My neighbor called me on a Wednesday afternoon, three weeks into her disability leave.

She wasn’t calling to talk about her back surgery. She was calling because the first check from her employer’s long-term disability plan had just hit her account. She’d expected $3,900. She got $2,480.

“Did they make a mistake?” she asked.

They didn’t.

Her company had been paying those insurance premiums for years. Every dollar. Never included it in her paycheck. And because of that — the IRS treated her disability benefits like salary. Full tax. No exceptions.

Are disability insurance benefits taxable?

Nobody told her. Not HR. Not the benefits brochure. Not the enrollment confirmation email. She found out the same way a lot of people do. By checking her bank account on a Wednesday and doing the math.

That’s the thing about disability insurance taxes. The rule is simple. The consequences are not.

Understanding benefit taxability is one piece of a larger picture. For a full overview of how disability policies work — and what determines whether a claim gets paid at all — see our 2026 disability insurance guide.

One Sentence Tells You Everything You Need to Know

Ready? Here it is.

How the premium was paid is how the benefit gets taxed.

That’s it. If your employer paid the premiums — and never added that cost to your taxable wages — your benefits are taxable income. The IRS sees them as a delayed paycheck. You owe federal tax on every dollar you receive.

If you paid the premiums yourself — with money already taxed — benefits come out clean. Tax-free. You’ve already paid your dues.

That’s the rule. Pre-tax dollars in, taxable dollars out. After-tax dollars in, tax-free dollars out.

Sound simple? It is. The problem is that most employees have no idea which side of that line they’re on. They enrolled in benefits during a 20-minute orientation three years ago and moved on. Nobody circled the part about tax consequences of employer-paid disability insurance on the handout. Nobody explained what would happen if they ever needed to actually use it.

The group vs. individual plan distinction is the single biggest factor in how your benefits get taxed. For a deeper look at how the two plan types compare beyond the tax angle, see our guide to individual vs group disability insurance.

What “60% Replacement” Really Means After Taxes

Here’s where it gets expensive.

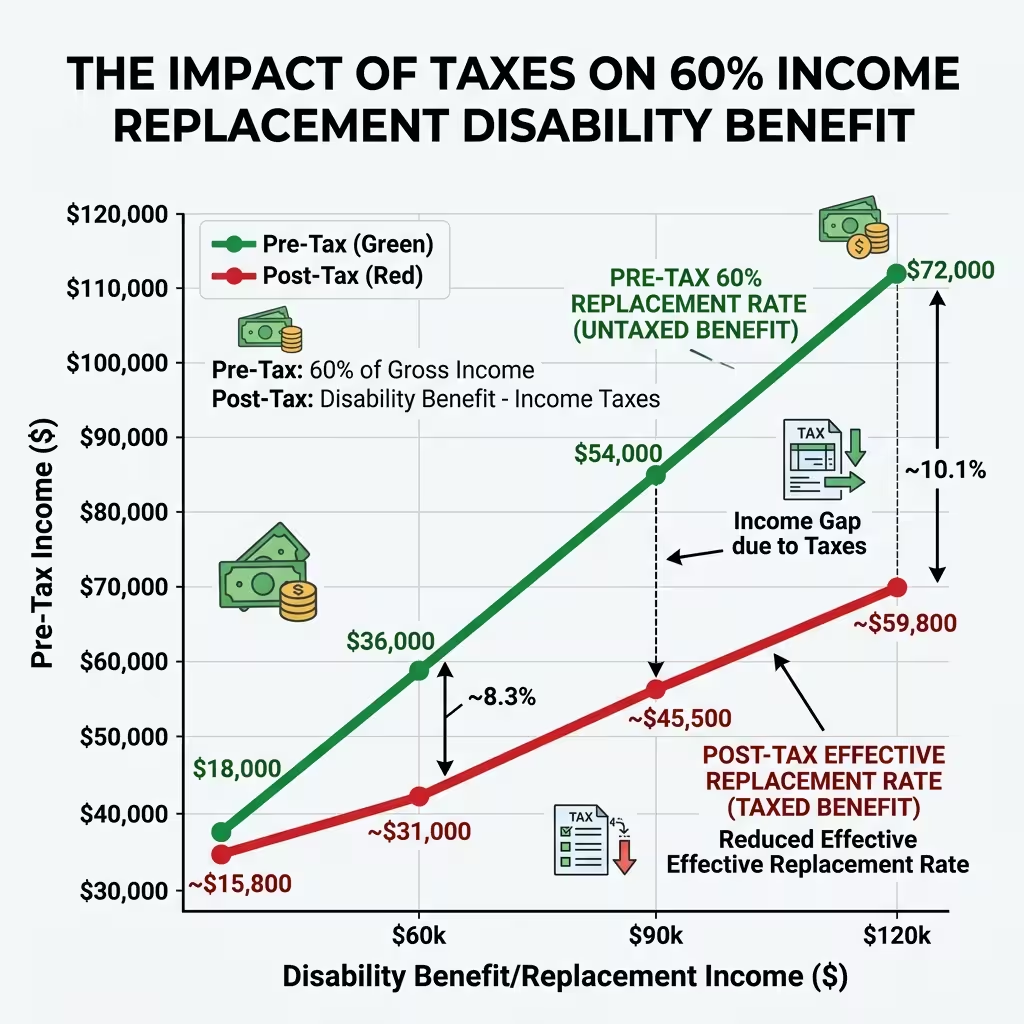

Group long-term disability plans — the kind your job provides — typically promise to replace 60% of your income. That sounds workable. It’s not the same as your full salary, but 60% gets you through, right?

Maybe. Depends on whether the IRS takes a cut.

Take a project manager earning $110,000 a year. Her group LTD plan kicks in. She starts collecting 60% — about $5,500 a month. But her employer paid those premiums. So the IRS counts those benefits as ordinary income.

She’s in a 38% combined federal and state tax bracket. After taxes, $5,500 becomes roughly $3,400.

That’s not 60% replacement. That’s 37%.

For someone whose mortgage, car payment, and bills were built around $110,000 a year — $3,400 a month is a real crisis. Not a tight month. A crisis.

Financial planners have a name for this. They call it the executive income gap. The distance between what a group plan promises on paper and what actually lands in your account after the IRS is finished.

I think that name’s too polite. It’s a trap. One most people don’t discover until they’re already in it.

The Simple Fix Most Employees Never Do

You can avoid this entirely. Most people just don’t know to ask.

Many employers offer a choice during open enrollment. You can pay your share of the group LTD premium with pre-tax dollars or after-tax dollars. Pre-tax lowers your take-home slightly each paycheck. After-tax lowers it a bit more.

The difference feels small every two weeks.

It’s massive if you ever file a claim.

If you’ve been paying your share after-tax, your portion of any benefit you receive is tax-free. The math flips in your favor. You gave up $8 or $12 per paycheck and protected yourself from owing taxes on months of disability income.

Ask HR which option you’re currently enrolled in. Ask today. Most employees have never thought to ask, and most HR departments won’t bring it up unless you do.

If your company pays 100% of the premium — you don’t have a choice to make. But you still have a move. Ask whether you can elect to have the premium value added to your gross wages. That treats it like taxable income now, and your future benefits become tax-free. Some employers allow it. Many don’t know anyone’s ever asked.

If your benefits will be taxable, your gross benefit amount needs to be higher to maintain the same net income replacement. Use our disability insurance coverage guide to recalculate your target with taxes factored in.

When You Buy Your Own Policy: The Clean Version

This one’s straightforward.

Buy your own individual disability insurance policy. Pay the premiums yourself, out of pocket, with after-tax dollars. When you collect benefits — tax-free. Full stop.

No employer involved. No IRS claiming it’s ordinary income. The money lands and stays.

You can’t deduct the premiums on your tax return. That’s the trade-off. But when you actually need the coverage — when you’re out for months and watching your account balance — you’ll get the number the policy promised. Not 60% minus taxes. Just 60%.

For self-employed workers, independent contractors, and freelancers billing on 1099s — this is the only real option anyway. There’s no employer group plan. They build their own safety net. They pay their own premiums. And IRS Section 104 — the provision that excludes personally paid disability benefits from gross income — protects the payout.

It’s the one time the tax code actually works cleanly in your favor.

The Split-Premium Mess

What if your employer pays part and you pay part?

That’s common. Lots of companies cover a base benefit and let employees buy supplemental coverage through payroll deductions. The trouble is that the tax treatment of your benefit depends on the exact split.

Say 65% of your total premiums came from your employer — pre-tax. You paid the other 35% through after-tax deductions. When you file a claim, 65% of your monthly benefit is taxable. The other 35% isn’t.

Every claim, your insurer has to calculate that ratio.

And here’s the wrinkle nobody talks about. The Three-Year Look-Back Rule.

High-income professionals — especially physicians — have the most to gain from structuring premiums correctly for tax-free benefits. See how this fits into broader coverage strategy in our disability insurance guide for physicians.

If the funding mix on your policy changed — your employer restructured benefits, or you changed how much you were contributing — insurers don’t just use the current split. They look back at the last three full policy years before your claim. They calculate the average ratio of pre-tax premiums to total premiums across that whole period. That average becomes your taxable percentage going forward.

Most people find this out when the insurer sends them an unexpected tax document. There’s nothing to fix at that point. You either knew going in, or you didn’t.

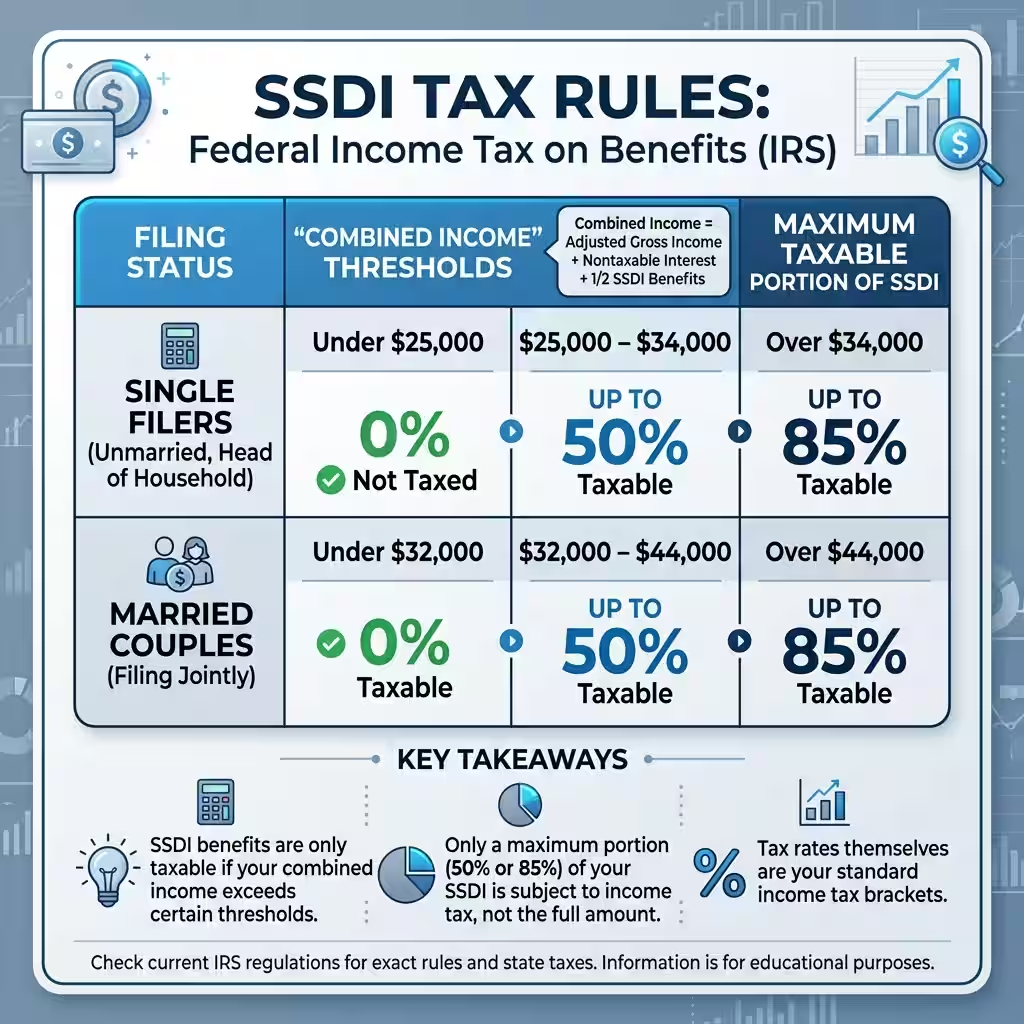

SSDI Tax Rules: Different Animal Entirely

Social Security Disability Insurance doesn’t follow the same pre-tax/after-tax rule. It has its own formula.

SSDI benefits aren’t automatically taxed. Whether you owe anything depends on something called provisional income. The IRS calculates it like this: take your adjusted gross income, add any tax-exempt interest you earned, then add half of your annual SSDI benefits. That total is your provisional income.

For single filers in 2026:

- $25,000 to $34,000 — up to 50% of your SSDI may be taxable

- Above $34,000 — up to 85% may be taxable

For married couples filing jointly:

- $32,000 to $44,000 — up to 50% taxable

- Above $44,000 — up to 85% taxable

Here’s what frustrates me about these numbers. Congress set those thresholds in 1984. They’ve never been adjusted for inflation. A retired person with a modest investment account, a small pension, and SSDI benefits can easily blow past $34,000 today — even on a fixed income that would have been considered working-class in 1984.

The 2026 COLA bump was 2.8%. Average benefits went up slightly. But Medicare Part B premiums also jumped — to $202.90 a month, pulled directly from Social Security checks before they arrive. After netting everything, the typical SSDI recipient gained about $26.10 a month in real terms. Not nothing. Not much either.

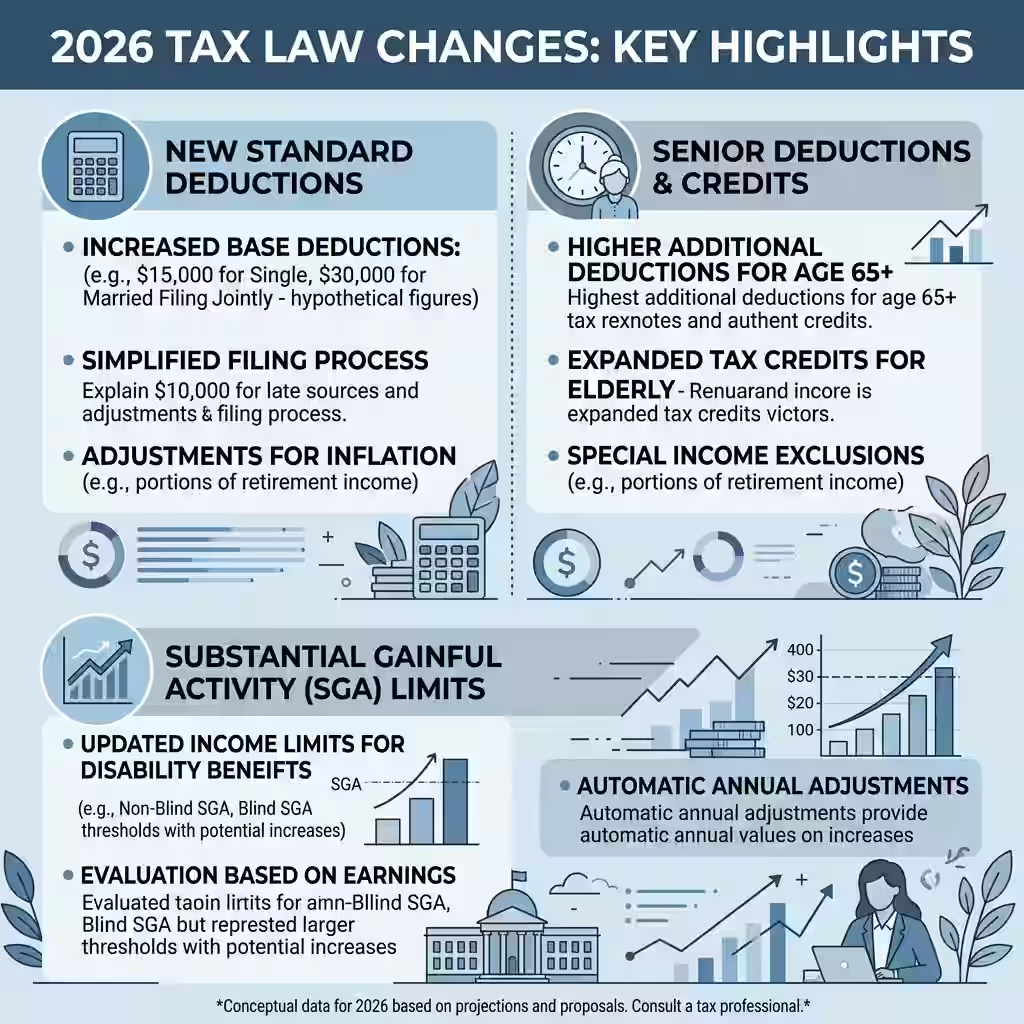

What the 2026 Tax Law Changed

The One Big Beautiful Bill Act — signed July 4, 2025 — made real changes to the standard deduction and added a few new ones.

Standard deductions for 2026: $16,100 for single filers. $32,200 for married couples filing jointly. $24,150 for heads of household. These are now permanent. They won’t sunset in a few years the way previous provisions did. That stability matters for planning.

The Senior Deduction is worth knowing if you’re 65 or older.

The OBBBA gives taxpayers 65 and up an extra $6,000 deduction — $12,000 for couples. This runs through 2028. It phases out at $75,000 MAGI for individuals and $150,000 for joint filers. Fully gone at $175,000 for individuals.

Practical effect: around 88% to 90% of seniors won’t owe federal tax on their Social Security benefits during this window. If you’re collecting SSDI and you’re 65 or over — run the math. Depending on your other income, this deduction might eliminate your tax bill on those benefits entirely.

The Substantial Gainful Activity limit also increased. In 2026, non-blind SSDI recipients can earn up to $1,690 a month without triggering a review of their eligibility. For blind recipients, the threshold is $2,830. The Trial Work Period threshold sits at $1,210 a month — meaning you can test returning to part-time work for nine months without losing benefits automatically.

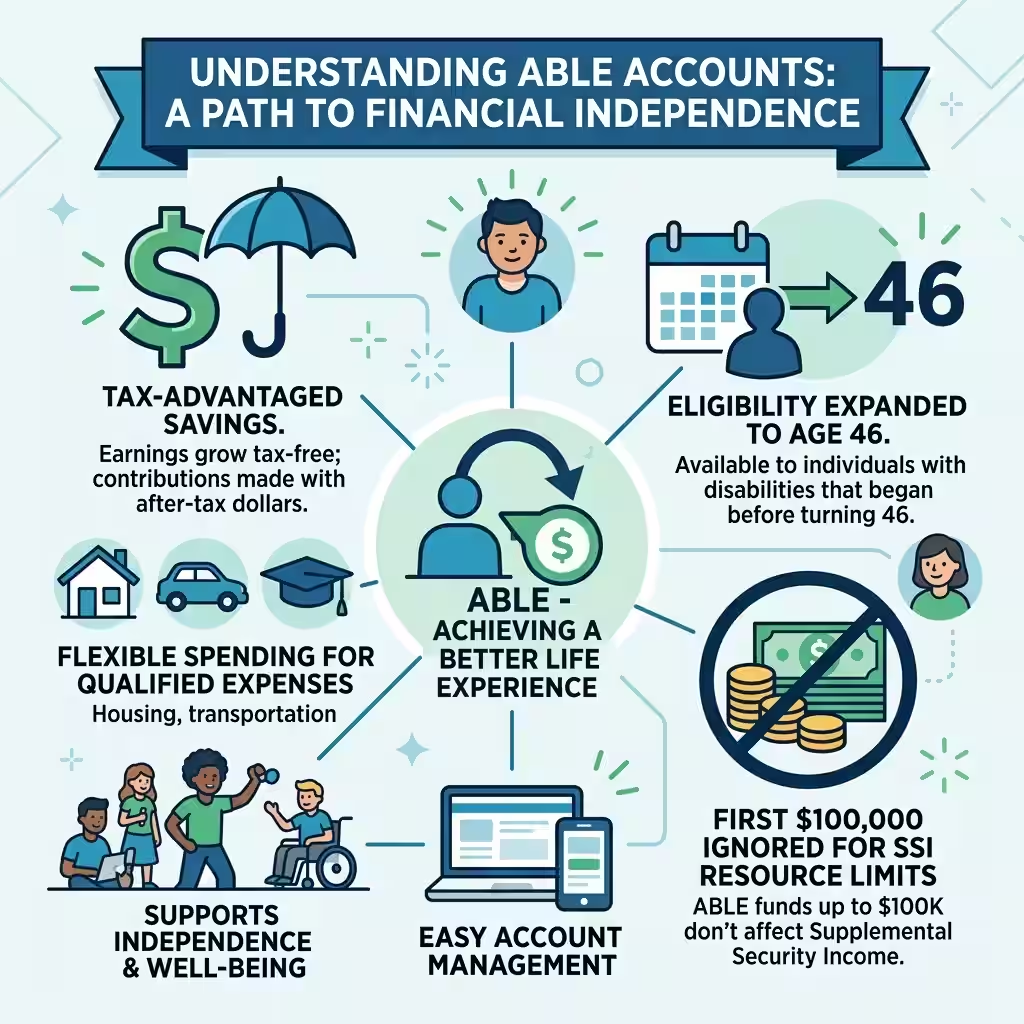

ABLE Accounts Deserve More Attention Than They Get

Honest opinion: ABLE accounts are one of the most useful tools in disability financial planning, and they barely come up in most conversations.

Here’s what they are. ABLE accounts are tax-advantaged savings vehicles for people with disabilities. Contributions go in after-tax. Money grows tax-deferred inside the account. Withdrawals spent on qualified disability expenses — housing, transportation, health care, education, assistive technology — come out completely tax-free.

Starting January 1, 2026, the eligibility window expanded. Previously, you had to have a disability with onset before age 26. Now the cutoff is 46. That change opens access to millions of people — mid-career professionals who got a diagnosis in their 30s or 40s, veterans, anyone whose disability didn’t show up in childhood. The annual contribution limit in 2026 is $20,000.

The piece that matters most for people on SSI: the first $100,000 in an ABLE account is ignored for SSI resource limits. You can save without losing your SSI benefits. Medicaid eligibility isn’t impacted either.

For a disabled worker trying to build a financial cushion without being punished for it — this tool is exactly what it looks like. Use it.

Business Owners: Different Rules Apply to You

Quick note for anyone running their own business.

Business Overhead Expense insurance — BOE — covers your operating costs if you can’t work. Rent, utilities, employee wages, software subscriptions. Premiums for BOE coverage are generally tax-deductible as a business expense. The benefits you receive are taxable — but they’re paying for deductible expenses, so it usually nets out reasonably.

Disability Buyout insurance — used when a business partner becomes disabled — works differently. Premiums aren’t deductible. But the benefits are typically tax-free. Same logic as a personally paid individual policy.

Key Person disability insurance follows the same pattern. The company pays non-deductible premiums. If a critical employee goes out, the business receives tax-free benefits.

None of these are complicated once you know which bucket they’re in. The confusion usually comes from trying to apply personal policy rules to business policies without checking.

People Also Ask – PPA’s

Are disability insurance benefits taxable?

Depends entirely on who paid the premiums. Employer-paid group premiums — benefits are taxed as ordinary income. Personally paid after-tax premiums — benefits are tax-free. Mixed funding — benefits are taxed proportionally based on the pre-tax/after-tax split.

What are the tax consequences of employer-paid disability insurance?

Every dollar of benefit is taxable ordinary income. For a professional in a 38–40% combined tax bracket, a “60% replacement” group plan delivers roughly 36–37% effective replacement after taxes. That gap can be thousands of dollars a month in a real claim situation.

How do I receive tax-free disability benefits?

Two main ways. Buy your own individual policy with after-tax dollars. Or — if your employer offers a choice — elect to pay your group LTD share through after-tax payroll deductions. Either route means your benefits arrive without a federal tax bill attached.

What does pre-tax vs. post-tax mean for premiums?

Pre-tax: the money used for premiums hadn’t been taxed yet. IRS taxes your benefits later. Post-tax: the premium dollars were already taxed before they left your paycheck. No second tax when benefits arrive.

What is the Three-Year Look-Back Rule?

When a group plan’s funding mix changed over time, insurers calculate your taxable benefit percentage using the average ratio of pre-tax premiums to total premiums over the three policy years before your claim. That average sets what portion of your benefit is taxable going forward.

What is IRS Section 104? It’s the tax code provision that excludes disability payments from gross income — but only when the benefits come from personally paid after-tax premiums. It’s the legal reason individually owned disability policies produce tax-free benefits.

Does the 2026 Senior Deduction affect SSDI recipients?

Yes — for anyone 65 or older. The OBBBA’s $6,000 additional deduction (through 2028) can effectively remove federal tax on SSDI benefits for most seniors, depending on total income. Couples get $12,000.

My neighbor didn’t switch policies immediately.

She spent another two months working through her claim, adjusting her budget, and being quietly angry that nobody had flagged this before. When she went back to work, she called her HR department and asked a single question: “Can I pay my LTD premium after-tax instead?”

Yes. She could.

She’d been paying it pre-tax for six years and never knew the option existed.

Now she pays $14 more per month. The after-tax difference is $14. If she ever files another claim — the entire benefit is tax-free. Six years of $14 choices she didn’t know she was making.

That’s the story behind disability insurance taxation. It’s not about complicated IRS formulas. It’s about a small election most employees never make because nobody explains what’s at stake until the check comes in short.

Check how your premiums are funded. Ask HR what options you have. And if you’re buying your own coverage — pay after-tax and never think about it again.

About the Author Selene Voss is a financial writer with nine years focused on tax strategy, disability income planning, and employee benefits for working professionals and self-employed individuals. Before writing full-time, they spent five years as a licensed insurance professional helping clients untangle benefit elections they’d made without understanding the long-term tax consequences.

Disclaimer: This article is for informational purposes only. It does not constitute tax, legal, or financial advice. Tax treatment of disability benefits varies by individual circumstances, state law, and filing status. Talk to a licensed CPA or tax advisor before making any benefit election decisions.