Last Updated: April 2026

My cousin called me on a Thursday night, kind of panicked.

Not like emergency panicked. More like “I just realized something and I don’t know what to do about it” panicked. He’s 42. Works in logistics. Has a wife, three kids, a mortgage he refinanced in 2021. And he’d just gotten a letter in the mail saying his term life insurance policy was expiring in 90 days.

He’d bought it when his oldest was born. Ten-year policy. $300,000. Totally forgot about it.

“Is that bad?” he asked me.

I asked him how much his mortgage was. How much he made. How old his kids were.

The math took about four minutes. His family would run out of money in roughly 18 months if he died tomorrow. The $300,000 sounds like a lot until you hold it up against a $240,000 mortgage balance, three kids who need years of support, and a wife who’d stepped back from full-time work.

Yeah. It was bad.

And the thing is — he’s not careless. He bought coverage when he was supposed to. He just bought it once, filed it away, and assumed the job was done. That’s exactly what most Americans do with term life insurance.

So this guide is for my cousin. And honestly, probably for you too.

Heads up: A few links in this post are affiliate links. If you buy through them, we get a small commission — costs you nothing extra. Doesn’t change what I recommend.

Okay, First — What Even Is Term Life Insurance?

I’ll keep this part short because it really isn’t complicated.

You pay a monthly premium. You pick how many years you want coverage — usually 10, 15, 20, or 30. If you die during that window, the insurance company pays your family a lump sum called the death benefit. That money comes to them tax-free. Fast. Usually within days of a valid claim.

If you’re still alive when the term ends? Nothing happens. Coverage just stops. No check. No refund. You don’t get anything back.

That sounds like a raw deal on the surface. But here’s the thing — term life insurance isn’t supposed to pay out most of the time. It’s there for the worst-case scenario. And because it’s so simple — no fancy savings component, no investment account quietly running in the background — the monthly cost is genuinely low.

Like, shockingly low compared to other options.

A healthy 30-year-old can get $500,000 of coverage for a 20-year term for around $25–$30 a month. A whole life policy with the same death benefit? Often $300–$350 a month. Same payout if you die. More than ten times the price. The reason is that whole life builds something called cash value — an equity component — and you’re paying for that on top of the insurance. With term, you’re paying for one thing: the death benefit. Nothing else.

For most working families with a mortgage, kids at home, and a real monthly budget — term life is where you start.

What Does Term Life Insurance Actually Cost?

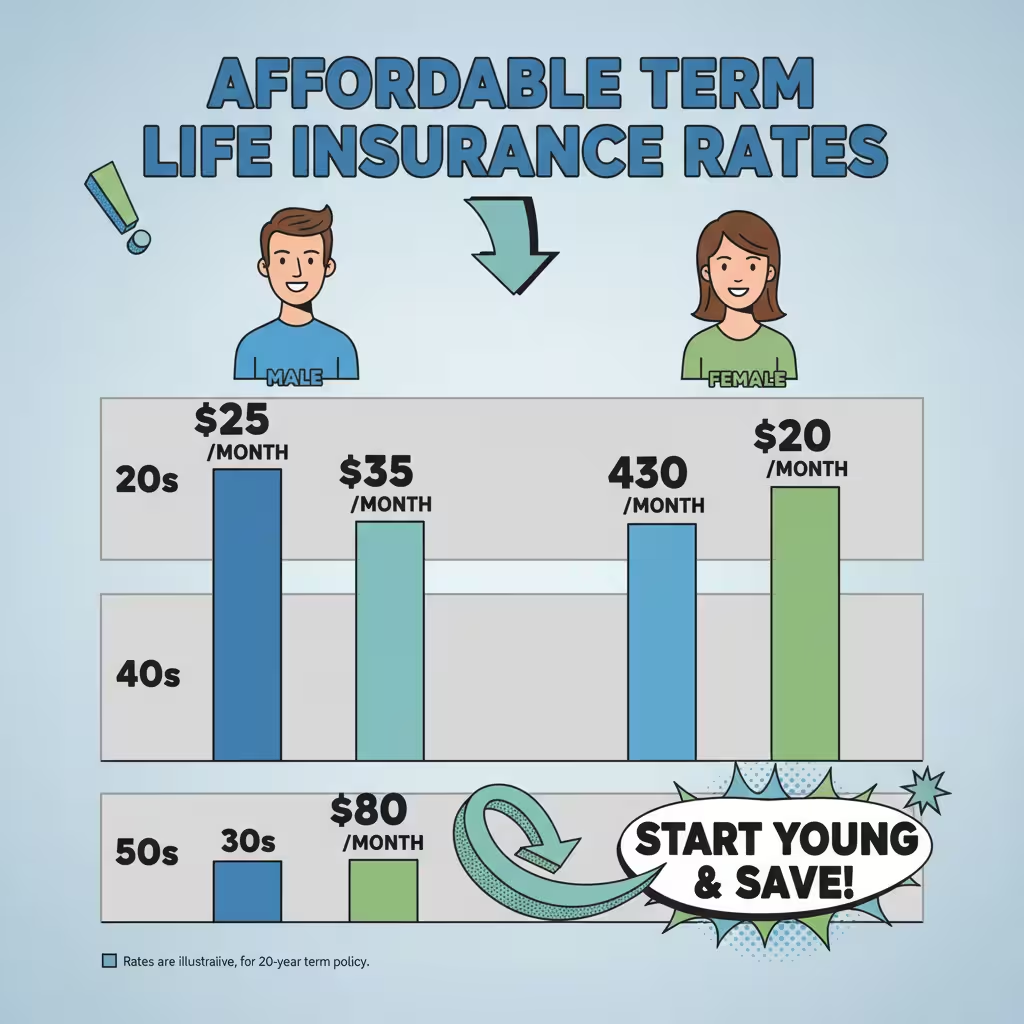

Let me give you real numbers because vague ranges are useless.

These are rough monthly rates for a $500,000 20-year term policy in 2026, for non-smokers:

| Age | Male | Female |

| 25 | ~$22/mo | ~$18/mo |

| 30 | ~$25/mo | ~$21/mo |

| 35 | ~$30/mo | ~$25/mo |

| 40 | ~$45/mo | ~$36/mo |

| 45 | ~$70/mo | ~$55/mo |

| 50 | ~$110/mo | ~$85/mo |

A few things jump out at me every time I look at that table.

The jump between 30 and 40 is $20 a month. That’s $240 a year. Over a 20-year policy, that’s $4,800 in extra premiums — for the exact same coverage. Every year you wait past 30 costs you real money, permanently locked in for the life of the policy.

Smoking is brutal on rates. Smokers pay roughly double or triple what non-smokers pay at every age. And if you quit recently — within the past year — most insurers still classify you as a smoker. You need to be smoke-free for at least 12 months, ideally 24, before applying. The difference in monthly premium is worth waiting for.

For a 40-year-old male non-smoker — which is one of the most common searches I see — $500,000 of 20-year term coverage runs about $40–$55 a month depending on the carrier and which health tier you fall into. That’s not bad money for half a million dollars of protection.

One more thing on rates: shop around. Seriously. I know that sounds obvious but most people just go with whoever their agent works for. Rates for the exact same applicant can vary by 20–30% between carriers. An independent broker who has access to multiple insurance companies at once can find you the best rate without you having to call five different places yourself.

The Four Kinds of Term Life — One of Them Is Hugely Overlooked

Most people don’t realize term life isn’t just one thing. There are actually four structures, and each one works differently.

Level term is the standard. Your premium stays the same for the whole period. Your death benefit stays the same. Lock in at 33 and you’re paying the same amount at 52 with the same coverage. That’s the one most families should buy.

Annual renewable term works differently — coverage renews each year and the price goes up a little every year as you age. It starts cheap but gets expensive over time. This one makes sense if you need a short gap covered — like a year or two while you’re waiting for something else to settle. Not great as a long-term plan.

Decreasing term is built for a specific purpose. The death benefit shrinks over time — usually designed to run alongside a declining mortgage balance. Premium is roughly flat but you’re getting less and less coverage as years pass. Too narrow for most families who need flexible protection, not just mortgage coverage.

Convertible term — and this is the one I think gets nowhere near enough attention.

A convertible term policy has a clause that lets you switch to a permanent policy later without a new medical exam. No new health questions. No new blood work. Whatever health rating you got when you bought the term policy? That carries over.

Why does that matter so much?

Because you might be 34 and perfectly healthy when you buy. Then at 48 you get a Type 2 diabetes diagnosis. Or high blood pressure. Or something more serious. Without convertibility, you either can’t get permanent coverage at all or you’re paying two to three times more for it. With the convertibility clause, you can switch regardless of what’s happened to your health in the years since.

Most good term policies include convertibility at no extra charge or for a minimal add-on cost. But always confirm before you sign. Ask your agent specifically: “Does this policy let me convert to permanent coverage without new underwriting, and until what age?”

Shopping for a 20-Year Term Policy: What to Actually Pay Attention To

A 20-year term is the most popular option in the country and there’s a reason for that. It covers the years when your financial obligations are highest — the mortgage decade, the raising-kids years, the stretch where your income disappearing would be genuinely catastrophic.

When you’re comparing policies, the monthly premium is the last thing I’d lead with. Here’s what I’d actually look at first.

The carrier’s financial strength rating. You can look these up at AM Best. Target at least an A rating. This company is making a 20-year promise to your family. You want them still standing — and paying — two decades from now.

The complaint ratio. The NAIC publishes data on how many formal complaints each insurer receives relative to their market share. A low number means customers aren’t fighting to get claims paid. That’s more revealing than any slick advertisement.

Living benefits. A lot of modern term policies include what’s called an accelerated death benefit — if you’re diagnosed with a terminal illness while the policy is active, you can pull forward part of the death benefit while you’re still alive. Some carriers include this at no extra cost. Worth asking about.

And convertibility. Already said it above — confirm it’s in there.

Then look at price.

My Cousin Had One More Question: What Happens When the Policy Expires?

He asked this and I could tell he was hoping the answer was “nothing, you’re fine.”

It’s not nothing.

When a term policy ends, you’ve got a few choices.

You can let it lapse. If you no longer have a mortgage, your kids are grown and financially independent, and you’ve built up retirement savings that could cover your own final expenses — letting it lapse is genuinely fine. You used the coverage during the years it mattered. That’s exactly what term insurance is supposed to do.

You can renew it year by year. Most policies allow this without a new medical exam. The downside: your premium resets to your current age. A 60-year-old renewing a policy they first bought at 40 can easily pay four or five times the original monthly rate. Fine for a year or two of bridge coverage. Brutal as a long-term plan.

You can convert it. If your policy is convertible, this is usually the best move for someone who still needs permanent coverage. Your original health rating carries over, you don’t answer new health questions, and you get lifelong coverage without going back through underwriting.

Or you can apply for a brand new policy. Possible if you’re still healthy when the old one expires. But you’re older now, rates are higher, and anything that’s changed with your health over the past 10–20 years becomes a factor again.

Here’s the thing I told my cousin that he actually wrote down: put the expiration date in your phone calendar right now. Then set another reminder five years before that date. That five-year window is when you evaluate, convert, or replace — not the 90-day panic window he found himself in.

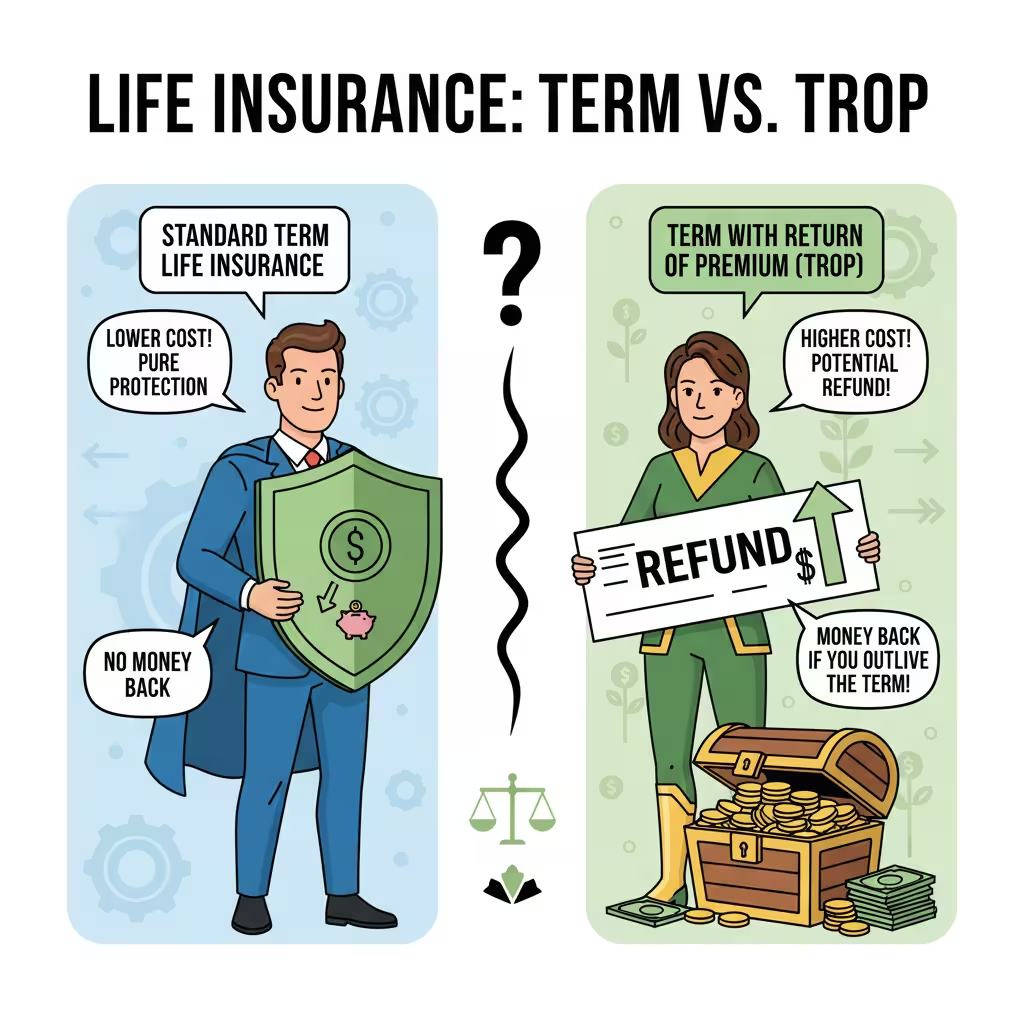

A Word on Term With Return of Premium

There’s a version of term called TROP — term with return of premium — where you get all your paid premiums refunded if you outlive the policy.

Sounds like the obvious choice, right? Heads I win, tails I break even?

The reality is messier. TROP premiums run about 50–75% higher than standard term. The refund you get at the end is exactly that — a refund of your overpayment, with no interest added. The insurer held your extra money for 20 years, invested it, and hands back the principal.

If a 35-year-old bought standard term for $30/month and TROP for $50/month, that $20 difference invested in a basic index fund at historical average returns would likely outgrow the premium refund before the 20 years is even up.

So the math generally favors buying regular term and investing the difference.

But here’s what I’ve seen in real life: most people don’t invest the difference. They just spend it. For those people, TROP works as a sort of forced savings — you overpay, and the refund feels like found money two decades later. Not the ideal financial move, but not a terrible outcome either.

Whether it makes sense depends less on the math and more on honest self-knowledge about your own habits.

The Tax Law Change That Affects How You Think About This

In July 2025, Congress passed the One Big Beautiful Bill Act — the OBBBA. It made the federal estate tax exemption permanent at $15 million per person, or $30 million for married couples. That adjusts for inflation starting next year.

For the average American buying a $500,000 term policy to protect a mortgage and replace income — this doesn’t change your core decision much.

But it matters if you’ve been holding large permanent life policies specifically to cover estate taxes. That strategy may now be oversized. With fewer estates facing federal estate tax liability at all, some policies bought for that purpose might need to be reconsidered or restructured.

The law also put more money in ordinary workers’ pockets through things like overtime deductions and expanded standard deductions — $31,500 for joint filers. More take-home income means more households can actually afford the right coverage amount rather than buying whatever barely fits.

Questions I Get Asked All the Time

So how does term life insurance actually work, in plain English?

You pay monthly. If you die during the coverage period, your family gets a tax-free lump sum. If you outlive it, the policy ends and nothing happens. No cash value, no refund, no investment. Pure death benefit coverage.

What are realistic 20-year term life insurance rates in 2026?

For a healthy 30-year-old non-smoker: $20–$30/month for $500,000. For a 40-year-old male non-smoker in standard health: $40–$55/month for the same coverage. Rates vary meaningfully by carrier — shop at least three before deciding.

Is 40 too old to buy term life insurance?

No. A 40-year-old male non-smoker can still get solid coverage at reasonable rates. The mistake most people make at 40 is buying too little to keep the premium low. Don’t do that. Calculate what your family actually needs — mortgage, income replacement, kids’ support years, final expenses — and buy that number, not a round figure that felt manageable.

What happens at the end of a term life policy?

Coverage stops. You can let it go, renew annually at a much higher rate, convert to permanent coverage if your policy allows it, or apply for new coverage. Build a five-year runway before expiration so you’re making this decision with options, not under pressure.

What is level term insurance?

Level term means your premium and death benefit stay the same for the full policy period. The most common and most straightforward structure. What most people should buy.

Is a convertible term policy actually worth it?

For most people, yes. Health can change in 20 years in ways you can’t predict. Convertibility lets you lock in a permanent policy later at your original health rating. Most policies include it at little or no extra cost. Always verify before signing.

My Cousin Got a New Policy. Here’s What It Took.

He called an independent broker the next day. Got quotes from four carriers. Bought a new 20-year level term policy — $750,000 — for $53 a month. Made sure it was convertible. Updated his beneficiaries while he was at it because the old ones were still set to his parents from a decade ago.

The whole thing took about two hours across two days.

He was embarrassed it took a panicked phone call to get there. But honestly, that’s how most of these things work. Nobody wakes up thinking “I should really review my life insurance today.” Something rattles you — a letter, a health scare, a conversation with someone who ran the math — and then you move.

Consider this your something.

If you don’t have a policy, get quotes today. If you have one, find the expiration date. Run the real numbers on whether the coverage still fits your actual life — not the life you had when you bought it.

Your family’s situation has probably changed more than you think.

About the Author

Selene Voss is a personal finance writer with 8 years covering life insurance, consumer financial planning, and U.S. tax legislation. She has reviewed policy pricing and structures across dozens of major U.S. carriers and contributed to [publication names]. Focuses on translating complex insurance decisions into plain language for everyday American families.

This article is for informational purposes only and is not financial, legal, or insurance advice. Rates, policy features, and regulatory details vary by carrier, state, and individual profile. Always consult a licensed insurance professional before purchasing or modifying a policy.