Last Updated: April 2026

Priya didn’t ask questions at open enrollment. Nobody does, really.

She was a radiologist at a large Houston hospital system. Good salary. Good benefits package. When HR sent the annual enrollment email, she clicked through, selected the long-term disability option, and moved on to the next item in her inbox. She figured if the hospital was offering it, it was probably fine.

Three years later, she was diagnosed with multiple sclerosis.

The claim got filed. The insurer started paying. And then Priya’s financial advisor sat her down and walked her through something she’d never actually looked at — the policy itself. What he showed her was three separate problems she hadn’t known existed.

First: the benefit was taxable. Because the hospital paid her premium, every check from the insurer counted as ordinary income. Her 60% income replacement was closer to 40% after federal and state taxes.

Second: at month 25, the definition of disability was going to change. Own-occupation for the first two years. Any-occupation after that. At month 25, the insurer could argue she was capable of sedentary radiology work — reviewing scans remotely, consulting — and cut her off.

Third: if she ever left the hospital, the policy didn’t come with her. It stayed with her employer. Gone.

That’s what individual vs group disability insurance actually looks like when it gets tested. Not on a comparison chart — in real life, with a diagnosis, a calculator, and a clock ticking toward month 25.

Before getting into the specifics, it helps to understand how disability insurance works at the policy level. Our complete disability insurance guide for 2026 covers the core mechanics — definitions, elimination periods, and benefit structures — that apply to both plan types.

Disclosure: Some links in this post connect to independent insurance brokers. We may receive a referral fee if you connect through our links. Our editorial positions aren’t influenced by that.

The Gap Between “Covered” and Actually Protected

Most people with employer-provided disability insurance believe they’re covered. They’re not wrong, exactly. The policy exists. The premiums are being paid. A claim would probably trigger some kind of benefit.

But “some kind of benefit” and “enough benefit to maintain your financial life while disabled” are two very different things. That gap — between what group LTD provides and what a high earner actually needs — is where supplementing group LTD with an individual policy becomes not just smart but often necessary.

Here’s what the gap looks like in numbers.

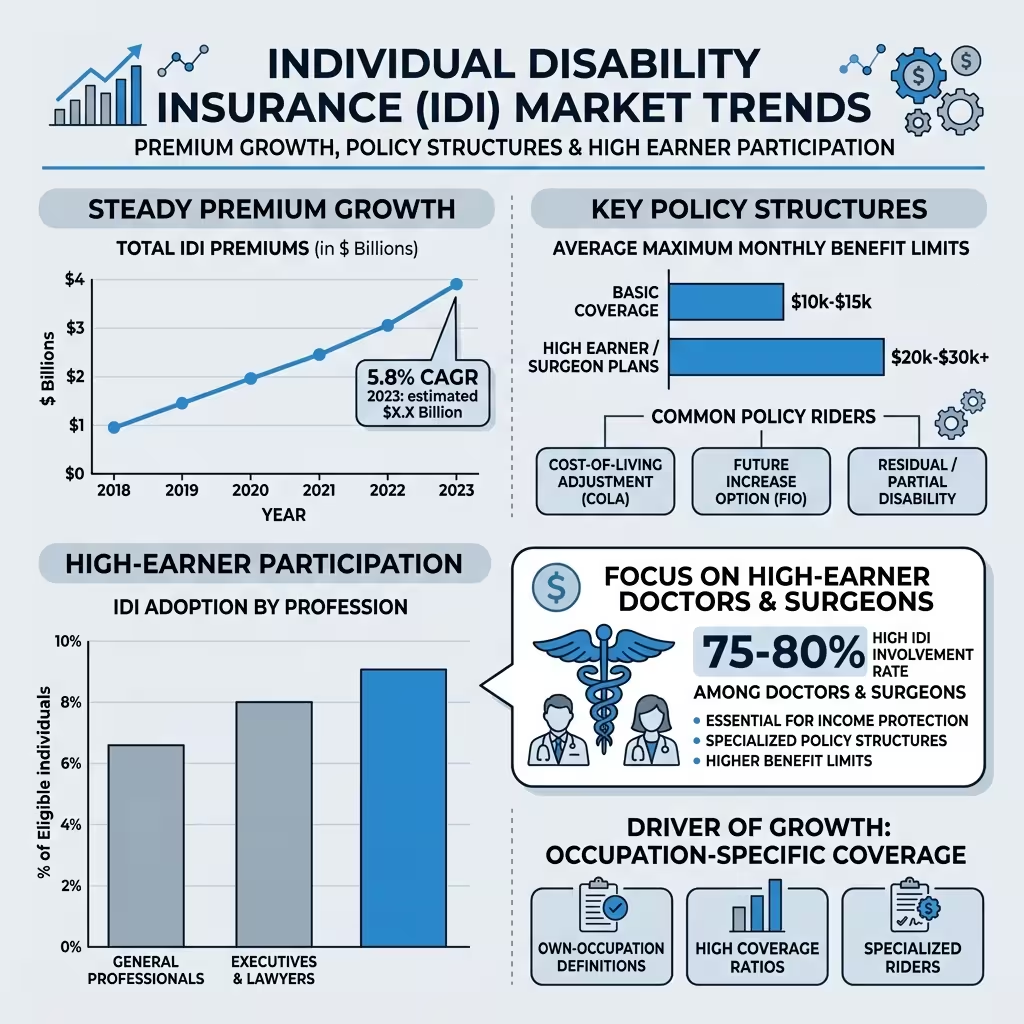

The U.S. individual disability income market issued $423 million in new annualized premium in 2024, according to the Milliman 2025 IDI survey. The number of new individual policies actually increased 0.7% even as premium volume dipped slightly — more people buying, at different price points. The market is growing because more professionals are figuring out what Priya’s advisor figured out for her. Group coverage has structural limits that individual policies don’t.

What are those limits? There are four of them. And every high earner should understand all four before their next open enrollment.

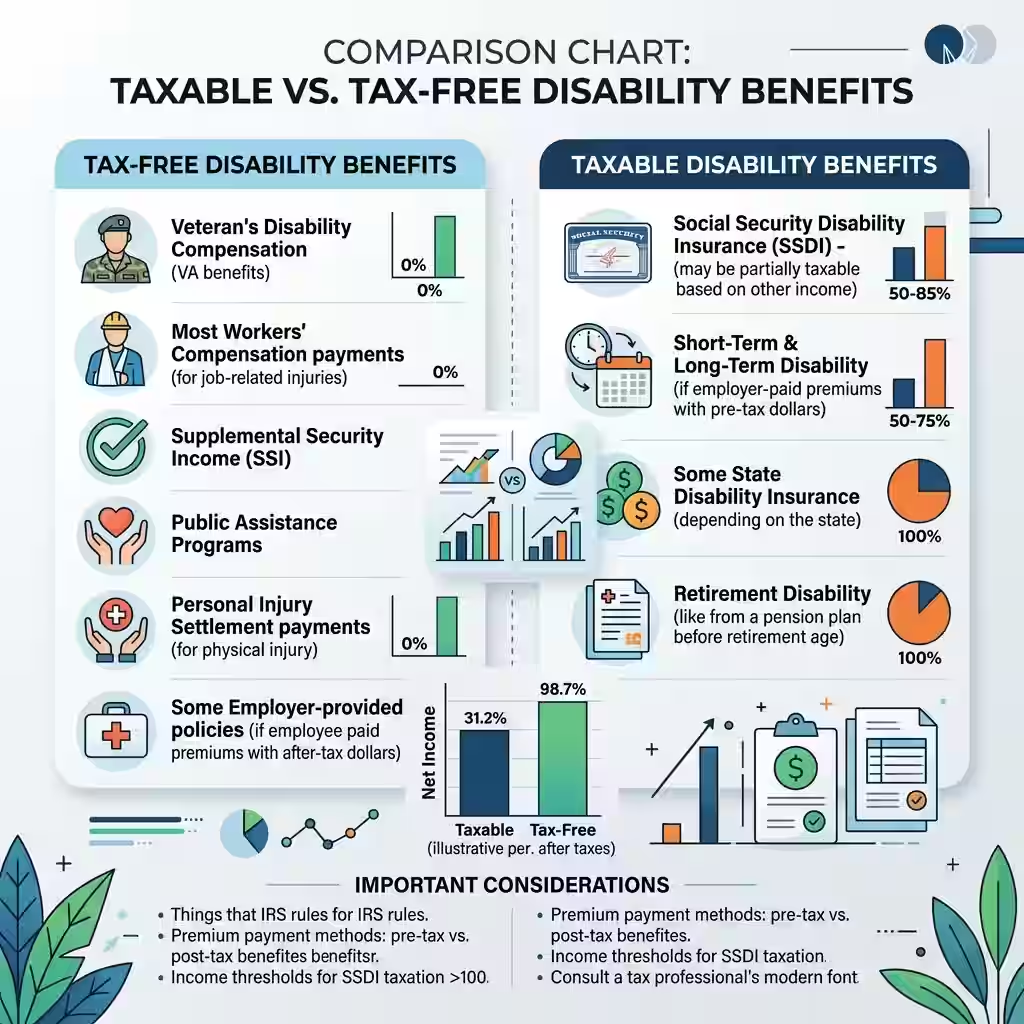

Problem One: The Tax Trap

Let’s start with the one nobody talks about at open enrollment.

Whether your disability benefit is taxable depends entirely on who paid the premium. One factor. That’s it.

If your employer pays the employer-provided disability insurance premium — or if you pay it through a pre-tax payroll deduction — your benefits are taxable as ordinary income when you receive them. The IRS treats them the same as a paycheck.

If you pay with pre-tax premiums through salary reduction, same result. Taxable.

Pay with after-tax dollars on an individual policy you own personally? Benefits arrive tax-free. Every dollar.

There’s also a tax consequence that catches most people off guard: when your employer pays the premiums on your group plan, any benefits you receive are taxable income. See are disability insurance benefits taxable for the full explanation.

Why does this matter? Do the math on a real salary.

An anesthesiologist earning $380,000 a year has a group LTD plan promising 60% income replacement. That’s $228,000 annually on paper. But if that benefit is taxable at an effective rate of 35%, the actual check is about $148,200. That’s a $79,800 annual gap against a household built on $380,000. Against a mortgage, practice loan payments, kids’ tuitions — that gap isn’t a rounding error. It’s the difference between maintaining a life and fundamentally changing it.

Individual policies paid with after-tax dollars don’t have this problem. The $228,000 is $228,000. That’s the whole point of owning one privately.

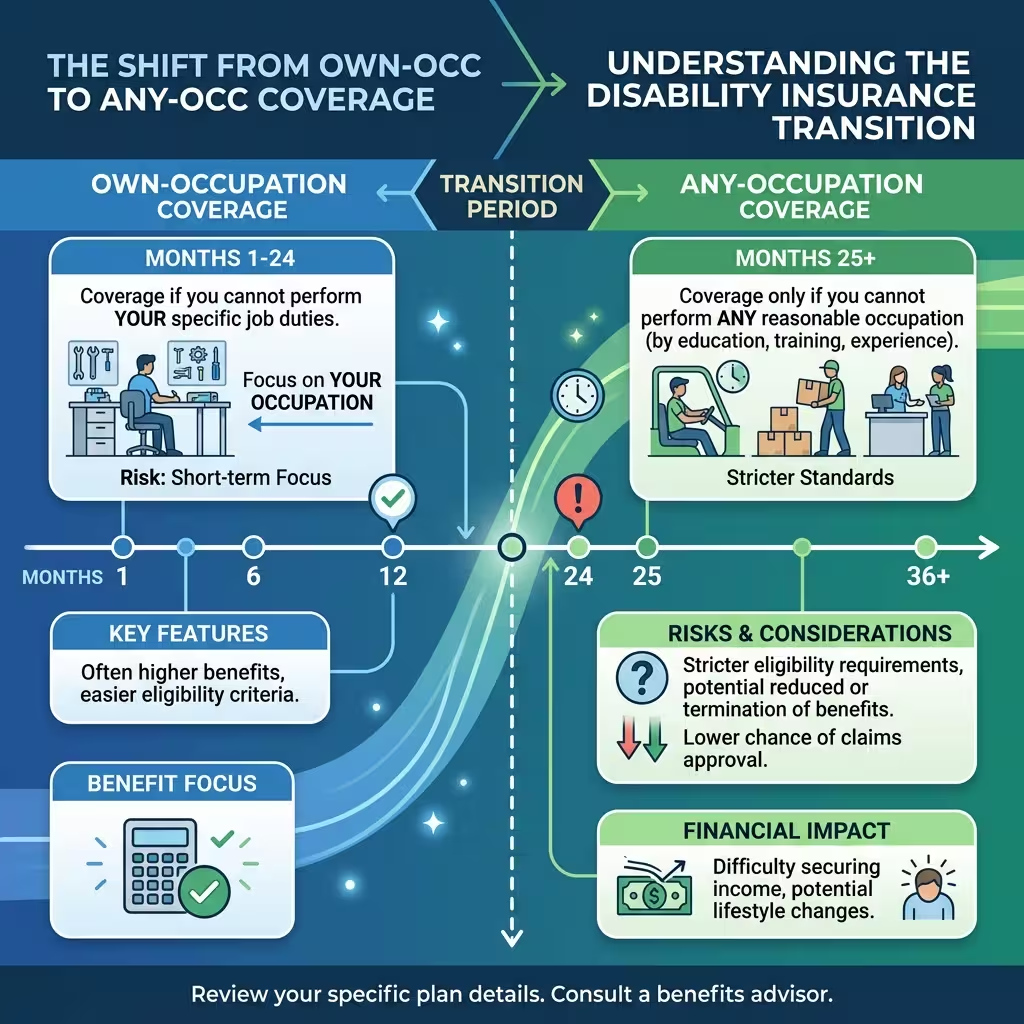

Problem Two: The 24-Month Trap

This is the clause most group plan holders have never read.

Most employer-provided disability insurance plans use a two-phase definition of disability. For the first 12 to 24 months of a claim, benefits are paid under an “own-occupation” standard — meaning you’re considered disabled if you can’t perform the duties of your specific job. Reasonable enough.

At month 25, the definition automatically switches to “any-occupation.” Now you’re only considered disabled if you can’t perform any job you’re reasonably qualified for by education, training, or experience.

For Priya, that meant the insurer could argue she was capable of remote radiology work — reviewing scans from home, providing written consults, performing functions that don’t require physical presence. She couldn’t stand at a workstation for long periods. She had fatigue and intermittent vision issues. But she could theoretically do some form of radiology work.

Under any-occupation, theoretically is enough.

This isn’t hypothetical. As of 2026, 71% of insurance companies use AI-driven claims review to flag cases for denial — particularly at the 24-month mark. These systems scan medical records looking for evidence of function. They’re not looking for evidence of limitation. The two aren’t the same thing, but the algorithm doesn’t always know the difference.

Individual policies with true own-occupation language don’t have this switch. They keep the same definition — can you perform the duties of your specific occupation — for the entire benefit period. No automatic flip. No month-25 cliff.

For radiologists, surgeons, dentists, and any specialist whose income is tied to a specific set of clinical skills, that consistency is the entire value proposition of an individual policy.

Problem Three: Portability

Group disability insurance stays with your employer. Not with you.

Leave the hospital, leave the law firm, leave the company — the group LTD policy stays behind. You don’t convert it. You don’t transfer it. You start over, and if your health has changed since you originally enrolled, starting over means going through medical underwriting again. With whatever pre-existing conditions you’ve accumulated in the meantime.

Priya’s MS diagnosis, for instance. If she ever left her hospital and tried to purchase new disability coverage afterward, the MS would likely trigger an exclusion rider or a premium increase, depending on the carrier and the progression of her condition. The group plan she had when she was healthy — and that felt like a safety net — can’t be taken with her.

Individual disability policies are portable. You own them. They travel with you through every job change, every career shift, every time you decide to leave a large employer and go into private practice or start your own firm. The rates you locked in when you were 32 and healthy stay locked in — assuming you bought a noncancelable policy, which brings us to the next point.

The Noncancelable Advantage

Eighty-five percent of new individual disability income premium in 2024 was issued on noncancelable (noncan) policies, according to Milliman’s survey. For physicians specifically, that number hits 96%.

Here’s why that matters.

A noncancelable policy guarantees two things: the insurer cannot cancel your coverage, and they cannot raise your premium as long as you keep paying. The rates you agreed to on day one are the rates you’ll pay at 45, at 55, at 62. Even if you develop a chronic condition. Even if your occupation’s risk profile changes. Even if the insurer would rather not cover you anymore.

Group plans have no such guarantee. Employers can change carriers, reduce coverage, or eliminate the benefit entirely. You find out at open enrollment, usually without much warning.

The definition of disability is the single biggest quality gap between group and individual plans. We cover this distinction in depth in our guide to own-occupation vs any-occupation disability insurance.

For anyone buying disability coverage with a long-term view — which should be everyone, since that’s the whole point — a noncancelable individual policy is the only version that locks in both coverage and cost.

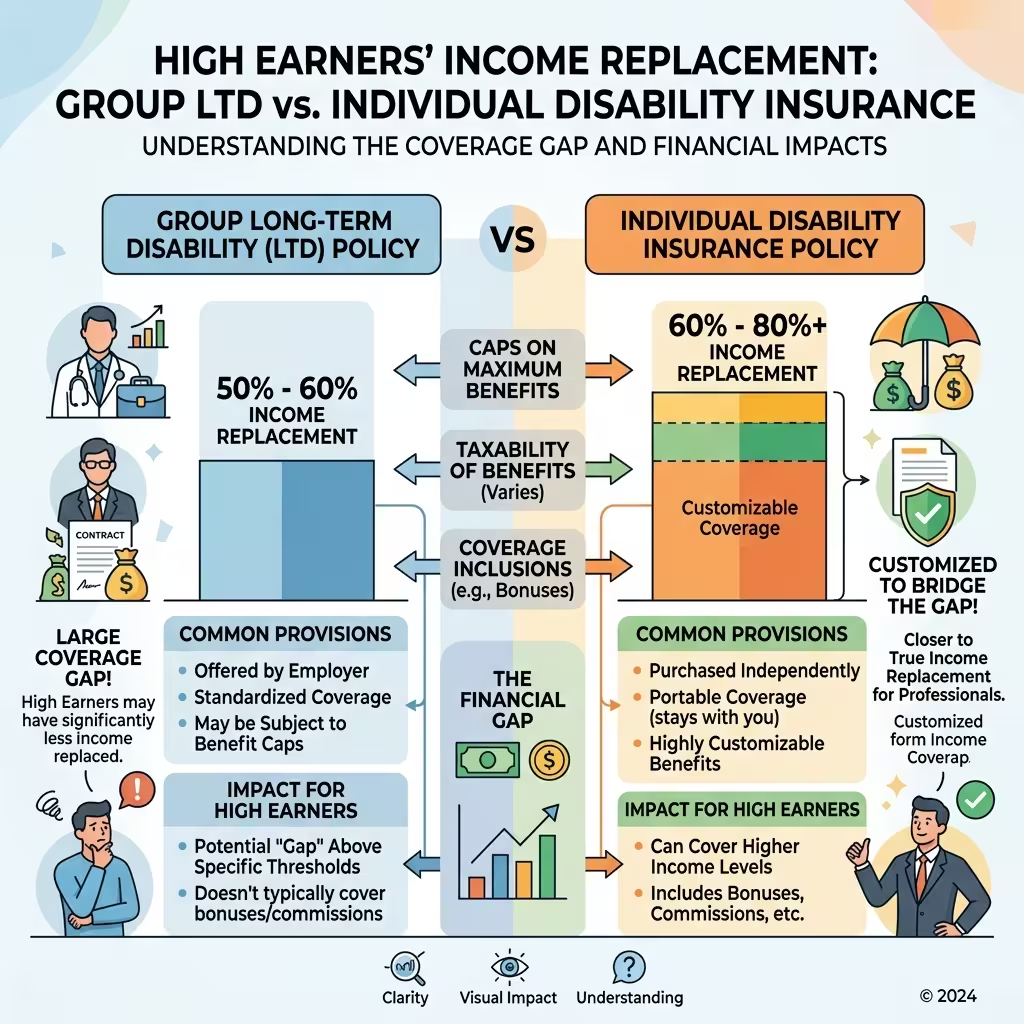

Is Employer Disability Insurance Enough for High Earners?

Short answer: usually not. Longer answer: it depends on how you define “enough.”

For a worker earning $55,000 a year, a group LTD plan paying 60% — even a taxable 60% — may produce something workable. The gap between the benefit and baseline living expenses might be manageable.

For a physician earning $450,000, a dentist at $280,000, a partner at a law firm making $600,000 — the taxable benefit, the any-occupation switch at month 25, and the annual benefit cap on most group plans combine to produce a replacement that falls far short of what those incomes support.

Most group plans cap benefits at $10,000 to $15,000 a month. Some go higher, but caps are standard. On a $450,000 salary, $10,000/month is $120,000 a year — roughly 27% income replacement before taxes eat into it further.

That’s not coverage. That’s a floor that’s much lower than most high earners realize they’re standing on.

The Core-and-Satellite Strategy

Here’s the approach independent brokers recommend most consistently for high earners, and it doesn’t require choosing one over the other.

Keep the group plan. It’s low-cost or employer-subsidized. It provides a baseline benefit that costs you very little or nothing. There’s no reason to walk away from it.

Add an individual policy alongside it — a true own-occupation policy with a noncancelable premium guarantee, a benefit period to age 65, and a residual disability rider. This is the “satellite” that fills the gap. It’s portable. It’s tax-free on the benefit side. It doesn’t flip definitions at month 25. And it protects the income that the group plan cap doesn’t reach.

The combination — group LTD as core, individual own-occ as satellite — produces the coverage structure that actually mirrors what high earners need. Not as a marketing concept. As a functional financial safety net.

One more piece worth adding: a COLA rider. This adjusts monthly benefits for inflation during a long-term claim — typically 3% compounded annually. It only activates after the first 12 months on claim, but on a disability that lasts a decade or more, the difference between a fixed benefit and one that keeps pace with inflation is substantial. COLA riders add roughly 40% to the premium cost, so the decision is a real one. For younger professionals locking in coverage that might pay out for 20-plus years, it’s usually worth it.

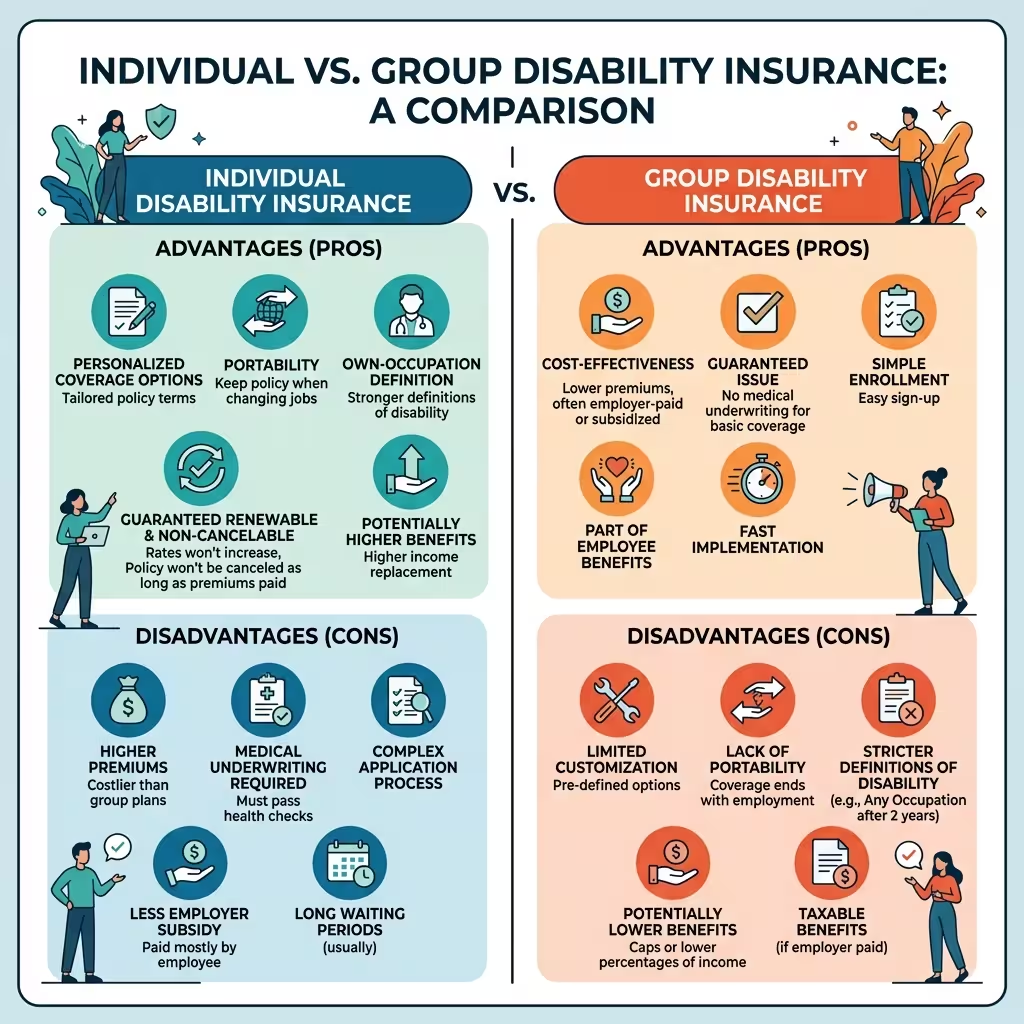

The Pros and Cons of Private Disability Insurance

No coverage type is perfect. Here’s an honest look at both sides.

Individual policy advantages:

- Portable — stays with you regardless of employer

- Tax-free benefits when paid with after-tax dollars

- Noncancelable — rates locked in permanently

- True own-occupation definitions that don’t switch

- Higher combined benefit potential when layered over group coverage

Individual policy disadvantages:

- Requires medical underwriting — health history matters at application

- Higher premiums than group coverage (you’re not sharing the pool)

- Must be purchased while healthy; pre-existing conditions can trigger exclusions

- Requires working with a broker to compare contracts — not a quick online purchase

Group plan advantages:

- Low or no out-of-pocket cost if employer pays the premium

- No medical underwriting at initial enrollment

- Immediate coverage — no waiting period to apply

- Simple — no broker meetings, no contract review required

Group plan disadvantages:

- Not portable when you leave the employer

- Taxable benefits if employer pays the premium

- Definition of disability typically switches at 24 months

- Benefit caps often insufficient for high earners

- Subject to employer changing carriers or eliminating coverage

Once you know what your group plan covers, the next question is whether it’s enough. Our disability insurance benefit calculator guide helps you figure out exactly how much additional coverage to layer on.

The honest framing: group coverage is a good starting point that most high earners outgrow. Individual coverage is the layer that turns that starting point into actual protection.

What the Market Looks Like Right Now

The individual disability income market had $423 million in new annualized premium in 2024. Doctors and surgeons alone represented 33% of total new premium — and for some carriers, over 70%. That tells you who this market is really built for.

The 90-day elimination period is the most common choice, used in 73% of new policies. “To age 65-70” benefit periods account for 84% of new coverage. These are the standard structures for a reason — 90 days matches a typical professional’s emergency fund, and a to-age-65 benefit period is the only one that covers the actual window of risk.

Issue limits for top medical and nonmedical occupations now reach $35,000 monthly at some carriers. When a group LTD plan is already in place, some carriers allow participation up to $40,000 monthly combined. The math can be made to work for very high earners — but only with an individual policy filling the gap between the group cap and the actual income replacement needed.

People Also Ask – PAA’s

What’s the main difference between individual vs group disability insurance?

Group disability is employer-provided, often low-cost or free, but not portable and typically taxable. Individual disability is privately owned, portable, and produces tax-free benefits — but requires medical underwriting and costs more. The definitions of disability also differ significantly, especially after 24 months on a group claim.

Is employer disability insurance enough for high earners?

Usually not. Group plans typically cap benefits at $10,000–$15,000/month, switch to any-occupation definitions after 24 months, and produce taxable benefits. For professionals earning $200,000 or more, these three factors together often create a gap that individual coverage is designed to fill.

What does supplementing group LTD actually mean?

It means adding an individual true own-occupation policy alongside your existing group coverage. The group plan provides the baseline. The individual policy fills the gap — higher benefit, better definition, portable, and tax-free on the benefit side.

What is a noncancelable disability policy?

A policy where the insurer can’t raise your premiums or cancel your coverage as long as you keep paying. The rates you locked in when you applied are guaranteed for life. Most new individual disability policies (85% of new premium in 2024) are issued on noncancelable terms.

What is a COLA rider and should I add it?

A COLA (Cost of Living Adjustment) rider increases your monthly benefit each year during a long-term claim to keep pace with inflation — typically at 3% compounded annually. It activates after 12 months on claim. It adds about 40% to the premium cost, so it’s a real financial decision. For younger professionals whose coverage might pay out for 20-plus years, it’s typically worth it.

What are the pros and cons of private disability insurance?

Pros: portable, tax-free benefits, locked-in rates, better policy definitions. Cons: requires medical underwriting, higher premium than group coverage, must apply while healthy. For most high earners, the pros significantly outweigh the cons — especially since the group plan’s cons tend to surface at the worst possible moment.

What happens to my group disability plan if I leave my employer?

The coverage ends. It doesn’t convert or transfer. You’d need to apply for new individual coverage, going through medical underwriting at whatever your health status is at that point. If your health has changed, that can mean exclusions, higher rates, or difficulty obtaining coverage at all. This is the portability risk that individual policies eliminate.

What Priya Did

Her financial advisor walked her through all three problems in one meeting. The tax issue, the definition switch, the portability gap.

She bought an individual true own-occupation policy — specialty-specific, because radiology is specific enough to warrant it. Noncancelable. Benefit period to 65. Paid with after-tax dollars, so the benefit is tax-free. A residual rider covering partial disability. And a COLA rider, because she was 39 and hoping not to need it for twenty-five years.

The group plan stayed. She kept it. It’s the core. Low cost, employer-subsidized, and worth having as a baseline even with its limitations.

The individual policy is the satellite. The part that actually covers the income the group plan doesn’t reach, with a definition that won’t flip at month 25, and a contract that travels with her no matter where she works next.

That’s the whole structure. Not complicated. Just requires understanding the gap exists before the claim does.

Individual vs group disability insurance isn’t a choice between two equal options. It’s a baseline and the protection that makes the baseline useful. For high earners, finding out which one you have — and which one you’re missing — is worth doing before you need to find out the hard way.

About the Author

Selene Voss has written about personal finance, income protection, and U.S. insurance markets for eight years. He has reviewed disability contracts across more than a dozen carriers and covered ERISA litigation, IDI market trends, and professional coverage strategy for financial literacy publications. He holds no insurance licenses and does not sell products.

This article is for informational purposes only. It does not constitute financial, legal, or insurance advice. Policy terms, premiums, and benefit structures vary by carrier, state, and individual underwriting profile. Consult a licensed independent insurance broker before making coverage decisions. Market figures reflect 2024–2026 publicly available industry data.