Last Updated: April 2026

Marcus thought he had it figured out.

Thirty-eight years old, two kids, a mortgage in Columbus — he found a term life policy for $22 a month, set up autopay, and moved on. Checked the box. Done.

Three years later he got married. Tried to update his beneficiary. Logged in and found… nothing. His bank account had changed when he switched jobs, the payment quietly failed, and nobody — not the insurer, not his agent — called to say the policy lapsed.

Gone.

That’s the thing people don’t tell you about life insurance. The buying part is easy now. It’s the staying covered part that trips people up. And when your family actually needs it, there’s no going back to fix a mistake you made on a Tuesday afternoon three years ago.

This guide is for Americans who want to get this right. First-timers. People who already have a policy and aren’t sure what’s actually in it. Anyone who’s been told to “just get term” and wants to know if that advice holds for their situation. We’ll cover cost, coverage, the companies worth trusting, and the products that sound better than they are.

Disclosure: Some links in this guide are affiliate links. If you click and buy, we may earn a small commission. It doesn’t change what we recommend or why.

Why 2026 Is a Different Kind of Year for Life Insurance

The U.S. life insurance market just came off its biggest year on record. According to LIMRA, total new premiums hit $17.5 billion in 2025 — a 10% jump and the fourth record in five years. Sales are up. Awareness is up.

And still, millions of households are flying without a net.

Part of that is cost. Part of it is confusion. Honestly? Part of it is that the industry has gotten so good at making the buying process fast and frictionless that people click through without really reading. Getting approved in 10 minutes feels like a win — until you realize the coverage amount was a number you pulled from thin air.

Growth is expected to slow to 2%–6% in 2026, as inflation continues squeezing household budgets. Carriers are shifting — less “sign everyone up,” more “keep who we have.” What that means for buyers: there’s more competition on price right now than there’s been in years.

Good time to shop.

Term vs. Whole Life Insurance — Let’s Be Honest Here

Everyone has an opinion on this debate. Most of those opinions are too simple.

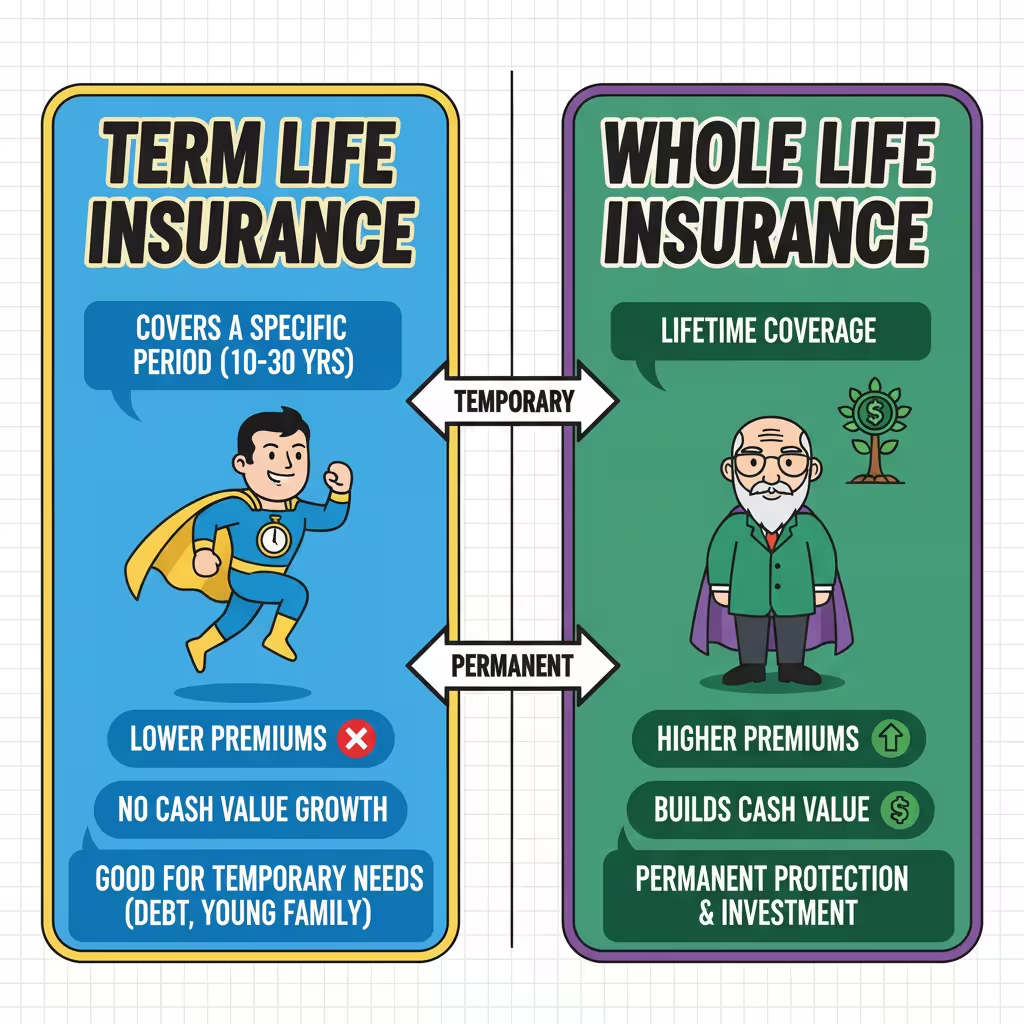

Term life insurance is exactly what it sounds like. You pick a term — 10, 20, or 30 years — pay a fixed monthly premium, and if you die within that window, your beneficiary gets the death benefit. If you outlive the policy, it expires. No payout, no cash back. Pure protection.

Whole life insurance never expires. Pay your premiums and you’re covered for life. It also builds cash value over time — a growing account you can borrow against, use to cover premiums, or pass as part of your estate.

Price difference? Meaningful. A healthy 30-year-old can get a $500,000 20-year term policy for around $25–$30 a month. The same death benefit in whole life? Often $200–$400 a month or more.

So term wins automatically, right?

Not so fast.

Statistically, around 99% of term policies never pay out a death claim — because most people outlive the coverage window. That’s not a reason to skip term. But it does mean that if you’re 58 when your 20-year term expires, you’re starting over. At 58. Probably with some health changes. At much higher rates. Some people can’t qualify at all anymore.

Whole life doesn’t have that problem. It pays out. Guaranteed. And for someone using the cash value component strategically — retirement supplementation, estate transfer, business planning — it’s not the overpriced product critics say it is.

My honest take: if you’re under 40, have dependents, and budget is tight, start with term. Lock in the coverage now, lock in a low rate, revisit in a decade. If you’re 50-plus and thinking about final expenses or what you leave behind, whole life deserves a real conversation — not an automatic dismissal.

Best Life Insurance Companies in 2026

Rankings are based on AM Best financial strength grades, NAIC complaint ratios (lower = better), and customer satisfaction data from 2025 surveys.

Note: Some links below are affiliate links. We only recommend carriers we’d point a family member toward.

| Rank | Company | Score | Why They Stand Out |

| 1 | Northwestern Mutual | 4.64 | Lowest complaint ratio in study (0.040); A++ AM Best |

| 2 (tie) | Guardian Life | 4.59 | Consistently high trust scores; top-tier financials |

| 2 (tie) | New York Life | 4.59 | Best document access; A++ rating |

| 4 (tie) | Mutual of Omaha | 4.56 | Highest customer satisfaction; strong for seniors |

| 4 (tie) | Pacific Life | 4.56 | Premiums roughly 27% below the industry average |

Northwestern Mutual’s complaint ratio of 0.040 is the number that jumps out. Most major carriers run between 0.1 and 0.3. Getting to 0.040 means the overwhelming majority of customers move through the entire claims experience without a dispute. That’s not marketing. That’s operations.

For buyers watching their budget, Pacific Life keeps coming up. Average premiums well below industry norms, strong financial ratings. That combination is genuinely rare — usually you’re trading one for the other.

Corebridge Financial and Transamerica offer some of the lowest raw monthly rates in the market. But they carry higher complaint volumes. Read recent reviews if you go that direction. Know what you’re trading.

One more worth noting: Amica. In recent surveys, 100% of customers said they planned to keep their coverage. That kind of retention doesn’t happen accidentally.

How Much Life Insurance Coverage Do You Actually Need?

Most advice starts with a formula: 10 to 12 times your annual income.

Earn $70,000? Aim for $700,000–$840,000.

Reasonable starting point. Misses a lot.

A better calculation looks at what your family would actually face:

- Income replacement — How many years would they need to maintain their lifestyle without your paycheck?

- Mortgage balance — Would they be able to keep the house?

- Debt — Car loans, credit cards, student loans don’t disappear

- Kids’ education — College costs keep climbing

- Final expenses — This one surprises people. Funeral and burial costs jumped 14.2% since 2024. California now averages $11,500. Parts of Florida have passed $12,800. Texas runs around $9,200, though Houston metro projections push closer to $12,450.

Run those numbers with your real figures. Most people discover they’re underinsured. Sometimes significantly.

The formula is a floor, not a ceiling.

Life Insurance With No Medical Exam — Who Should Use It

No-exam coverage has improved a lot. The old version was an expensive, low-limit fallback for people who couldn’t qualify otherwise. What’s available now is different.

Simplified issue underwriting skips the physical entirely. No blood draw, no appointment, no waiting weeks for a paramedic to show up at your house. Insurers run your information against real-time prescription databases and detailed health questionnaires. Approval often comes in 24 to 48 hours.

Two groups benefit most from this route.

Seniors who’ve developed health conditions that make traditional underwriting difficult or impossible. And buyers who need coverage fast — just had a kid, closing on a house, starting a new job with dependents — and can’t wait six weeks for standard processing.

The trade-off is real. No-exam policies cost more per dollar of coverage than fully underwritten ones, and limits typically cap somewhere between $25,000 and $500,000 depending on the carrier.

If you’re healthy and under 50, fully underwritten will almost always beat simplified issue on price over time. But if speed or medical history is the constraint right now, no-exam is a legitimate path — not a consolation prize.

The IUL Problem Nobody Mentions Until It’s Too Late

Indexed Universal Life insurance — IUL — had a breakout year in 2025. Premiums jumped 17%. Agents are selling it hard. Ads are everywhere.

The pitch sounds almost too good. Your cash value grows linked to a market index like the S&P 500. If markets rise, you participate. If they crash, a “0% floor” shields your principal. Upside with no downside.

Here’s what the brochure leaves out.

Monthly charges run against your cash value no matter what the market does. Administrative fees. Cost of insurance — which climbs every year as you age. Those charges don’t pause in flat years. They don’t pause in zero-return years.

Picture this: you’re 67, retired, taking withdrawals from your IUL to supplement Social Security. The market goes flat two years in a row. Your policy earns nothing. Charges keep running. Withdrawals keep coming out. Cash value drops. At some point the insurer may require you to put more money in just to keep the policy alive.

That’s called sequence of returns risk. The timing of gains and losses matters more than the average return. A clean illustration showing steady 8% per year looks reassuring. Real markets don’t work that way.

IUL caps have also declined significantly — from roughly 13% fifteen years ago down to around 8% today. That limits how much of the market’s upside actually reaches your policy.

The NAIC is currently pushing to restrict illustrated returns above 10%. If an agent shows you a projection built on double-digit assumptions, ask for the conservative scenario. If they hesitate or push back — leave.

IUL can work. For certain people. With specific goals. With full understanding of the mechanics. But it gets sold too casually to people who think they’re buying something simple. It isn’t.

What Changed in 2026: Tax Laws and New Rules

The One Big Beautiful Bill Act — signed into law in 2026 — made a permanent change to federal estate planning that high-net-worth families should understand.

The federal estate and gift tax exemption now sits at $15 million per individual. For married couples, that’s $30 million they can transfer without federal estate taxes. Starting in 2027, it adjusts annually for inflation. Amounts above the exemption are still taxed at 40%.

For most American families, this doesn’t dramatically change day-to-day insurance planning. But for anyone with a business, real estate portfolio, or investment accounts that could push an estate past those numbers — this is an important window. Life insurance death benefits are generally received income-tax-free by beneficiaries under IRS Section 7702 rules. A well-structured permanent policy becomes a real wealth transfer tool in this context.

Texas residents got a separate win this year. Under House Bill 2067, effective January 1, 2026, insurers must automatically provide written explanations if your home or auto policy is declined, canceled, or not renewed. You don’t have to ask. They have to tell you why. Took long enough.

Cheapest Life Insurance for Young Adults — And Why This Window Closes Fast

If you’re in your mid-20s or early 30s, one thing is true about life insurance that isn’t true about much else in personal finance: waiting costs you real money, locked in permanently.

The younger and healthier you are when you apply, the lower your monthly premium — and that rate is fixed for the entire term. A 25-year-old in good health can lock in a $500,000 30-year term policy for under $25 a month with several strong carriers. Wait until 35 and that same policy runs $35–$45. Wait until 45 and you’re often looking at $80 or more, sometimes much more depending on what health conditions have developed.

The cheapest life insurance for young adults isn’t the policy with the lowest quote on some comparison site. It’s the policy you buy while you’re still cheap to insure, from a company that’ll still be around in 30 years, with payments tied to an account you won’t close by accident.

Four things to do if you’re in this group:

- Get quotes from at least two top-rated carriers — rates vary more than most people expect

- Pick a 30-year term if you have young kids — match the term to your actual financial obligation window

- Name beneficiaries with specifics, not “my estate”

- Set a recurring January reminder to log in and confirm the policy is active

That last one is exactly what Marcus skipped.

Frequently Asked Questions

How much does life insurance cost per month? Depends on age, health, coverage amount, and policy type. A healthy 30-year-old can get a $500,000 20-year term policy for around $25–$32/month. The industry average runs about $382/year for that same policy. Shop at least two or three carriers — pricing varies more than most people realize.

What are the best life insurance companies for seniors in 2026? Mutual of Omaha and Pacific Life both rank well. Mutual of Omaha earned the top customer satisfaction marks in recent surveys and covers final expense whole life solidly. Pacific Life’s premiums average roughly 27% below industry norms — that matters a lot on a fixed income.

Is term or whole life insurance better? Neither is universally better. Term is cheaper and works well for income replacement during working years. Whole life costs more but lasts your entire life and builds cash value. Most younger buyers with tight budgets start with term. Many revisit whole life in their 50s.

Can I get a life insurance policy with no medical exam? Yes. Simplified issue policies skip the physical and use health questionnaires plus prescription database checks instead. Approval often takes 24–48 hours. Premiums run higher than fully underwritten coverage and limits are lower, but for seniors or buyers who need coverage quickly, it’s a real option.

How much life insurance do I need? Start with 10–12 times your annual income. Then add your mortgage balance, outstanding debts, projected education costs, and current final expense costs in your area. Most people find they’re underinsured when they run the actual numbers.

What’s the real risk with IUL insurance? Sequence of returns risk is the one that catches people off guard — poor market timing during retirement can deplete your policy even with a 0% floor, because monthly charges keep running. Caps have dropped from ~13% to ~8% over 15 years. Don’t buy based on an illustration using double-digit return projections.

How does the OBBBA affect life insurance planning in 2026? The One Big Beautiful Bill Act raised the federal estate tax exemption to $15 million per person ($30 million for couples). Since life insurance death benefits are generally income-tax-free to beneficiaries, permanent policies become a useful wealth transfer vehicle for larger estates.

Marcus Got His Coverage Back. It Cost Him More.

He reapplied at 41 and qualified — but at higher rates. Three years older. Slightly elevated blood pressure. One more flag in the health questionnaire. The policy he should’ve had all along now costs him about $14 more a month than it would have.

He also set a January calendar reminder. Every year. Log in. Confirm active. Check beneficiaries.

He got lucky. Most families don’t find out there’s a problem until they’re trying to file a claim.

The right life insurance isn’t the one with the lowest number on a comparison site. It’s the one that’s still active when your family needs it. The one backed by a company strong enough to pay without a fight. The one with a coverage amount calculated from your real life — not a round number that felt reasonable in the moment.

Go get that policy. Or pull up the one you already have and make sure it’s what you think it is.

Your family will never know you did this. That’s the whole point.

About the Author

Selene Voss is a personal finance writer with 8 years covering insurance, estate planning, and consumer financial products for U.S. households. She has reviewed policy documents and pricing data across dozens of major American carriers and contributed to [publication names]. [Optional: Specializes in helping first-time buyers and families near retirement understand what their coverage actually covers.]

This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Premium rates, coverage limits, and regulatory details vary by state and individual circumstances and may have changed since publication. Consult a licensed insurance professional before purchasing or changing any policy.