Last Updated: April 2026

Dana didn’t think the definition section mattered.

She was a trial attorney in Chicago. Twelve years of litigation work, a solid book of business, good income. When her firm’s HR team sent over the open enrollment packet, she enrolled in the long-term disability plan the way most people do — quickly, without reading the fine print, assuming that “covered” meant covered.

Then came the diagnosis. A neurological condition affecting her ability to stand for long periods, manage the physical demands of courtroom work, track rapid back-and-forth during cross-examination. Her neurologist documented everything. She filed a claim. The insurer acknowledged the diagnosis.

And then the insurer said she wasn’t disabled.

Because Dana could still do legal research. She could review documents. She could take phone calls. She couldn’t try cases, but she could theoretically do sedentary legal work — and under her policy’s language, that was enough to disqualify her from benefits.

She had disability insurance. She just didn’t have the right definition of disability.

That distinction — own occupation vs any occupation — is what this post is actually about. It’s the most important clause in any disability policy, and most professionals never read it until the moment they desperately need it to say something different than what it says.

For a complete foundation on how disability insurance works — including elimination periods, benefit periods, and policy structure — our 2026 disability insurance guide covers all of it in one place.

Disclosure: Some links in this post are referrals to independent insurance brokers. We may receive compensation if you connect with a broker through our links. Our editorial positions aren’t influenced by that.

Why the Definition Is the Only Part That Really Matters

Most people compare disability policies on price. Monthly premium. Benefit amount. Elimination period. Those things matter. They’re not wrong to look at.

But here’s what gets missed: two policies with identical premiums and identical monthly benefits can produce completely opposite outcomes at the moment of a claim based on one clause buried in the contract. The definition of disability.

This isn’t a technicality. It’s the entire mechanism of the policy. It determines whether your claim gets paid. Whether it keeps getting paid at month 25. Whether the insurer can legally terminate your benefit while you’re still sick, still unable to do your actual job, still watching your income disappear.

If you’re a surgeon, a dentist, a physician, a trial attorney, or any professional whose earning capacity is tied to a specific set of trained skills — the definition of total disability in your policy is the most important financial document you own. More important than the premium. More important than the carrier name.

Let’s break down what these definitions actually say.

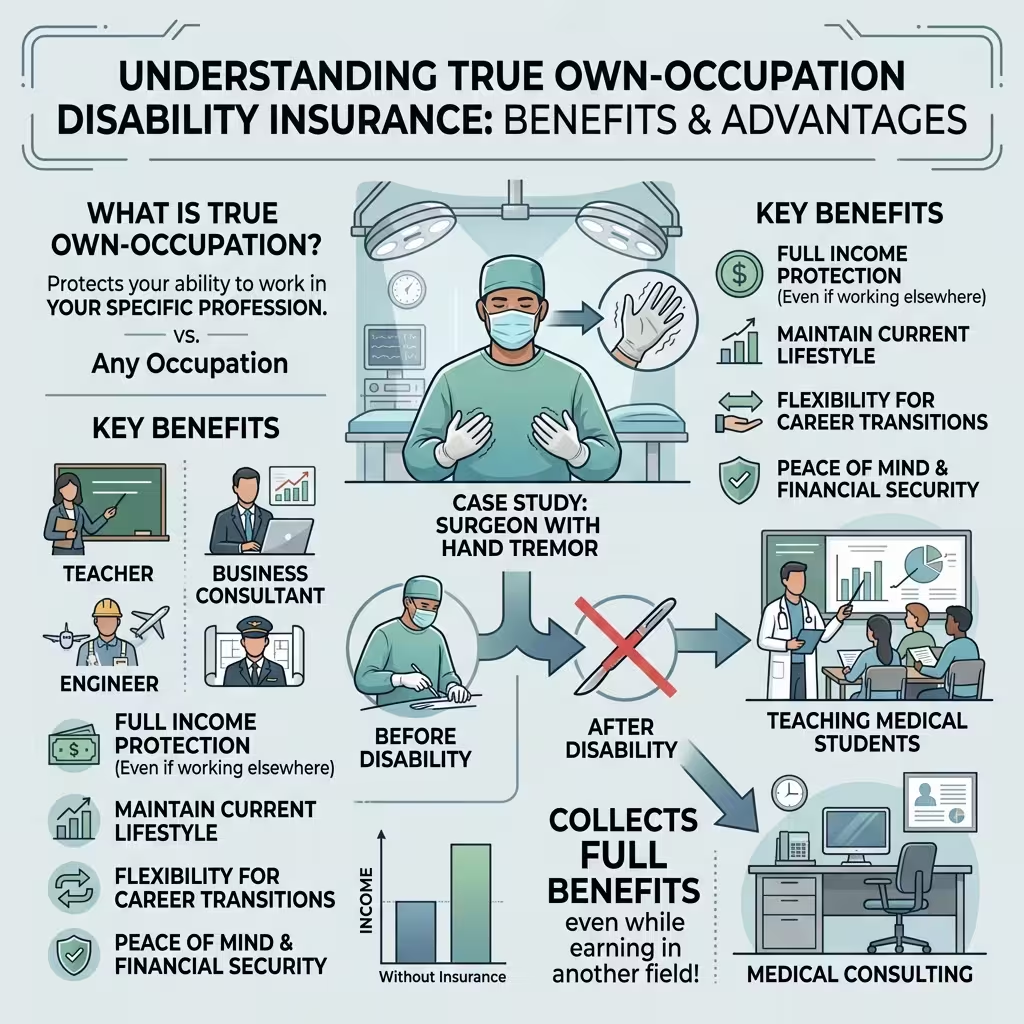

Own-Occupation: What It Means and Why It’s the Standard Worth Holding Out For

True own-occupation coverage pays benefits if you can no longer perform the material and substantial duties of your specific occupation — even if you choose to work in a completely different field.

Read that again, because it’s the part most people miss.

You collect full benefits. You can still work somewhere else. You can teach, consult, write, advise, manage — whatever you’re capable of. The policy doesn’t care. The trigger is whether you can perform the job you had when the disability began. That’s it.

For a neurosurgeon who develops a hand tremor, true own-occ means she can collect her full disability benefit while taking on a medical consulting role or teaching at a university. The policy pays because she can’t operate. Not because she can’t earn anything, anywhere.

Physicians and surgeons are the professionals where this distinction matters most. Our guide to disability insurance for physicians explains exactly what to look for in a specialty-specific policy.

There’s also a refinement called specialty own-occupation — or specialty-specific coverage — designed specifically for medical professionals. Under this version, benefits are tied to your specific clinical specialty, not just the broader category of “physician.” A pediatric dermatologist who can’t practice dermatology isn’t reclassified as a general practitioner. An orthopedic surgeon who can no longer operate isn’t told he can still do psychiatric consultations. The coverage protects the specialty he actually trained for.

This is the gold standard. And it’s what makes disability insurance genuinely useful for high-skill professionals.

Any-Occupation: The Version That Sounds Like Coverage Until You Need It

Any-occupation coverage only pays if you can’t work in any job you’re reasonably suited for by education, training, or experience.

This any-occupation switch is especially common in group plans. If you’re comparing what your employer offers against individual coverage, the differences go far beyond just the definition — see individual vs group disability insurance for the full breakdown.

That phrase — “reasonably suited” — is doing enormous work in that sentence. Under any-occupation standards, insurers routinely argue that a trial attorney who can’t stand in a courtroom can do sedentary legal research. That a surgeon who can’t operate can consult. That a construction manager who can’t be on a job site can do administrative work.

Sound familiar if you’re reading this as a professional? It should. This is exactly what Dana ran into.

The insurer doesn’t need to prove you can do your old job. They just need to find some job — often a lower-paying, generalized role that loosely relates to your background — and argue you’re theoretically capable of it. At that point, under any-occupation language, the gainful employment test is satisfied and the claim fails.

Here’s the part that makes this especially dangerous in 2026: insurers now use computer-generated Transferable Skills Analyses (TSAs) to identify alternative occupations based on your background. These tools scan your work history and generate a list of jobs you could theoretically perform — often without the insurer ever speaking to you directly, your doctor, or anyone who’s actually seen how your condition affects your professional duties.

Seventy-one percent of insurers now use AI tools in claims adjudication. When UnitedHealthcare integrated AI into its disability review process, its denial rate more than doubled. Lawsuits have alleged error rates as high as 90% for certain AI tools used in these reviews. The system isn’t neutral. It’s built to find functionality, not to assess it honestly.

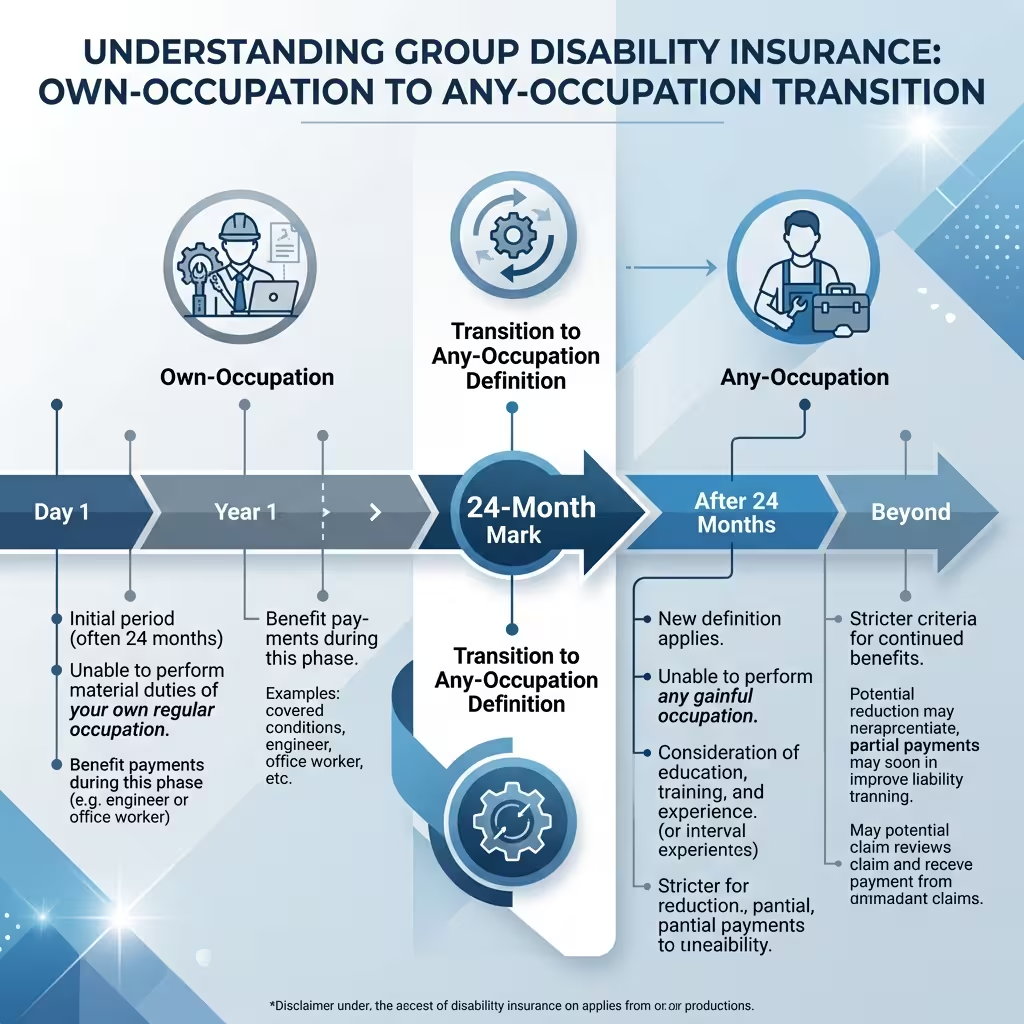

The 24-Month Trap — Where Most Group Plans Fall Apart

Here’s the thing that catches most professionals off guard. They read their group plan summary and see “own-occupation coverage.” They assume they’re protected.

They’re protected. For two years.

Most employer-sponsored group LTD policies use a hybrid structure. Own-occupation language for the first 12 to 24 months. Then an automatic switch to any-occupation after that. It’s written into the policy. It’s legal. And most people don’t find out about it until month 25, when the insurer sends a letter saying the definition of disability has changed.

This isn’t an edge case. It’s standard practice in group plans.

Insurers know exactly what they’re doing. Statistically, month 25 is when partial recoveries cluster — when a claimant is functional enough to work in some capacity but not well enough to return to their actual job. Under own-occupation, they’d still collect benefits. Under any-occupation, the insurer has grounds to terminate.

If you have a group plan — employer-provided, association-provided, or through a union — pull the actual policy document. Not the summary. The contract. Find the definition section. Find what it says at month 25. Know what you have before you ever need to file.

ERISA Makes This Even Harder Than It Sounds

Most employer-sponsored disability plans are governed by ERISA — the Employee Retirement Income Security Act. Without going into a full legal lecture, ERISA creates significant structural advantages for insurers over individual claimants.

No jury trials. Federal judges only. No punitive damages. No compensation for pain and suffering, even if the denial was clearly improper.

Here’s the one that matters most practically: if you need to appeal an ERISA denial and eventually take it to court, you generally can’t introduce new evidence. The case is decided on the “administrative record” — meaning the documents already in the insurer’s file. If your claim file is thin, if your doctor’s notes are incomplete, if your functional limitations weren’t documented carefully from the beginning, you’re building your legal case on a foundation you can no longer fix.

The 180-day internal appeal deadline is real. Miss it and you typically lose all benefit rights permanently.

I’ll be direct: filing an ERISA disability claim without legal counsel at the appeal stage is a mistake. The internal appeal process feels designed for claimants but it frequently functions as evidence-gathering for insurers. Don’t navigate it alone.

Why Surgeons and Specialists Need Own-Occupation Coverage — And What It Actually Costs

If you’re a physician, surgeon, dentist, or any licensed specialist, this section is specifically for you.

The combination of any-occupation language and occupational misclassification is particularly brutal for specialists. Insurers routinely reclassify:

- A pediatric dermatologist as a generic “physician”

- A trial attorney as a “lawyer” who can do sedentary document review

- A surgical nurse as a general “nurse” who can work in case management

Under this logic, why surgeons need own-occupation disability insurance becomes obvious. A surgeon who can no longer operate isn’t just “a doctor who can’t do one thing.” She’s lost the specific skill set she spent a decade developing, the income attached to that skill set, and the professional identity built around it. Any-occupation coverage treats that loss as irrelevant, as long as she can theoretically do something medical.

Specialty own-occupation coverage protects against this. It pays if she can’t perform her specific specialty — not just if she’s broadly unable to work in medicine.

On cost: physician disability premiums vary by specialty risk class. In 2026, estimated monthly costs per $1,000 of monthly benefit run roughly:

- Psychiatry, Pathology, Administration (lowest risk): $15–$25

- Family Medicine, Radiology, Anesthesiology: $25–$40

- Orthopedic Surgery, Neurosurgery (highest risk): $50–$75

For a surgeon wanting $10,000/month in benefits, that’s $500–$750/month. Against an income of $400,000–$500,000 a year, the math is clear. The premium is the cost of protecting the other 99%.

The Core-and-Satellite Strategy for High Earners

One approach worth knowing about — and one that independent brokers recommend consistently — is the core-and-satellite model.

The “core” is your employer group plan. Keep it. It’s typically low-cost or employer-subsidized, and it provides a baseline of coverage even with the 24-month definition switch. Take it.

The “satellite” is an individual true own-occupation policy that you own personally. This policy doesn’t depend on your employer. It doesn’t change definitions at month 25. It travels with you if you change jobs. And because it’s paid with after-tax dollars, the benefits arrive tax-free — which matters significantly at high income levels where a taxable group benefit can lose 30%–35% of its value to federal and state taxes.

The two together — group coverage as the base, individual own-occ as the protection layer — produce a combined benefit that’s both adequate and actually reliable when tested.

For residents and fellows early in a career: add a Future Increase Option rider. This lets you expand coverage as your income grows without new medical underwriting. Lock it in while you’re young and healthy. That optionality becomes more valuable, not less, as the years pass.

The Best Own-Occupation Disability Insurance Companies in 2026

Carriers consistently recommended by independent brokers for true own-occupation and specialty own-occupation language include Guardian, Principal, and Ameritas. These names come up not because they’re cheapest — they’re not always — but because their policy definitions hold up when claims actually get filed and tested.

Work with an independent broker, not a captive agent. A captive agent can only offer one carrier’s products. An independent broker can lay three contracts side by side and compare the definition sections, the residual riders, and the specialty language. That comparison is where the real value lives.

Don’t compare premiums across policies without first comparing definitions. A cheaper policy with any-occupation language isn’t a bargain. It’s a policy that may not pay.

Protecting Your Claim If You Already Have Group Coverage

If you currently have only a group plan and can’t immediately add individual coverage, here’s what to do in the meantime.

Document functional limitations, not just diagnoses. Insurers often concede a diagnosis while denying the resulting disability. Your medical records need to document specific, concrete limitations: sitting tolerance, cognitive reliability over an eight-hour day, fine motor skill capacity, physical stamina for the duties your job actually requires. Vague notes saying “patient has condition X” don’t build a claim. Specific documented observations do.

Request a human reviewer if you receive an AI-generated denial. California and Colorado now require licensed human clinicians to review AI-driven denials. Other states are moving in this direction. But you have to ask.

Mark month 24 on your calendar if you’re currently on claim. Treat it as a deadline. The definition shift is coming. You need to know your options before it hits — not after.

People Also Ask – PAA’s

What is the main difference between own occupation vs any occupation disability insurance?

Own occupation pays benefits if you can’t perform your specific job, even if you work somewhere else. Any occupation only pays if you can’t perform any job you’re reasonably qualified for. For specialists, the difference can be the entire benefit — own-occ pays; any-occ finds a workaround.

What is the definition of total disability under these standards?

Under own-occupation, total disability means you can’t perform the material duties of your specific profession. Under any-occupation, total disability means you can’t work in any capacity your education and training could support. The any-occupation bar is significantly harder to clear.

Why do surgeons specifically need own-occupation disability insurance?

A surgeon who loses the ability to operate has lost the core value of years of specialized training. Any-occupation coverage can reclassify a surgeon as any other type of physician — or any medical professional at all — and deny benefits on the grounds that she can still do something medical. Own-occupation protects the specialty itself, not just the broad career category.

What are the best own-occupation disability insurance companies in 2026?

Independent brokers consistently point to Guardian, Principal, and Ameritas for strong own-occupation and specialty own-occupation contract language. The right choice depends on specialty, age, health history, and benefit amount — all things an independent broker can compare across carriers simultaneously.

What is specialty own-occupation coverage?

It’s a refinement of true own-occupation that protects a professional’s specific clinical specialty rather than their general occupation category. A pediatric cardiologist with specialty own-occ coverage can’t be told to just do general medicine. The benefit is tied to the specialty she actually trained for.

What is the 24-month trap in group LTD policies?

Most employer group plans use own-occupation language for the first 24 months, then automatically switch to any-occupation. Month 25 is when most group-plan benefit terminations happen — the insurer now applies the stricter standard and argues the claimant can do some other type of work.

Is specialty own occupation coverage worth the higher premium?

For high-skill specialists whose income is directly tied to what their hands, voice, or specific cognitive capacities can do — yes, without much debate. The premium for specialty own-occ reflects the real cost of protecting a specialized skill set. The alternative is paying for coverage that fails exactly when you need it.

What Happened to Dana

She appealed. Twice. The second appeal went through with the help of a disability attorney who documented her specific functional limitations — not just the diagnosis, but exactly what those limitations prevented her from doing in a courtroom context.

She won the appeal. Benefits reinstated.

It took 14 months. She spent savings she hadn’t planned to touch. She lost clients she couldn’t maintain contact with during the fight. The policy eventually paid, but only after a process that almost no one has the stamina or resources to survive without help.

She’s now fully insured under an individual true own-occupation policy with specialty language specific to litigation practice. Paid with after-tax dollars. Tax-free benefits. A benefit period to 65.

The group plan is still there. She kept it. It’s the core.

The individual own-occ policy is the satellite — the part that actually protects what she spent twelve years building.

Own occupation vs any occupation isn’t a technical distinction. It’s the difference between a policy that works and one that finds a reason not to. For anyone whose income depends on a specific set of trained skills, there’s really only one definition worth having.

If you’ve confirmed your policy uses true own-occupation language, the next step is evaluating whether the right riders are attached. See our breakdown of disability insurance riders for physicians for what’s worth adding.

About the Author

James Whitfield covers personal finance, insurance policy, and income protection strategies for U.S. professionals. He has analyzed disability contracts across more than a dozen carriers and written about claims adjudication, ERISA law, and professional coverage gaps for eight years. He holds no insurance licenses and does not sell products.

This article is for informational purposes only. It is not financial, legal, or insurance advice. Policy terms vary by carrier, state, and individual underwriting. Speak with a licensed independent insurance professional before making coverage decisions. Figures reflect 2026 publicly available market and government data.