. No form. Just money.

Border denial coverage is emerging. This is new and niche but relevant. Some top-tier 2026 plans now cover you if you’re denied entry at a destination’s border because of an unexpected change in visa or entry requirements. Countries like Thailand and Costa Rica have had entry requirement changes that caught travelers off guard. This coverage is not standard yet but it’s growing.

The evacuation limit standard has gone up. Old recommendation was $50,000 for medical evacuation. That number is now dangerously insufficient. The 2026 recommendation is $500,000 minimum for most international travel. For remote or adventure travel, $1,000,000. A cruise ship airlift alone can run over $250,000.

Is the Cheapest International Travel Insurance Actually Worth It

Here’s my honest take on this.

For a young, healthy traveler going to a country with good medical infrastructure — Western Europe, Japan, Canada — a budget plan from Trawick might genuinely be the right call. You’re mainly covering cancellation costs and getting the medical coverage your US plan doesn’t provide. You don’t need $1,000,000 evacuation limits for a trip to Amsterdam.

But for anyone over 60, anyone with health conditions, anyone going somewhere genuinely remote, or anyone with significant non-refundable trip costs — cheap is the wrong frame. The question isn’t “how little can I spend” — it’s “what’s the minimum coverage that actually protects me.”

Medical evacuation from Southeast Asia to the US: $100,000+. From parts of Africa: $200,000+. From Antarctica: over $500,000. The cost of the insurance that covers these things is a few hundred dollars. The math is not complicated.

Go cheap on the trip cancellation limits if you want. Don’t go cheap on emergency medical and evacuation.

What to Actually Check Before You Buy

Quick checklist. Run through this before you click purchase on any international travel insurance plan.

Does it have primary medical coverage? If you’re traveling internationally, you want primary. Not secondary.

What are the medical limits? Minimum $50,000. Better: $100,000. For adventure or remote travel: $250,000+.

What are the evacuation limits? Minimum $100,000. Better: $500,000. For remote travel: $1,000,000.

Does it cover pre-existing conditions — and did you buy it within the time-sensitive window?

Does your destination have specific requirements? (Europe’s Schengen area doesn’t mandate travel insurance for US citizens, but some countries require specific minimum coverage for certain visa types.)

What’s the AM Best rating of the underwriter? Stick to A- or better. Top underwriters in 2026 include Berkshire Hathaway Specialty, Zurich American, and United States Fire Insurance.

Frequently Asked Questions – FAQ’s

- What is international travel insurance?

It provides coverage for medical emergencies, trip cancellations, lost luggage, and other travel-related risks while abroad. - Do I need travel insurance for international trips?

While not always mandatory, it’s highly recommended for financial protection and peace of mind during unforeseen events. - What does international travel insurance cover?

Coverage typically includes medical emergencies, trip cancellations, delays, lost luggage, and emergency evacuations. - How much does international travel insurance cost?

Costs vary based on trip length, destination, age, and coverage type, averaging 4-10% of the trip cost. - Can I get coverage for pre-existing conditions?

Yes, many policies offer waivers for pre-existing conditions if purchased within a specific time frame. - Is travel insurance mandatory for international travel?

Some countries require it for entry, but it’s generally optional unless specified by your destination or tour operator. - What is CFAR (Cancel For Any Reason) coverage?

CFAR allows you to cancel your trip for any reason and get partial reimbursement, usually up to 75%. - How do I choose the best travel insurance?

Compare policies based on coverage, exclusions, cost, and reviews to find one that suits your needs. - Does travel insurance cover COVID-19?

Most policies now include COVID-19 coverage for medical expenses and trip interruptions, but check specifics. - When should I buy travel insurance?

Purchase it as soon as you book your trip to maximize benefits like cancellation and pre-existing condition waivers.

The Bottom Line

International travel insurance for US citizens isn’t a luxury product. It’s gap coverage — filling the enormous hole left by the fact that American health insurance basically stops working the moment you leave the country.

About 50% of Americans now buy travel protection before international trips. And 65% say they consider it a critical requirement. That number has been climbing every year since 2020 and it’s not slowing down.

The global market for this stuff is $35.82 billion right now. It’s headed for $53 billion by the early 2030s. It’s growing because people are learning — usually the hard way, like Karen — that the cost of not having it is so much higher than the cost of having it.

Buy it early. Check the medical limits. Make sure evacuation is real and not capped at some number that an airlift would blow past in the first hour.

And for the love of all things travel — don’t show up in Rome thinking your employer health plan has you covered.

It doesn’t.

Disclaimer: This article is for informational purposes only and is not insurance, financial, or legal advice. Coverage terms, pricing, and provider offerings vary. Always review your complete policy documents and consult a licensed insurance professional before purchasing.