Last Updated: April 2026

My neighbor Tony bought whole life at 29.

Paid $310 a month. Every month. For six years straight. Never missed one. His agent told him it was the smartest financial move he’d ever make — builds wealth, permanent coverage, death benefit plus a growing cash account. All of it sounded good.

Then his wife got sick. Nothing catastrophic — a surgery, some time off work — but their budget took a hit for about eight months. Tony couldn’t swing the premium anymore. He called the carrier. Cancelled. Got a check back for $4,100.

He’d paid in over $22,000.

I tell you that story not to scare you off whole life. That’s not the point. The point is Tony bought a product he didn’t fully understand, at a price that had no cushion built in, for reasons that sounded smart in a sales meeting. He didn’t ask hard enough questions. His agent didn’t volunteer the uncomfortable ones either.

That’s the whole life vs term life problem in one story. Not that one product is better. It’s that people pick without really understanding what they’re choosing or why.

Quick note before we go further: Some links here may be affiliate links. If you click through and buy, I earn a small cut — no extra charge to you. Doesn’t change what I say. Always sit with a licensed insurance professional before you actually pull the trigger on anything.

Let Me Tell You What Term Life Is, Without the Sales Pitch

It’s simple. Almost annoyingly simple.

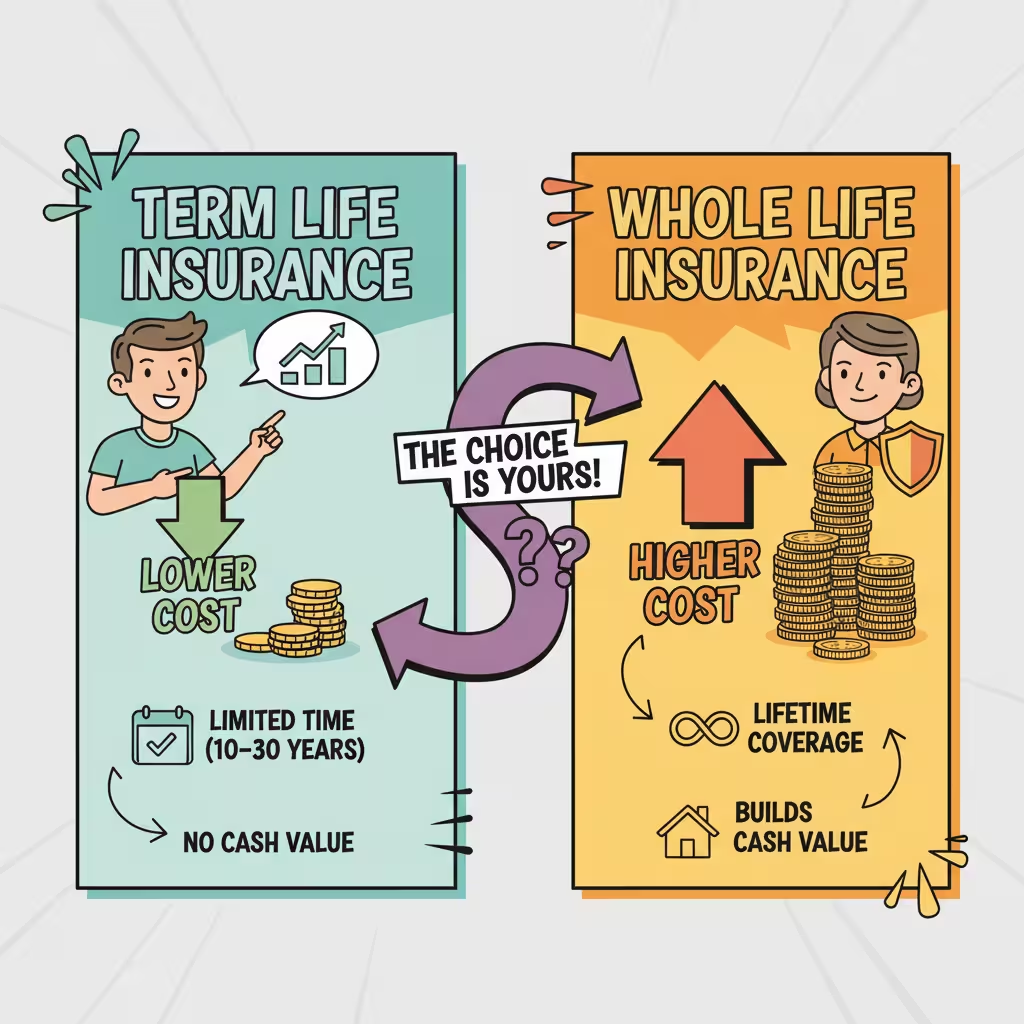

You pay a monthly premium. The company covers you for a set number of years — usually ten, twenty, or thirty. If you die in that window, your family collects the death benefit. If you’re still alive when the clock runs out? Coverage ends. No money comes back. No account. Nothing.

That’s it.

And because it’s simple — because the company’s only job is to pay out if you die during a specific stretch of time — it’s cheap. A healthy, non-smoking 35-year-old man can get $500,000 in coverage for somewhere around $25 to $35 a month on a 20-year policy. Some carriers price it even lower.

A woman the same age? A little less. Women live longer on average, which means statistically they’re a lower risk to insure. Actuarial math.

The knock on term is that “you get nothing back if you outlive it.” People hate that. I understand it. But that framing confuses insurance with investing — and those are two completely different things. Your car insurance doesn’t cut you a check because you didn’t crash this year. Your homeowner’s policy doesn’t send money back because the house is still standing. Term life works the same way. You bought protection for a risk. If the risk didn’t happen, the protection did its job.

One real weakness though: if your policy expires and your health has changed — you’re going to pay for that when you try to rebuy. Or you might not qualify at all. Some policies come with a conversion rider baked in, which lets you flip to permanent coverage before the term ends without a new medical exam. Ask about that upfront. Don’t find out it doesn’t exist when you need it.

Whole Life. The Real Version.

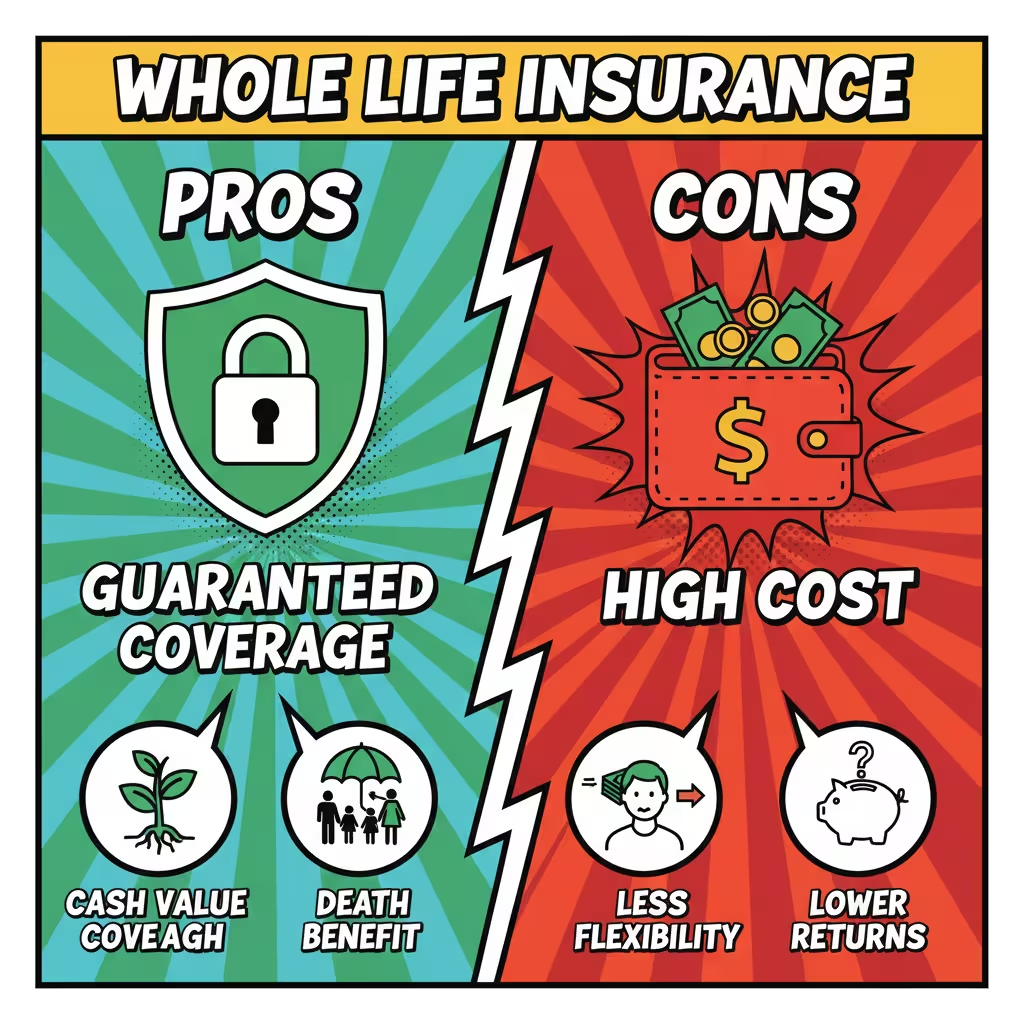

Whole life is permanent coverage. It doesn’t expire. You keep paying, you stay covered — whether you die at 61 or 97.

The premium splits two ways every month. Part covers the cost of your insurance. The rest builds up in a cash value account. That account grows at a guaranteed rate. Tax-deferred. You can borrow from it. Pull from it. Some policies throw off annual dividends on top of the growth — though those aren’t locked in like the guarantee is.

Sounds great. Now the cost.

That same 35-year-old man buying $500,000 in whole life coverage? He’s paying $400 to $600 a month. Not $30. Four hundred to six hundred dollars. Monthly.

For a woman the same age, maybe $350 to $500.

Run that out over 20 years and you’re looking at $96,000 to $144,000 in premiums paid for the woman’s version of that policy. Compare that to roughly $7,200 over 20 years on a similar term policy. That’s not a rounding error — that’s a $90,000-plus difference in what leaves your bank account.

The cash value account will have grown. No question. But the question worth asking is: grown enough to justify that gap? And grown enough to survive a rough year in your finances?

For Tony — it didn’t survive eight rough months.

Here’s the Part Where I Get a Little Annoyed

I’ve read a lot of articles about whole life vs term life. And almost all of them do this thing where they sit in the middle. “Both are good! It depends on your situation!” Very measured. Very fair. Very useless.

So I’ll say it flat: whole life is oversold to people who don’t need it. That’s not my opinion against the product. That’s my opinion about how it gets distributed. Agents make dramatically more on a whole life policy than a term policy. That financial incentive doesn’t make them dishonest — most aren’t — but it absolutely shapes what gets presented first and most enthusiastically.

The people whole life genuinely, clearly makes sense for are a specific group. And most people reading this right now aren’t in that group.

Here’s that group:

You’ve maxed your 401(k). Your Roth IRA is done for the year. You’re earning well above the Roth contribution income limits. You have a permanent financial need — a dependent who’ll require care indefinitely, an estate tax situation, a business continuity issue — and you want a tax-deferred savings vehicle that doesn’t depend on market performance. That’s a real, legitimate use case for permanent life insurance.

Or you’re a business owner who needs guaranteed, stable, permanent coverage for a buy-sell agreement. The guaranteed premium never moves. You can plan around it.

Or your child has a disability that means they’ll need financial support well past any 30-year term window.

Those are real cases. Buy for one of those reasons and whole life is a smart move.

But if you’re 34 with a new mortgage and a kid in diapers and you’re buying whole life because your neighbor said it was “the smart money move”? That’s Tony’s story. And Tony’s story ends with a $4,100 check after $22,000 in premiums.

What the Cash Value Actually Does — And Doesn’t Do

People hear “cash value growth” and think: investment account. Something working hard for them in the background.

The reality is slower and more boring.

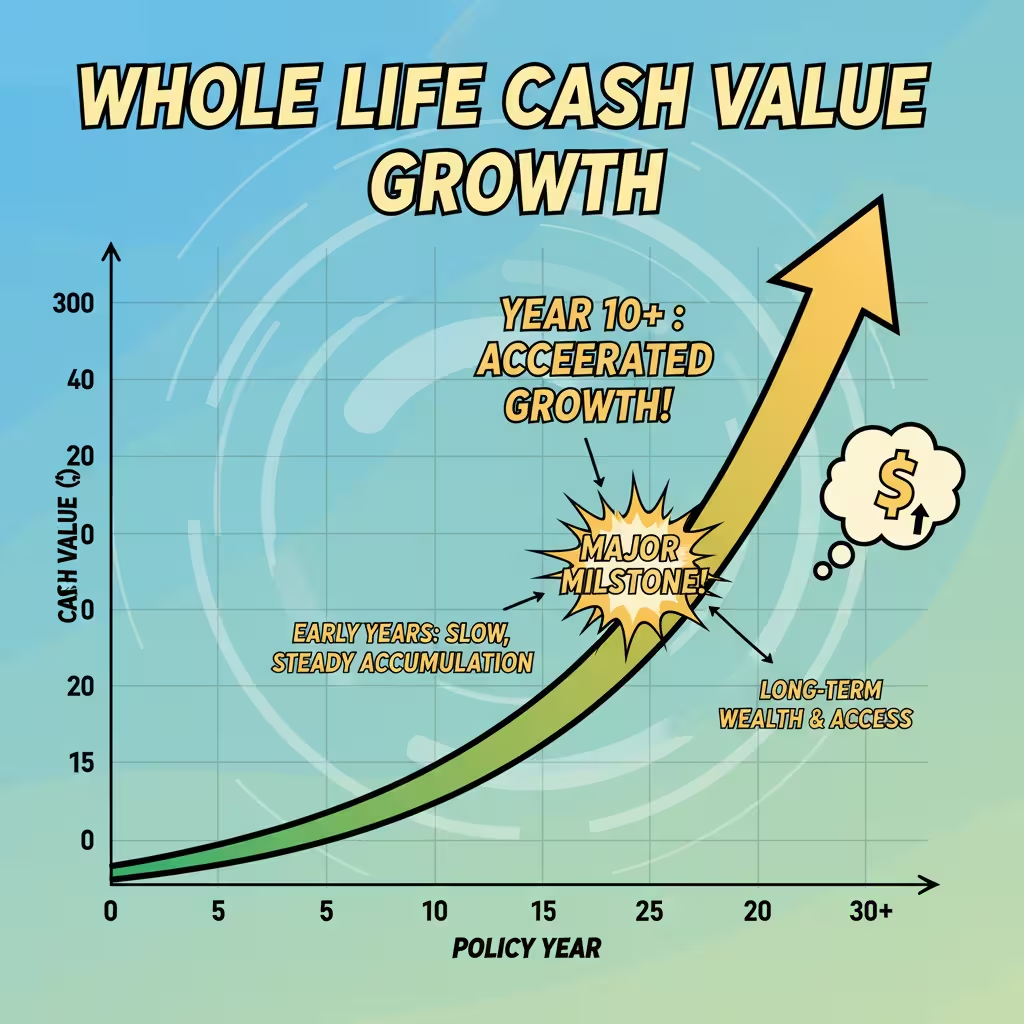

When your premium hits every month, a slice goes to insurance costs, a slice goes to carrier fees, and what’s left flows into the cash account. In year one or two, that leftover slice is small. The growth starts building traction somewhere around year five or six and improves from there. Most whole life policies don’t reach the point where total cash value equals total premiums paid until well past year ten. For some, it’s closer to year fifteen.

That matters enormously because it means you can’t treat whole life as a flexible financial tool in the near term. If you need to cancel in year four — like Tony did — you’re leaving serious money on the table.

The forced savings angle is real though. Not everyone will invest the premium difference if they go with term. I’d love to say everyone has the discipline to dump $400 a month into a Roth IRA and index funds every single month without fail. But that’s not how human beings work. For people who know they won’t actually invest the difference, the mandatory nature of a whole life premium does create a savings habit. A pool of money that grows quietly. Something they can borrow against in retirement without triggering a taxable event.

Some financial advisors have started calling whole life a “foundational liquidity asset.” I think that framing is a little generous, but the concept holds for the right person at the right income level.

One thing that changed recently: the 2021 updates to IRC Section 7702 — the tax code rule defining what qualifies as life insurance — lowered the minimum interest rate assumptions used in two qualification tests. The practical effect is that you can now pour more money into a whole life policy’s cash component without accidentally crossing into Modified Endowment Contract territory. That’s relevant if you’re funding whole life aggressively as an insurance investment tool, not just for the death benefit.

But honestly? Over 20 years, a plain index fund in a Roth IRA almost certainly outgrows the cash account. The case for whole life isn’t “better returns.” It’s “guaranteed, stable, tax-deferred growth with a death benefit attached and no market exposure.” That’s a different product with different strengths. Don’t confuse the two.

2026 Stuff That Actually Affects This Decision

A few real changes this year are worth knowing before you buy.

The “One Big Beautiful Bill” — the federal legislation that passed in 2025 — bumped the standard deduction for Americans 65 and older up to $34,700 for married couples filing jointly. Single seniors get $17,750. On top of that, there’s a new $6,000 tax break for qualifying seniors who have Social Security income. If you’re a buyer in your late 50s or early 60s looking at whole life as a retirement planning tool, those changes make the tax positioning worth modeling out properly with an advisor.

Social Security got a 2.8% cost-of-living adjustment this year. Average monthly payment climbed to about $2,071. Sounds good until you see Medicare Part B premiums jumped 9.7% — from $185 to $202.90 a month. That $17.90 increase eats most of the COLA bump for a huge chunk of retirees. The people watching that math closely are increasingly interested in having liquidity they control — separate from Social Security, separate from Medicare — which is one reason permanent life insurance with accessible cash value keeps showing up in retirement planning conversations.

SECURE 2.0 also added something worth noting: people under 59½ can now pull up to $2,500 a year out of an IRA or 401(k) without the 10% early withdrawal penalty, as long as the money goes toward a qualifying long-term care insurance premium. Not directly about life insurance — but it signals the broader direction. The government wants people thinking about these products together, not in separate boxes.

The Carriers Worth Knowing in 2026

If you’re shopping term, these names keep earning good marks.

Protective ranked Best for Cost in the 2026 Forbes/Money insurance ratings. Consistent pricing, solid policy stability. Good first stop if you’re price-sensitive.

State Farm keeps landing near the top on customer satisfaction. They’re not always the cheapest, but they’re reliable and easy to bundle if you already carry auto or home through them.

Ladder is built for people whose coverage needs change over time. You can dial your benefit down as your mortgage shrinks and your kids get older. Smart if you’re buying a big policy now and expect to need less in fifteen years.

Ethos runs a streamlined online process — no medical exam for most applicants. Fast and clean if you want to be done quickly.

For whole life, the mutual carriers have the strongest dividend track records.

Guardian Life is worth serious attention. Their 2026 dividend allocation came in at $1.7 billion — the largest in their 165-year history. Their Dividend Interest Rate for policyholders sits at 6.25% this year. That’s not guaranteed to continue, but the consistency over decades is real.

New York Life ranked Best Whole Life in the 2026 Forbes/Money ratings. Long dividend history. Strong financials. If you’re committing to a 30-year relationship with a carrier, financial stability matters more than most people realize.

National Life Group ranked second in the Wall Street Journal’s whole life rankings this year, specifically for policy fees and access to cash value. Worth comparing to Guardian and New York Life side by side.

One thing I’d push on with any whole life illustration you get: look at the guaranteed column, not the projected one. Projected assumes dividend performance that isn’t contractually locked in. The guaranteed column is what you’re actually buying. Don’t let the projected numbers close a decision that the guaranteed numbers can’t justify.

The Side-by-Side That Cuts Through Everything

Same person, same death benefit, two different products.

Healthy 35-year-old man, non-smoker, $500,000 death benefit:

Term Life (20 years): About $30/month. $7,200 over 20 years. Coverage ends at year 20. Cash value: zero. At year 21, you’re uninsured unless you rebuy.

Whole Life: About $500/month. $120,000 over 20 years. Coverage continues forever. Cash value at year 20: somewhere in the $65,000–$90,000 range depending on carrier and dividend performance.

The whole life policy builds something. The term policy covers a window and stops. Neither answer is wrong. The gap in cash value doesn’t make whole life a winner automatically — because that same $470 monthly difference, invested in a Roth IRA earning historical average market returns over 20 years, would likely build more than $90,000.

“Buy term and invest the difference” isn’t just a slogan. The math behind it is real. But it only works if you actually invest the difference — every month, without fail, for 20 years. Most people don’t. Which is where the whole life argument picks up some genuine ground.

So — Is Whole Life Worth It? Or Should You Just Buy Term?

Short version:

If you’re under 45, have kids at home, carry a mortgage, and haven’t maxed your 401(k) yet — buy a 20-year term policy. Get enough death benefit to replace your income and cover your debts. Keep the premium at a number you can hold through a tough stretch. Don’t add complexity you don’t need.

If you’re a high earner who’s done the retirement account work, has a permanent coverage need you can name specifically, and wants a conservative tax-deferred growth vehicle — whole life is worth serious consideration. Get illustrations from two or three carriers. Compare guaranteed columns. Work with a fee-only advisor who isn’t on commission.

And if you’re somewhere in between — not sure what your permanent needs look like yet — start with term. You can revisit this later. The people who regret buying term are rare. The people who regret buying whole life they couldn’t sustain? I’ve met plenty of them.

Don’t be Tony.

FAQ: Whole Life vs Term Life Insurance

Q: How much does whole life insurance cost per month for a 40-year-old?

A healthy 40-year-old man pays roughly $300–$500 a month for $250,000 in whole life coverage depending on the carrier and health rating. Women at the same age typically pay $250–$400. A 20-year term policy for the same benefit runs $25–$50 a month. That spread is real and it compounds over time.

Q: What are the honest pros and cons of whole life vs term life insurance?

Term is cheap, clean, and built for income replacement during a defined window. No cash value, no investment component, nothing left when it ends. Whole life is permanent, builds tax-deferred cash value, and can pay dividends — but costs 10 to 15 times more than similar term coverage. The cash value grows slowly early on and the policy collapses if you can’t sustain premiums through a rough stretch.

Q: Is whole life insurance worth it, or should I just buy term?

Depends on what problem you’re solving. Young family, mortgage, income replacement need? Term. Maxed retirement accounts, estate planning, permanent dependent, business continuity? Whole life has a real case. Don’t buy whole life because it “sounds smarter.” Buy it because it solves something term doesn’t.

Q: What happens if I cancel a whole life policy early?

You get back the surrender value — cash value minus surrender charges. In the early years, that’s usually well below total premiums paid. Cancelling in year four or five typically means recovering 30 to 50 cents on the dollar or less. The math improves the longer you stay in. That’s why whole life only makes sense if you can genuinely commit to it long-term.

Q: Can I convert a term policy to whole life down the road?

Many term policies include a conversion rider — lets you switch to permanent coverage before the term ends without a new medical exam. Not every carrier includes this and the terms vary. Ask about it before you buy the term policy, not after you’ve already signed.

Q: Do whole life policies actually pay dividends?

Participating policies from mutual companies like Guardian and New York Life can pay annual dividends based on company performance. They’re not guaranteed by contract. Guardian’s 2026 dividend was the largest in 165 years — $1.7 billion back to policyholders. But a strong track record doesn’t lock in future payouts. Look at the guaranteed column in any illustration, not just the dividend-inclusive projection.

One Last Thing

The whole life vs term life decision feels complicated because the internet makes it complicated. Half the content is written by people selling whole life. The other half is written by people who hate whole life. Neither side is great at nuance.

Here’s the version I’ve landed on after looking at this for a long time.

Most people need term. They need it this week, not after six months of research. They need enough death benefit to cover what they’d leave behind — income, mortgage, debts — and they need a premium they can hold through whatever life throws at them.

A smaller group of people, usually older and higher-income, have specific permanent needs. Those people should absolutely look at whole life. Carefully. With a fee-only advisor. And full eyes on the guaranteed numbers.

Everyone else is probably overthinking it.

Buy the coverage that fits. Keep it. That’s the move.

About the Author

This post was built using the 2026 Insurance and Retirement Financial Study Guide and the 2026 Insurance Industry Briefing — drawing on NAIC regulatory data, Forbes/Money and Wall Street Journal 2026 carrier rankings, and legislative analysis of the SECURE 2.0 Act and the One Big Beautiful Bill. Premium estimates reflect 2026 published market ranges. Actual rates vary by state, carrier, health class, and coverage amount. Verify current quotes with a licensed agent.

This is educational content only. Nothing here is financial, insurance, or tax advice. Coverage costs and features differ by state and individual underwriting. Work with a licensed professional before making any policy or coverage decision.