Last Updated: April 2026

Nobody reads their disability policy. Not the whole thing.

They sign up at open enrollment, check the box, and move on. Which is completely understandable — nobody has time to read 40 pages of insurance contract language when they’re also trying to do their actual job. I get it.

But here’s where that becomes a problem.

Kevin was a dentist in Columbus. Fourteen years into a good private practice, earning around $310,000 a year. He had disability coverage through his state dental association. Enrolled at orientation. Filed it away. Thought nothing of it.

At 43, he developed essential tremor. His hands shook badly enough that fine restorative work became impossible — crown prep, implants, anything requiring precision motor control. He filed a claim. The insurer paid.

For 24 months.

Then month 25 hit, and his policy did something Kevin had never read about. The definition of “disabled” quietly changed. Under the original language, he was disabled because he couldn’t perform the duties of his specific profession. Under the new language — the any-occupation standard that kicked in automatically — he could still consult, still lecture, still supervise. So the insurer said he wasn’t disabled anymore.

$310,000 a year. Gone. Replaced by a $1,630-a-month Social Security check.

That’s what this disability insurance guide is actually about. Not the stuff you’d find on a carrier’s FAQ page. The real part — the switch, the clause, the policy language nobody reads until they desperately need to.

Disclosure: Some links in this post connect to independent insurance brokers. We may receive a referral fee if you connect through our links. This doesn’t affect our recommendations or editorial positions.

Here’s Something Most People Never Do the Math On

You’ve insured your car. Your house. Probably your life.

Now think about what actually pays for all of that.

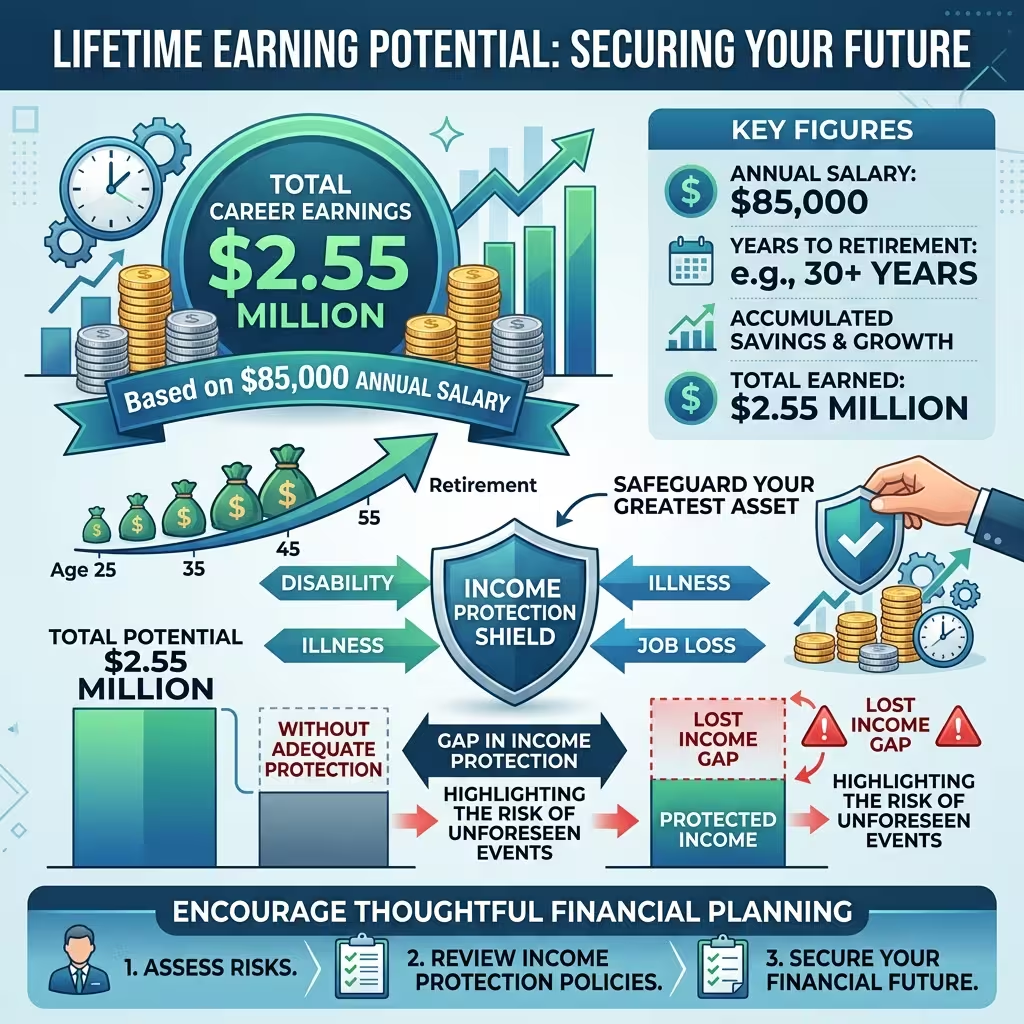

If you’re 35 and earning $85,000 a year, your future income — just at flat salary to retirement at 65 — is $2.55 million. With raises? More. Probably a lot more. Your car isn’t worth that. Your house might be, someday. Your 401(k) isn’t there yet.

Knowing how much of that income your policy should actually replace — and how to calculate the right benefit amount — is where most people get stuck. Our disability insurance coverage calculator guide walks through it in four steps.

And yet the paycheck itself? Totally unprotected for most people.

Income protection insurance — which is what the industry calls disability products — pays you a monthly benefit when a sickness or injury stops you from working. That’s it at the core. But the gap between “sounds simple” and “actually works when you need it” is where Kevin’s story lives, and it’s where most of the real risk hides.

The U.S. disability insurance market is projected to hit $5.08 billion in 2026, up from $4.56 billion last year. More products, more carriers, more noise. And underneath all of it — tens of millions of American workers still without real coverage. The market is growing fast. The coverage gap isn’t shrinking nearly as fast.

The Numbers Most People Get Wrong

Ask someone to picture a disability. What do they see?

Usually something dramatic. A car crash. A fall. A sudden, obvious event. That mental picture is why most people underestimate this risk — they’re imagining the wrong thing entirely.

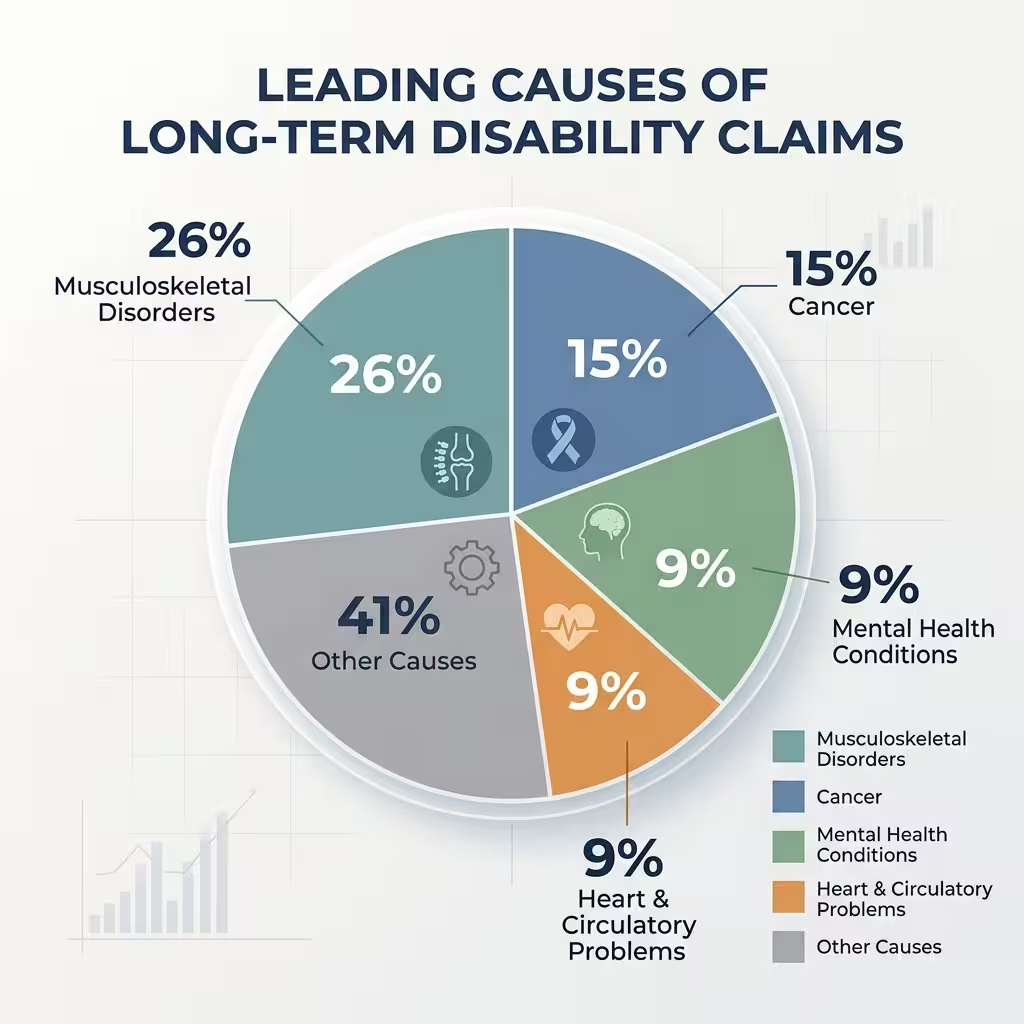

Here’s what the Council for Disability Awareness actually found. Musculoskeletal disorders — back problems, joint deterioration, repetitive stress injuries — cause 26% of long-term disability claims. Cancer accounts for 15%. Mental health conditions, 9%. Heart and circulatory problems, another 9%.

If you want to understand exactly what conditions drive the most claims — and what that means for your own coverage decisions — see our breakdown of the top causes of disability claims.

Mental health conditions alone account for nearly 1 in 10 long-term claims — and navigating those claims requires a different strategy. Our mental health disability insurance guide covers what to document, how insurers evaluate these claims, and how to avoid denial.

Accidents don’t even crack the top two causes.

Illness does. The slow kind. The kind that builds over years and then one day becomes impossible to work through. Kevin’s tremor didn’t appear overnight. These things rarely do.

Now the probability. Nearly one in four 20-year-olds will miss at least a full year of work due to disability before reaching retirement. That’s not a fringe statistic buried in actuarial tables. That’s a roughly 25% chance. If you’re reading this with a few colleagues, one of you statistically fits that profile.

Sound dramatic? It isn’t. It’s just what the numbers show.

Here’s the one that lands hardest: 51 million working Americans have no disability coverage beyond Social Security. Not inadequate coverage. None. And the average SSDI benefit in early 2026 — after the 2.8% cost-of-living adjustment that took effect in January — runs about $1,630 a month.

And that $1,630 SSDI check? It may be taxable depending on your other income. The same is true for private disability benefits — whether they’re taxable depends entirely on who paid the premiums. Get the full picture in are disability insurance benefits taxable.

For someone earning $80,000 or $200,000 or $400,000 a year, $1,630 a month isn’t income replacement. It doesn’t cover the mortgage. Doesn’t cover the car payment. Doesn’t come close to maintaining a household built on a professional salary.

Nearly 40% of American adults can’t cover a $400 emergency without going into debt. A multi-year disability funded only by SSDI doesn’t just create hardship — medically related work loss contributes to over 44% of consumer bankruptcies in the U.S. These aren’t worst-case projections. They’re documented outcomes.

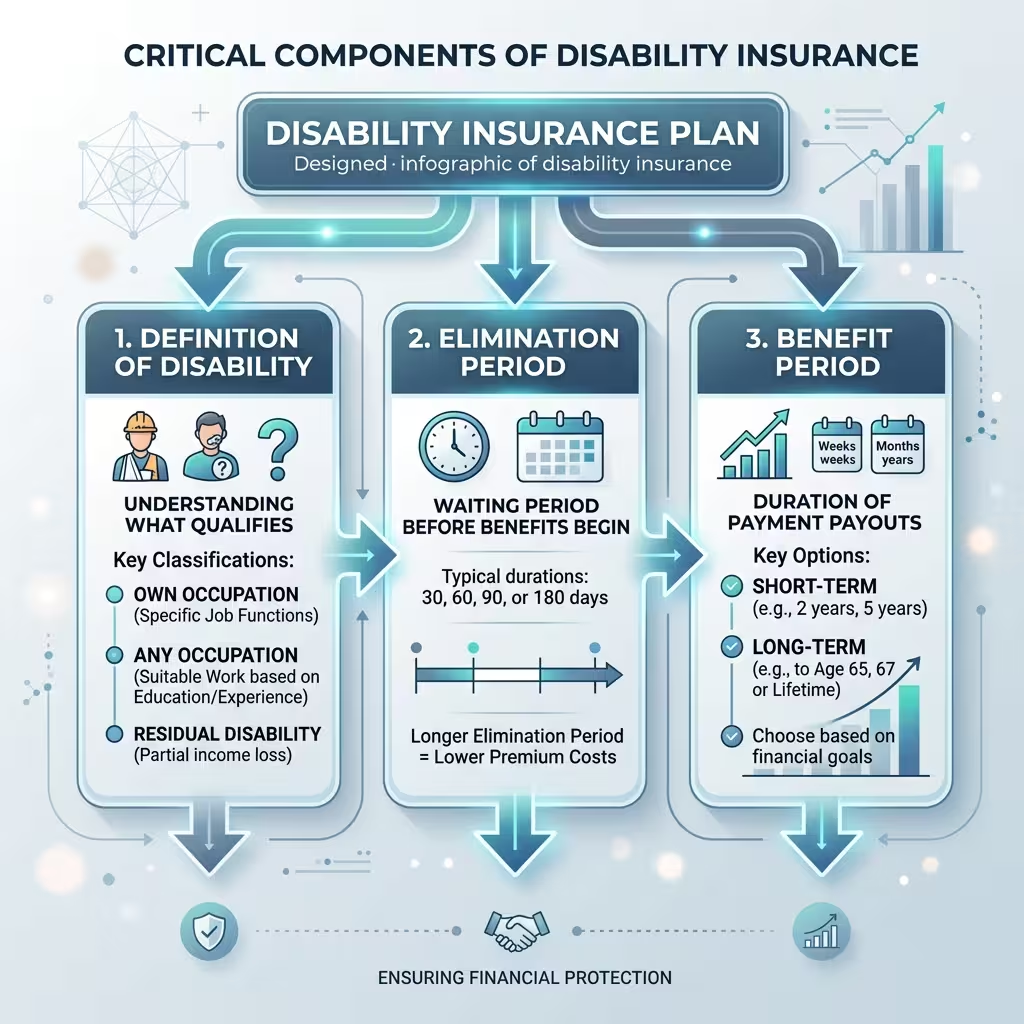

How Disability Insurance Actually Works — The Parts That Matter

Three things determine whether a disability policy is worth what you pay. The definition of disability. The elimination period. The benefit period.

Not sure whether you need short-term coverage, long-term coverage, or both? We break down exactly how each works — including elimination periods and benefit windows — in our short-term vs long-term disability insurance guide.

Get one wrong and the rest doesn’t matter.

The Definition — This Is Where Everything Lives or Dies

If you only read one part of any disability policy, make it the definition of disability. This is the clause that determines whether a claim gets paid. Two policies with nearly identical premiums can produce completely different outcomes at the moment of a claim based solely on this language.

There are a few main versions.

True Own-Occupation is what every dentist, physician, surgeon, attorney, and high-skill professional should hold out for. Under this definition, you collect full benefits if you can no longer perform the material duties of your specific occupation — even if you’re capable of working in a completely different field. A surgeon who can no longer operate gets paid. Even if she teaches. Even if she consults. Even if she runs a medical practice administratively. The policy triggers on what she can’t do, not on whether income is coming in from somewhere else.

Any-Occupation flips the whole thing. Benefits only pay if you can’t work in any occupation you’re reasonably suited for by education, training, or experience. A dentist who can consult and lecture? Technically employed in medicine. Claim denied. This is the definition Kevin’s plan used after month 25.

Modified Own-Occupation lands in between. It pays if you can’t do your own job and you’re not currently working somewhere else. Better than any-occupation. Not as protective as true own-occ, especially for specialists.

Physicians face the highest stakes here — a surgeon or specialist who loses the ability to practice their specific discipline needs coverage that reflects that reality. See our full guide to disability insurance for physicians for specialty-specific recommendations.

For a side-by-side breakdown of how these definitions play out in real claims — and which one you actually need based on your profession — see our full comparison: own-occupation vs any-occupation disability insurance.

Let me be direct: if you’re a specialist of any kind and your policy uses any-occupation language, you don’t have the protection you think you have. You have income protection for non-specialists living inside a specialist’s premium.

The 24-Month Switch — The Thing Nobody Warns You About

This is the specific mechanism that ended Kevin’s benefit.

A large number of group disability plans — the ones you get through an employer, a professional association, or a union — use own-occupation language for the first 24 months of a claim. At month 25, the definition automatically switches to any-occupation.

This is one of several critical gaps hidden inside employer-sponsored coverage. If you’re relying solely on a workplace plan, read our deep dive on individual vs group disability insurance before your next open enrollment.

Insurers aren’t doing this arbitrarily. Month 25 is statistically when partial recoveries cluster. The claimant is better, but not completely better. Under own-occupation, that doesn’t end the benefit. Under any-occupation, it frequently does.

Pull your group plan document today — not when you need to file. Find the definition section. Find what happens at month 25. Know what you have before you ever need it.

The Elimination Period

Think of this as a time-based deductible. The elimination period is the gap between when a disability starts and when the first benefit check arrives. Typical options are 60, 90, or 180 days.

Longer waiting period, lower premium. The tradeoff: you have to fund that gap with savings. A 180-day elimination period means six months of mortgage, utilities, groceries, and everything else coming out of pocket while you wait.

Choose based on how many months of liquid savings you actually have — not based on what looks cheapest on a quote comparison.

The Benefit Period

How long the policy pays once benefits start. Options run two years, five years, to age 65, or to age 67.

Two-year coverage handles a broken ankle that keeps you out of work for a few months. It doesn’t handle essential tremor, early-onset Parkinson’s, or a cancer diagnosis at 44. For most professionals — doctors, dentists, attorneys, CPAs — a benefit period to age 65 is the minimum worth buying. Anything shorter is short-term coverage wearing a long-term label.

The Tax Rule That Changes Your Real Numbers

Here’s the one that genuinely surprises people.

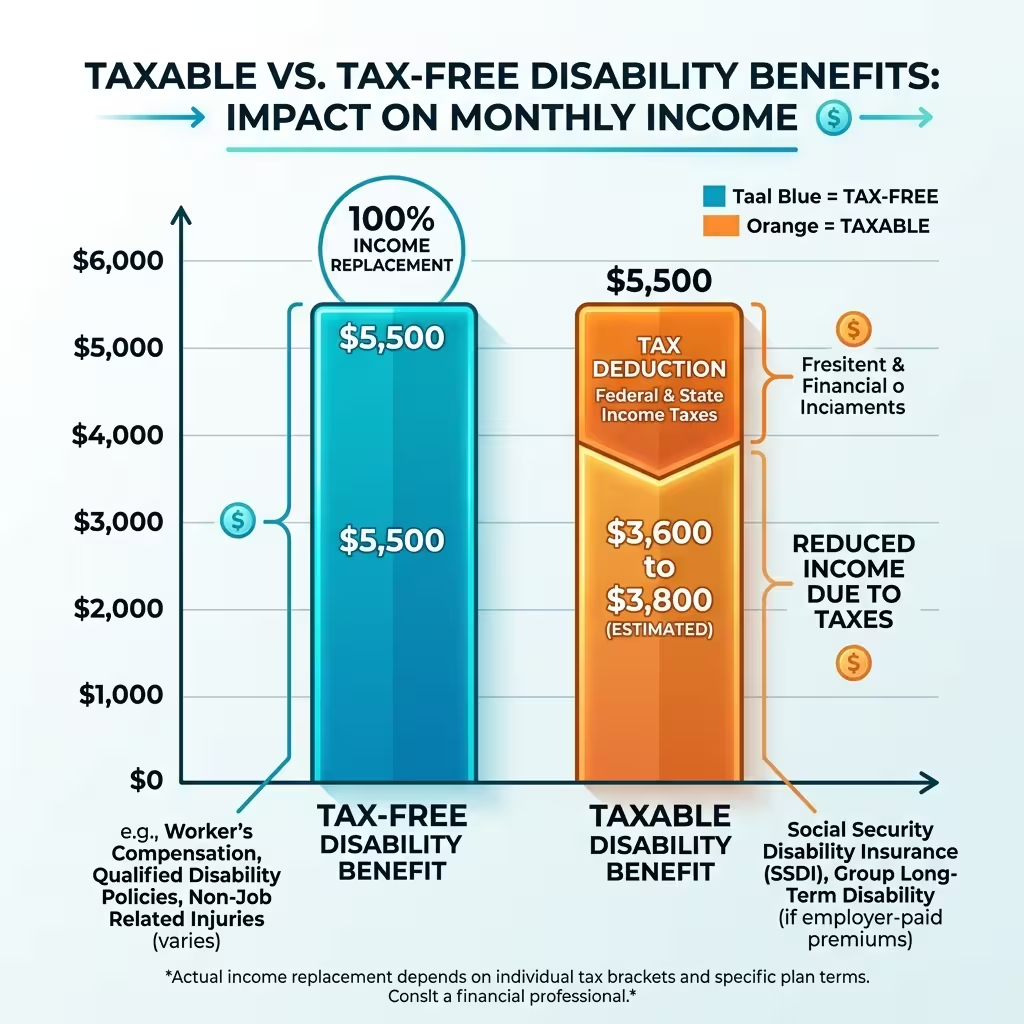

Whether disability benefits are taxed depends entirely on how you paid the premium. One factor. That’s it.

Pay premiums with after-tax dollars — which is how most individual policies work — and the monthly benefit arrives 100% tax-free. A $5,500/month benefit is $5,500 you actually receive.

Pay premiums with pre-tax dollars — which is what happens when an employer pays your premium or uses a salary-reduction plan — and every benefit dollar is taxable as ordinary income. That $5,500/month drops to somewhere around $3,600–$3,800 after federal and state taxes for a mid-to-high earner.

Run that through on a $200,000 salary where the group plan promises 60% income replacement. On paper that’s $120,000 a year. On a taxable benefit at a 35% effective rate, you’re looking at roughly $78,000. That’s a $42,000 annual gap against a mortgage, school tuition, and a lifestyle built on the original number.

This is why high earners often carry supplemental individual policies on top of group coverage. Not for redundancy. For arithmetic. The group plan’s taxable benefit plus the individual policy’s tax-free benefit can produce a combined replacement close to what you actually need.

What It Costs

Individual long-term disability insurance runs 1% to 3% of annual salary in premiums for most applicants. On a $100,000 income, that’s $1,000–$3,000 per year — about $83 to $250 a month.

A few things move that number up or down.

Age is the biggest one. Buying at 28 locks in permanently lower rates. Waiting until 46 doesn’t just cost more — at some ages and health profiles, certain carriers start adding exclusions or declining the application entirely. The window for clean underwriting closes faster than most people expect.

Occupation class matters. Carriers assign risk ratings by job type. A financial analyst pays less than an oral surgeon. The surgeon’s hands are how she earns — the premium reflects that. High manual dexterity professions pay more because the risk of a dexterity-related disability is actuarially real, not hypothetical.

Benefit amount. Most policies cap at 60%–70% of pre-disability income. Combined with the tax treatment above, this is why calculating the net benefit — after any applicable taxes — matters more than the headline replacement percentage.

What’s Different in 2026

The Social Security COLA that kicked in January 2026 brought the average SSDI benefit to approximately $1,630 a month. The taxable wage base for Social Security contributions rose to $184,500, meaning higher earners pay more into the system. The Substantial Gainful Activity threshold — the monthly earnings limit used to determine whether SSDI recipients can still qualify as “disabled” — increased to $1,690 for non-blind recipients.

On the private market side, AI-driven underwriting is making applications faster but more thorough. Medical records get reviewed more carefully now, not less. This isn’t a reason to panic — it’s a reason to apply while healthy, before health history has accumulated enough to complicate underwriting.

One 2026-specific issue for physicians: if you prescribe GLP-1 medications or perform med-spa procedures, verify explicitly that your disability policy covers those treatment categories. Some group plans exclude newer procedure types. Bring this up as a direct question with your broker — not an afterthought at the end of a conversation.

Finding Coverage That Actually Holds Up

Note: Some broker links in this section are affiliate referrals at no cost to you.

Work with an independent broker — not a captive agent tied to a single carrier. A captive agent sells what their company offers. An independent broker can lay three or four contracts side by side and walk through the definition sections with you. That contract-to-contract comparison matters far more than a premium comparison.

Carriers consistently recommended by independent brokers for strong true own-occupation language include Guardian, Principal, and Ameritas. Not because they’re cheapest. Because their policy definitions tend to hold up when claims get tested.

Ask specifically about residual disability riders. These pay a proportional benefit when you’re working at reduced capacity — not fully disabled, just earning less. Most trigger at a 15%–20% income loss. For fee-for-service professionals — dentists, physicians, therapists, CPAs — partial disability is often more likely than total disability. The residual rider covers what the base policy misses.

The proportional math is simple: lose 40% of your income due to a qualifying disability, the policy pays 40% of the monthly benefit. Lose more than 75%–80%, most policies pay the full benefit. Lose 15%? Nothing without the rider.

Future Increase Option riders are worth adding early in a career. They let you buy more coverage as your income grows — without new medical underwriting. Lock it in at 29 when you’re healthy, and you can expand coverage at 38 or 42 without a new physical, even if your health has changed by then. That optionality gets more valuable over time, not less.

Physicians face the highest stakes here — a surgeon or specialist who loses the ability to practice their specific discipline needs coverage that reflects that reality. See our full guide to disability insurance for physicians for specialty-specific recommendations.

Is Disability Insurance Worth It for High Earners?

Yes. With no real debate.

High earners have more to lose and more fixed costs that don’t pause. The mortgage is larger. The practice overhead doesn’t stop. School tuition, partnership obligations, loan payments — none of it cares that income stopped.

SSDI pays $19,560 a year. A professional earning $350,000 annually can’t bridge that gap with a government benefit. Financial planning that doesn’t include own-occupation disability coverage isn’t complete — it’s built on a foundation with a visible crack in it. Life insurance covers death. Disability insurance covers the longer, slower financial emergency where the bills keep arriving and the income has already stopped.

The professionals who skip this coverage are often the ones with the most to lose. That’s not an exaggeration. It’s just math meeting high fixed costs.

If you’re self-employed or freelance, the calculus is different — you have no employer plan to fall back on and no payroll-based premium arrangement. Our guide to disability insurance for freelancers covers the options available without an employer and how to structure coverage on your own.

People Also Ask – PAA’s

What is a disability insurance guide really trying to help me understand?

What you actually own before you ever need to use it. Most people have “some coverage” through work but haven’t read the definition section. A real guide explains what the definitions mean in plain language, where the gaps appear, and what filling those gaps looks like.

How does income protection insurance work in practice?

You pay a monthly premium. A qualifying illness or injury prevents you from working. After your elimination period ends, the policy pays a monthly benefit — typically 60%–70% of pre-disability income — for the length of your benefit period. The key word is “qualifying.” The definition section determines what that means.

What is the US disability insurance market doing in 2026?

Projected to hit $5.08 billion this year, up from $4.56 billion in 2025. Growth is being driven by gig workers needing portable coverage, professionals learning from claim disputes they’ve watched others navigate, and AI underwriting making the application process faster. The market is expanding. Whether individual coverage is expanding at the same pace is a different question.

How long should my elimination period be?

Match it to your liquid savings. If you have 90 days of expenses comfortably accessible, a 90-day elimination period makes sense. If you have 6 months in cash, 180 days will lower your premium. Don’t stretch the elimination period beyond what your savings can actually bridge — the premium savings disappear fast if you have to carry credit card debt to cover the gap.

Can I just rely on SSDI?

SSDI averaged $1,630 a month in early 2026. Initial applications are frequently denied, and the process from application to first payment can take a year or more. For anyone earning above $35,000 a year, SSDI alone doesn’t replace income at any level that maintains a normal household. It’s a floor. It’s not a plan.

What’s the best long-term disability insurance for professionals in 2026?

For specialists, true own-occupation policies from carriers like Guardian, Principal, and Ameritas are consistently recommended by independent brokers for the strength of their contractual language — not just competitive pricing. Two policies at similar premiums can differ dramatically on what actually triggers a benefit. Contract language beats premium shopping every time.

Is disability insurance worth buying young if you’re healthy?

Young and healthy is exactly when to buy. Rates are lower, underwriting is cleaner, and the Future Increase Option rider is most valuable when income is still growing. Every year you wait, the rate goes up and the health history gets longer.

How Kevin’s Story Ended

He fought the insurer. Eighteen months of legal back-and-forth. Eventually settled for less than what his original benefit would have totaled — but enough to keep the practice from folding.

His tremor improved somewhat on medication. He returned to limited clinical work about two years later.

The financial damage from those two years — depleted savings, kids’ college funds touched, staff turnover he couldn’t prevent — doesn’t erase because the legal dispute eventually resolved. That part stays.

He now carries an individual true own-occupation policy with a residual rider and a benefit period to 65, purchased through an independent broker who compared four carrier contracts side by side. Kevin read the definition section before he signed. He knows what happens at month 25 because he lived through month 25 without knowing.

Your income built everything. In 2026, with policy language that can quietly flip after two years and a private disability insurance market growing fast enough that the differences between products are harder to spot, understanding what you actually own before you need it is the only responsible position.

That’s what a real disability insurance guide does. Not sells you fear. Makes sure you’ve read page 11.

About the Author

Selene Voss has covered personal finance, risk management, and U.S. insurance markets for eight years. He has analyzed disability contracts across more than a dozen carriers and written for financial literacy publications focused on professional income protection. He holds no insurance licenses and does not sell insurance products.

This article is for informational purposes only. It does not constitute financial, legal, or insurance advice. Policy terms, premiums, and benefit structures vary significantly by carrier, state, and individual underwriting profile. Consult a licensed independent insurance broker before making any coverage decisions. Figures reflect 2026 publicly available market and government data.