Last Updated: April 2026

Rachel thought she had it handled.

She’d bought a $500,000 life insurance policy three years ago. Paid every month without complaint. Told herself her family was covered. Slept fine.

Then her financial advisor asked one question: “Have you actually run the numbers?”

She hadn’t. So they did it together, right there at the table. Mortgage balance. Both kids’ projected college costs. Her income, multiplied out over the years until her youngest turns 18. Outstanding car loan. Her husband’s reduced earning capacity if he had to become the sole caregiver.

Total gap: $400,000. Her $500,000 policy would have left her family short — significantly short — inside of five years.

Here’s the thing. Rachel isn’t careless. She’s a nurse. She’s smart. She just did what most people do: picked a round number that felt big enough and moved on without contemplating how much life insurance do I need?

That round number could have cost her family everything.

This guide is about finding your actual number. Not a guess. Not a rule of thumb. A real figure based on your real life.

Disclosure: Some links in this article may be affiliate partnerships. We may earn a small commission if you purchase through them — at no extra cost to you. Our recommendations don’t change based on that.

If you’re still deciding which type of policy to buy, start with our complete life insurance guide — it covers term vs. whole, costs, and top-rated carriers.

Why “10x Your Salary” Is the Wrong Starting Point

Ask most people how much life insurance they need and they’ll say something like, “I’ve heard 10 times your income.” They’re not wrong that they’ve heard it. But that rule is a shortcut — and shortcuts in life insurance can leave real gaps.

Here’s why it falls apart. The 10x rule doesn’t account for your mortgage balance. It doesn’t ask how many kids you have or how old they are. It doesn’t factor in existing debt, your spouse’s income, or whether you’re paying for elderly parents. It’s a blunt instrument dressed up as wisdom.

A 40-year-old with a $400,000 mortgage, two kids under 10, and $80,000 in income needs a wildly different number than a 40-year-old who rents, has no kids, and earns the same salary.

Same formula. Completely different situations. Only one of them gets the right answer.

The financial industry has known this for years. That’s why better tools exist. Let’s go through them.

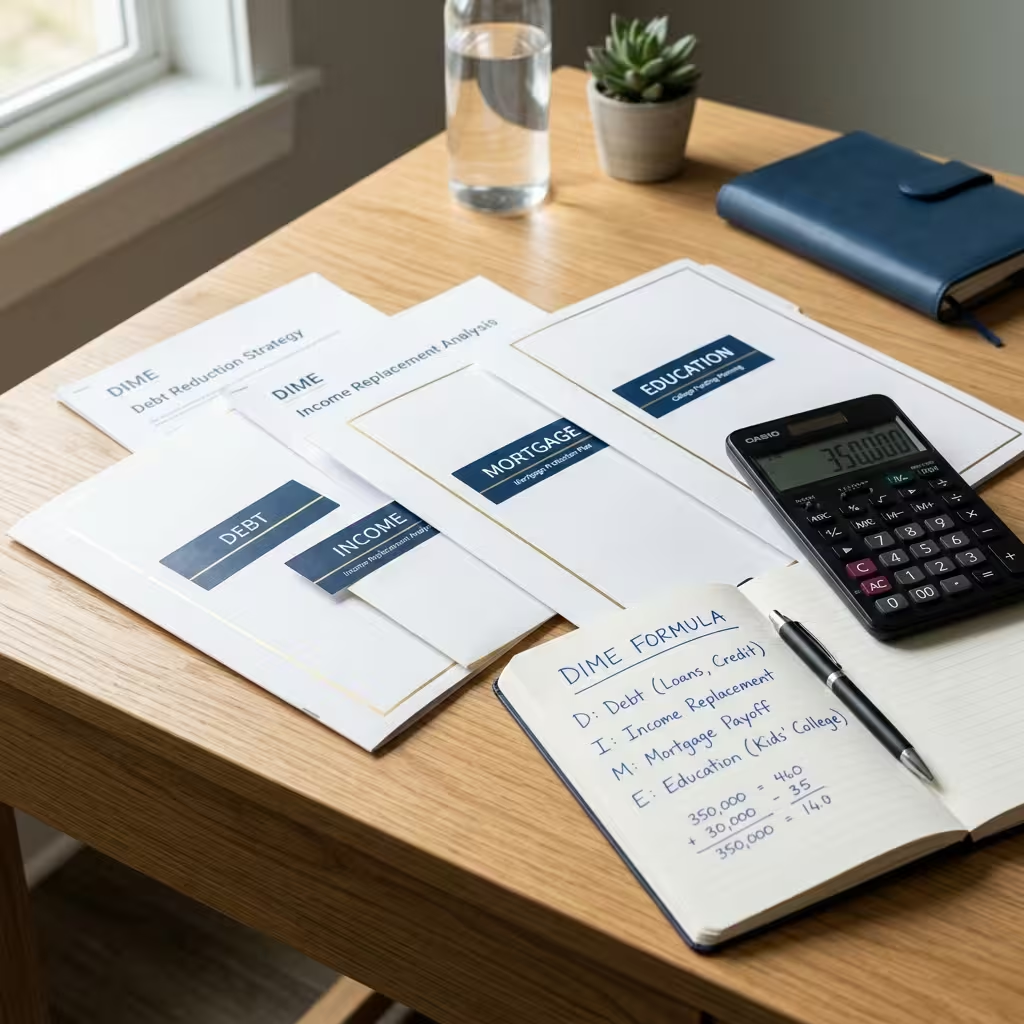

Method 1: The DIME Formula — The Most Accurate Starting Point

DIME stands for Debt, Income, Mortgage, Education. It’s the calculation financial professionals actually use — and it’s what your family actually needs.

Here’s how it works.

D — Debt Add up every debt you carry outside of your mortgage. Car loans. Credit cards. Student loans. Medical bills. Personal loans. Everything. Write down the total.

I — Income Take your annual income and multiply it by the number of years until your youngest child is financially independent — typically 18, sometimes longer. If you earn $75,000 a year and your youngest is 8, that’s 10 years. $75,000 × 10 = $750,000.

M — Mortgage Whatever you still owe on your home. Not the original loan amount. The current payoff balance.

E — Education College costs in 2026 run over $30,000 a year at public in-state schools, over $50,000 out-of-state, and above $65,470 at private universities. For each child, estimate four years of costs at whatever school type is realistic. Two kids at a public university? That’s roughly $240,000 to $260,000 in today’s dollars — and that number keeps climbing.

Add D + I + M + E. Subtract any existing savings, investments, or coverage your spouse already carries. What’s left is your number.

DIME Life Insurance Calculator

Calculate your precise coverage needs based on the DIME framework.

Your Coverage Breakdown

This calculation is based on the DIME method illustrative metrics for 2026 financial planning.

A Real Family Example

Let’s make it concrete.

Meet a typical family of four. Two parents, ages 38 and 36. Two kids, ages 9 and 6. Primary earner makes $85,000 a year. They own a home with $320,000 left on the mortgage. They have $35,000 in combined debt outside the mortgage. They want both kids to attend public universities.

Here’s the DIME breakdown:

| Category | Amount |

| Debt (non-mortgage) | $35,000 |

| Income (× 12 years until youngest is 18) | $1,020,000 |

| Mortgage balance | $320,000 |

| Education (2 kids × $120,000) | $240,000 |

| DIME Total | $1,615,000 |

| Minus existing savings/assets | − $150,000 |

| Coverage Needed | $1,465,000 |

Nearly $1.5 million.

If that family bought a $500,000 policy because it “seemed like a lot,” they’d be about $965,000 short. Their kids’ college plans would collapse. The mortgage would be in jeopardy within a few years. The surviving spouse would face an impossible financial rebuild — while grieving and raising two children alone.

This is why the math matters.

Is $500,000 Life Insurance Enough for a Family?

Short answer: it depends on your debt, income, and family size. But for most families with a mortgage and children under 18, $500,000 is not enough.

The example above shows a family needing over $1.4 million. For a family of four with modest debt and a mid-range income, $500,000 covers roughly two to three years of total expenses. That’s not a safety net. That’s a bridge to crisis.

Here’s when $500,000 is enough:

- You’re single with no dependents and minimal debt

- Your kids are grown and financially independent

- You’re close to retirement and your spouse has substantial retirement income of their own

- You’ve already paid off your mortgage

Here’s when it’s not enough:

- You have a mortgage balance above $200,000

- You have children under 15

- You’re a primary earner and your spouse earns significantly less

- You have outstanding debt above $50,000

If you’re in the second group — and most working parents are — $500,000 is a starting point, not a finish line.

How Much Life Insurance Does a Family of 4 Need?

This is one of the most Googled questions in insurance, and the honest answer is: more than most people carry.

Using DIME, a family of four with two young children, a mortgage, and a primary earner in the $70,000–$100,000 range typically needs between $1 million and $1.8 million in total coverage.

That sounds like a large number. And it is. But here’s something most people don’t know: according to LIMRA research, 42% of Americans overestimate the cost of life insurance by three to six times. A healthy 35-year-old can get $1 million in 20-year term coverage for around $50–$60 a month. That’s less than a streaming service bundle.

The coverage gap in this country isn’t a money problem for most families. It’s a math problem. People assume they can’t afford the right amount — before they’ve ever looked at the actual price.

Method 2: The Human Life Value Approach

DIME focuses on obligations. This method focuses on you.

Human Life Value (HLV) calculates the total economic contribution you’d make to your family over your remaining working years — including income, benefits, services, and the unpaid work you do every day.

Here’s something that makes this real. The 2026 Cost of Care Report found that 59 million family caregivers in the U.S. provide 49.5 billion hours of unpaid care per year, valued at over $1 trillion. That’s not a rhetorical number. It’s what economists calculate unpaid family labor — childcare, household management, elder care — is worth at market rates.

When a primary caregiver dies, their family doesn’t just lose their income. They lose all of that. Childcare costs alone average $17,264 per year for infants. Replacing even a portion of what a stay-at-home parent provides would cost a surviving spouse tens of thousands annually.

HLV adds this up. It asks: what would it cost to replace everything this person does — financially and practically — for the next 20 years?

The number is almost always larger than a simple salary multiplication. And it’s almost always closer to the truth.

The Stay-at-Home Parent Problem

Here’s one that catches a lot of families off guard.

Many couples insure the working parent heavily and carry little or no insurance on the stay-at-home parent. The logic seems to make sense — the working parent earns the income, so they’re the financial risk, right?

Wrong.

If the stay-at-home parent dies, the surviving working parent suddenly needs full-time childcare, after-school care, household management, and potentially elder care help — all at once, while continuing to work full-time. That’s not a theoretical cost. It’s a real, immediate expense that can easily run $30,000 to $50,000 per year.

Stay-at-home parents need life insurance too. Typically $400,000 to $600,000 is a reasonable starting range, adjusted for number of children and local care costs.

This is an area where the “income replacement only” thinking breaks down badly. We cover this in full in our guide to life insurance for stay-at-home parents and spouses

Using a Life Insurance Calculator — What to Put In

If you want to run your own numbers, a life insurance calculator by income and debt will ask for most of the same DIME inputs. Here’s what to have ready before you start:

- Your current annual income (and your spouse’s, if applicable)

- Your mortgage payoff balance — not the original loan

- All non-mortgage debt totals

- Number of children and their current ages

- Estimated college costs per child

- Any existing life insurance or savings

- Your spouse’s annual income

Put in real numbers. Not rounded estimates. Not what you wish the balances were.

The calculator will spit out a number. That number is your target.

What the 10x Rule Gets Right (And Where to Use It)

Okay — to be fair — the 10x salary rule isn’t useless. It’s a quick sanity check.

If someone tells you they have $50,000 in life insurance on an $80,000 salary with three kids, you don’t need DIME to know that’s dangerously low. The 10x rule catches the obvious problems fast.

Where it falls apart is for anyone with unusual circumstances. High debt. Young children. A non-working spouse. A high-cost state. An aggressive mortgage. Any of these push your real number well above what 10x gives you.

Use 10x to spot obvious gaps. Use DIME to find the right number.

2026 Costs Put This in Perspective

One more reason to take your coverage seriously: the numbers families are navigating right now are historically high.

Raising a child to age 18 now costs an average of $303,418 — roughly $16,857 per year, according to 2026 data. In Hawaii, that figure climbs to $412,661. The total cost of raising a child today mirrors the median U.S. home sale price of $356,000.

College runs over $30,000 per year at public in-state schools. Over $65,000 at private universities.

And 30% of Americans would suffer financial hardship within one month of a primary wage earner’s death. One month.

These aren’t abstract numbers. They’re the environment your family lives in. Your coverage amount needs to reflect that environment — not a rule of thumb written before tuition tripled.

People Also Ask – PAA’s

How much life insurance does a family of 4 need?

For most families with two young children, a mortgage, and a primary earner between $70,000–$100,000, the DIME method typically points to $1 million to $1.8 million in total coverage. The exact number depends on your mortgage balance, debt, income years remaining, and college cost estimates for each child. A 20-year term life insurance policy is the most cost-effective way to reach that number for most families.

How do I use a life insurance calculator by income and debt?

Gather your annual income, mortgage payoff balance, all non-mortgage debts, number and ages of children, and estimated college costs. Enter these into a DIME-based calculator. Subtract existing savings and any current coverage to get your net coverage gap. Life Happens and many major carriers offer free calculators online.

Is $500,000 life insurance enough for a family?

For most families with young children and a mortgage, no — $500,000 covers two to three years of total family expenses. Using the DIME method, most families of four need $1 million or more. $500,000 may be sufficient for single adults, couples without dependents, or families near retirement with low debt.

What is the DIME method for life insurance?

DIME stands for Debt, Income, Mortgage, and Education. Add your non-mortgage debts, multiply your income by years until your youngest child is independent, add your current mortgage balance, and add projected college costs for each child. The total, minus current savings and coverage, is your target coverage amount.

Does a stay-at-home parent need life insurance?

Yes. Replacing the childcare, household management, and caregiving a stay-at-home parent provides can cost $30,000–$50,000 per year. Most financial planners recommend $400,000–$600,000 in coverage for stay-at-home parents, adjusted for the number of children and local care costs.

What’s wrong with the 10x salary rule?

It ignores your mortgage balance, debt, number of dependents, and the age of your children. Two people with the same salary can need vastly different coverage amounts. Use the 10x rule as a rough check for obvious gaps — but rely on the DIME method for your actual coverage target.

Rachel ran the full DIME calculation two months after that conversation with her advisor. She increased her coverage to $1.2 million. Her monthly premium went up $34.

Thirty-four dollars. That’s what bridging a $400,000 gap cost her per month at her age and health rating.

She told me she almost didn’t do the math because she was afraid of what she’d find. I get that. Nobody wants to discover they’ve been underprepared. But the alternative — staying in the dark — doesn’t protect anyone.

Your family doesn’t need a round number. They need the right number. It takes 20 minutes and a calculator to find it.

Go find it.

About the Author

Selene Voss has spent 8 years writing about insurance, personal finance, and consumer advocacy. He has contributed to financial literacy programs at community health organizations across the Midwest and specializes in translating complex coverage decisions into plain-language guidance for everyday families.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Coverage needs vary by individual circumstance. All cost figures reflect 2026 published data and averages. Consult a licensed financial professional or insurance advisor before making coverage decisions