Last Updated: August 2026

A few links here are affiliate links. Small commission if you buy — zero extra cost to you, doesn’t change anything I recommend.

My uncle James died without life insurance.

48 years old. Heart attack out of nowhere. Three kids, a mortgage, and a wife who had to go back to work inside of two weeks because the bills don’t pause for funerals.

I bring that up because it’s the actual reason any of this matters. Life insurance isn’t really about death. It’s about what the living have to deal with after.

Not sure which type of policy you need yet? Start with our complete guide to life insurance, which covers term vs. whole, how much to buy, and what the costs really look like. So here’s best life insurance companies worth your money in 2026 — and why.

Before the Companies: The Two Numbers You Actually Need

Most people shop for life insurance backwards. They find a monthly payment they can live with, pick a policy type, and then shop for whoever’s cheapest.

Wrong order.

The company comes first. Because what you’re buying is a promise — a decades-long promise to pay your family a specific dollar amount when you die. If the company behind that promise is fragile or badly run, all those premium payments add up to exactly nothing.

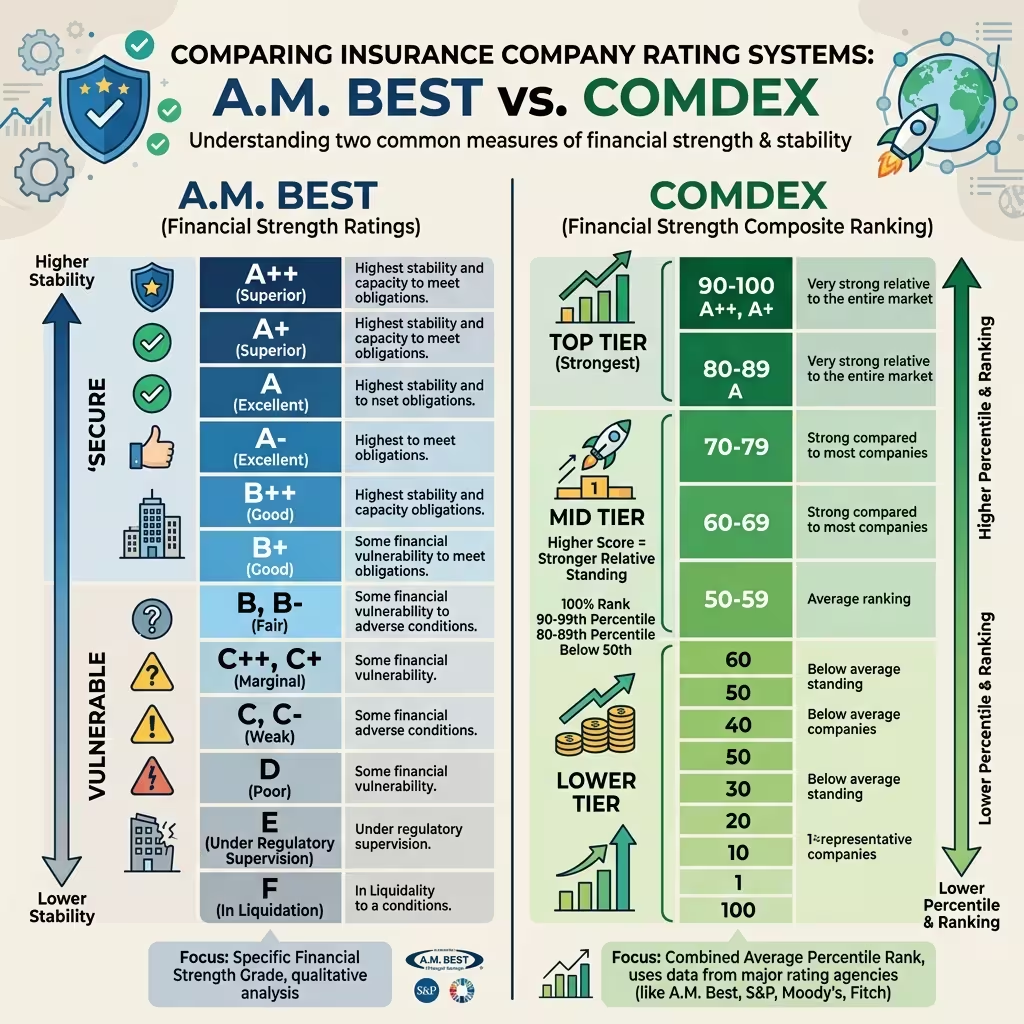

The A.M. Best rating is what tells you whether a company can actually keep that promise. They rate nothing but insurance companies. A++ is the top. I personally get uneasy recommending anything rated A- or lower for a long-term policy — the margin of safety gets thinner than I like.

Then there’s the COMDEX score. It averages the percentile rankings from A.M. Best, S&P, Moody’s, and Fitch into a single number between 1 and 100. Above 90 is strong. Above 95 is elite.

A perfect 100? Two companies in this entire market: Northwestern Mutual and New York Life.

That’s it. Two. I’d want you to sit with that for a second before we move into the rest of the list.

Northwestern Mutual

COMDEX 100. A.M. Best A++. 9.5% market share — largest of any US life insurer.

In 2026 they paid $9.2 billion back to policyholders. Not to Wall Street. Not to a board of directors optimizing quarterly returns. To policyholders — who are, technically, the owners of the company.

That’s the thing about mutual insurers that gets lost in typical comparison articles. Northwestern Mutual isn’t managed for shareholders because there aren’t any. The whole structure is built around one goal: keeping long-term promises. No pressure to juice short-term numbers. No activist investor threatening a dividend cut to fund a buyback. Just an insurer that has to answer to the same people it’s insuring.

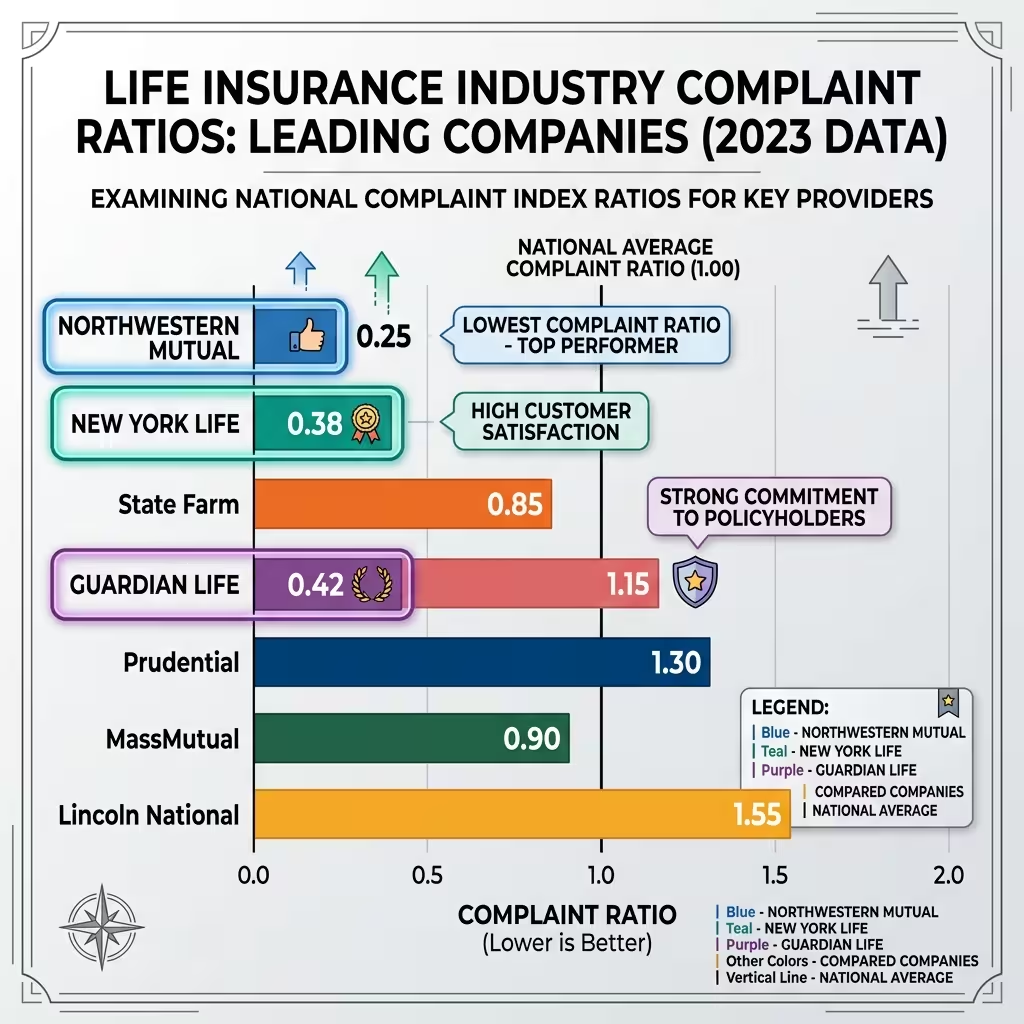

Their NAIC complaint index is 0.040. Industry average: 1.00.

I’ve never seen a complaint ratio that low at a company this size. Something is working.

Honest admission: they’re expensive, and you buy through an advisor rather than an app. If that bothers you, it bothers you. But for a permanent policy you’re holding for thirty years? I don’t know a stronger answer.

New York Life

172 years of consecutive dividends.

Not 172 years old. 172 straight years of paying dividends — through the 1918 flu pandemic, the Great Depression, every war, every recession, every financial crisis since the 1840s. In 2026 that streak continues. $2.8 billion paid out to policyholders.

COMDEX 100. A.M. Best A++.

They’re also the exclusive insurance partner of AARP, which matters more than most people realize. Other A++ carriers often get squirrelly about senior applicants in ways that don’t show up in marketing materials. New York Life actively builds products for the 60–85 window. If that’s you, or if that’s a parent you’re trying to get covered, the AARP partnership is real leverage.

Guardian Life

COMDEX 99. A++ from A.M. Best. Complaint ratio 0.099.

Those numbers aren’t what make Guardian worth talking about. Here’s what does.

Most carriers at this financial strength level get conservative fast when an application comes in with a complicated health history. Diabetes. Controlled hypertension. A cancer diagnosis from five years back that’s been fully resolved. These applicants often get declined outright or quoted rates so high the policy stops making financial sense. I’ve seen it happen repeatedly.

Guardian underwrites these situations differently. They have more flexibility at the A++ level than virtually anyone else in this tier. I’ve seen people get genuinely good rates from Guardian on applications that came back rated or declined from Northwestern Mutual and New York Life.

If you’ve already been told your health history is a problem somewhere else — try Guardian before you accept a simplified issue or guaranteed acceptance policy. The difference between a fully underwritten A++ policy and a guaranteed issue product isn’t small. It’s the difference between real coverage and a very expensive bandage.

MassMutual

98 COMDEX. A++ from A.M. Best.

Their Whole Life 100 product offers guaranteed cash value returns between 2% and 3.75%. That range sounds modest. In a 30-year policy, compounding that advantage over the industry average turns into a number that isn’t modest at all.

Something specific worth flagging for younger women: MassMutual prices more aggressively in that demographic than almost any other A++ carrier. Around $16 a month for a healthy applicant in her 20s or early 30s. That’s not a banner rate — that’s the actual price, consistently, at a company with top-tier financial strength.

The Paid-Up Additions rider is strong too. Lets you funnel extra premium directly into increasing cash value faster than standard policy growth. Penn Mutual competes in this space, but MassMutual’s guarantees are harder to beat.

Mutual of Omaha

Scores lower on raw financial strength than the companies above. Not in their tier on COMDEX.

But here’s the thing about financial strength ratings: they measure whether a company can pay your claim. They don’t measure whether dealing with that company feels like a root canal. And a lot of the A++ carriers are genuinely unpleasant to interact with on routine service issues.

Mutual of Omaha pulled 707 out of 1,000 satisfaction points in 2026 — surpassing State Farm for the top consumer satisfaction spot. Strong digital tools, agents who actually answer. Claims process that doesn’t feel like the company is trying to find a reason to say no.

I know plenty of people who’d trade a point or two on COMDEX for not dreading a call to their insurer. Mutual of Omaha is a legitimate answer for that person.

USAA

Military and their immediate families only.

If you qualify, run the USAA quote before you look at anything else. Not as one option among several — as the first quote you pull.

Wartime Coverage and a Severe Injury Benefit paying $25,000 for on-duty injuries. These don’t exist at any civilian carrier. Not as optional riders at extra cost. Not buried in a supplemental policy. Standard features.

The Life Event Option lets members increase coverage after marriage, a new child, or other milestones without going through a new medical exam. For someone whose life and deployment schedule can change dramatically and fast, that flexibility isn’t a minor detail.

Pacific Life

The carrier most people in the high-net-worth bracket end up with when the conversation is about estate planning rather than basic coverage. $1 million-plus policies. Wealth transfer. Complex trust structures. They lead the IUL market, and their complaint ratio — 0.090 — is almost absurdly low for a company handling that level of complexity.

The Index Lock feature on their IUL products is the one that gets talked about in financial planning circles. Policyholders can lock in market gains at any point during the year. That’s not a cosmetic feature. In a year with a mid-summer market run followed by a Q4 selloff, it’s the difference between keeping gains and watching them erode. Allianz pioneered it; Pacific Life implemented a version that works cleanly.

John Hancock

Nobody else in this market is doing what John Hancock is doing with the Vitality Program.

You earn points for exercising. For buying healthy groceries. For getting a flu shot. Points convert into premium discounts — up to 25% — plus actual external rewards: travel discounts, deals on fitness gear. For a younger policyholder who wants their insurance to participate in their life instead of just quietly draining their bank account, this is a genuinely different model.

Their Aspire program is built specifically for applicants managing diabetes. The underwriting treats it as an ongoing managed condition rather than a hard disqualifier. That’s not standard. Most carriers see a diabetes diagnosis and start pricing aggressively or declining. Aspire treats it like what it often is: a managed condition with real data behind it.

The Number That Should Bother You

$61.68 a month. That’s what a healthy 40-year-old male pays for $500,000 in 20-year term coverage.

Wait until 50. That same policy is $155.47 a month.

146% increase for ten years of delay. The top life insurance companies in America are excellent at many things. Overriding actuarial math is not one of them.

Which Company Pays Claims Fastest

Ethos and SBLI built their whole model around this. No medical exam for coverage up to $1 million. 94% of applicants get a same-day decision. If speed is a priority, our guide to no-exam life insurance explains every path to fast approval — from accelerated underwriting to guaranteed issue. The same digital infrastructure that handles applications fast also handles claims fast — there’s no paper file sitting on someone’s desk waiting to be reviewed.

Traditional carriers: Northwestern Mutual and Guardian. The complaint ratios tell you something real about how the claims process actually goes for most people. When almost nobody is filing complaints at a company this size, the claims process is either genuinely smooth or the customers are extraordinarily easy to satisfy. I think it’s the former.

Transamerica: complaint ratio 4.709. Nearly five times the industry average. The premium looks attractive until the policy actually needs to perform. I’ve seen this pattern enough times — cheapest price, worst friction when it counts.

Three Policy Types, Quickly

Term. Fixed premium. 10, 20, or 30-year window. Your family gets paid if you die during that period. Policy ends if you don’t. Banner Life and SBLI run 15%–30% cheaper than the big mutual companies on term products. Clean product. Cheapest entry point. Nothing wrong with it.

Whole life. Builds cash value on top of the death benefit. Think of it as a conservative financial asset that also happens to guarantee a payout when you die. The returns are modest, guaranteed, and genuinely useful in a volatile market when you want something that doesn’t go down. MassMutual and Northwestern Mutual own this space.

IUL — Indexed Universal Life. Cash value growth tied to a market index. Typically the S&P 500. There’s a floor — usually 0% — that protects you when the index drops. There’s also a cap that limits how much upside you capture. IUL is 25% of all new US life insurance premiums in 2026. $3.8 billion. Pacific Life and Allianz lead the category. This stopped being an obscure product years ago.

People Also Ask – PAA’s

Most reliable life insurance company in America in 2026?

Northwestern Mutual or New York Life — only two companies in the US market with a perfect COMDEX score of 100 and A++ from A.M. Best. If I’m picking one: Northwestern Mutual. $9.2 billion in dividends paid in 2026, complaint ratio of 0.040 at a company with 9.5% market share. That combination doesn’t happen by accident.

Haven Life vs. Bestow?

Haven Life is underwritten by MassMutual. A++ financial strength behind the policy. Bestow is an agency — it distributes policies issued by North American Company for Life and Health. Both skip the medical exam for most applicants. Both are fast. The question is what backs the policy itself. Haven Life has the stronger answer on that.

Which company pays claims fastest?

Digital: Ethos and SBLI — same-day decisions, fast claims. Traditional: Northwestern Mutual and Guardian — complaint ratios so far below the industry average the data speaks for itself. Anyone with a complaint ratio above 2.0 is a risk for slow, friction-heavy claims. Transamerica at 4.709 is where I’d draw the hardest line.

Just turned 50 and never bought life insurance. What now?

New York Life first — the AARP partnership makes them the most accessible A++ carrier for this age group. Guardian second, especially if health history complicates the application. Both can get someone into real coverage at 50 without the kind of underwriting scrutiny that pushes people into guaranteed issue products they don’t need.

Nationwide for young men?

$33 a month for healthy young men in their 20s puts them in genuinely competitive range. Not a top-tier financial strength story. Solid enough, and the price at that age makes the conversation worth having.

James

He would have paid $60 a month. Maybe $55 — he was healthy, late 30s, would have gotten a good rate.

The mortgage would have been covered. His wife wouldn’t have had to choose between the electric bill and groceries inside of a month. His kids wouldn’t have changed schools.

He thought he had more time than he did. Most people do.

The best life insurance companies in America cannot do anything for you until you actually buy a policy. The math on waiting is brutal. The cost of being wrong doesn’t come due until it’s too late to pay it differently.

Get the quote today.

About the Author Written by a financial content team covering US personal insurance, life insurance markets, and consumer protection. Research draws from A.M. Best 2026 ratings, NAIC complaint index reports, COMDEX composite rankings, and carrier-published dividend and satisfaction data.

Disclosure: Some links in this post may be affiliate links. If you purchase through them, I may earn a small commission at no extra cost to you. Doesn’t change what I recommend.

Disclaimer: Rates, ratings, and product details here reflect publicly available data as of August 2026. Products vary by state and health profile. Consult a licensed insurance professional before making coverage decisions.