Last Updated: May 2026

Disclosure: This post is for general education. Some links may earn a referral fee. Work with a licensed professional before buying any policy.

I want to tell you about a surgeon I know. Call him Marcus. Orthopedic guy, two years out of fellowship, absolute grinder. Broke his right hand on a mountain bike trail in Colorado — of all things — and suddenly found himself staring at eighteen months of recovery and a stack of insurance paperwork he’d never actually read.

He had disability coverage. His hospital set it up automatically. He signed where HR told him to sign and moved on with his life, like most of us do.

What Marcus didn’t know — and what nobody told him at orientation — was that his plan only paid if he couldn’t work in any job his education qualified him for. Not just surgery. Any job. The insurance company’s position was that a surgeon who can’t operate can still review charts, take phone consultations, do administrative work. So technically, under their policy language, Marcus wasn’t “totally disabled.” He spent nine months fighting for a partial benefit that was smaller than he expected and harder to get than it ever should have been.

I think about his story whenever someone asks me whether disability insurance for physicians is actually worth the premium. The answer is yes — but only if you buy the right kind. And most physicians, dentists, and specialists don’t have the right kind. They have whatever their employer handed them.

Before diving into the physician-specific considerations, our 2026 disability insurance guide covers the policy fundamentals every professional should understand — including the definition language that determines whether a claim gets paid.

The Definition That Makes or Breaks Everything

Here’s what I want you to understand before anything else: the monthly benefit amount on your policy is almost irrelevant if the definition of “disability” inside it doesn’t work in your favor. That definition is the one sentence — sometimes buried on page twelve — that determines whether your claim gets paid or disputed.

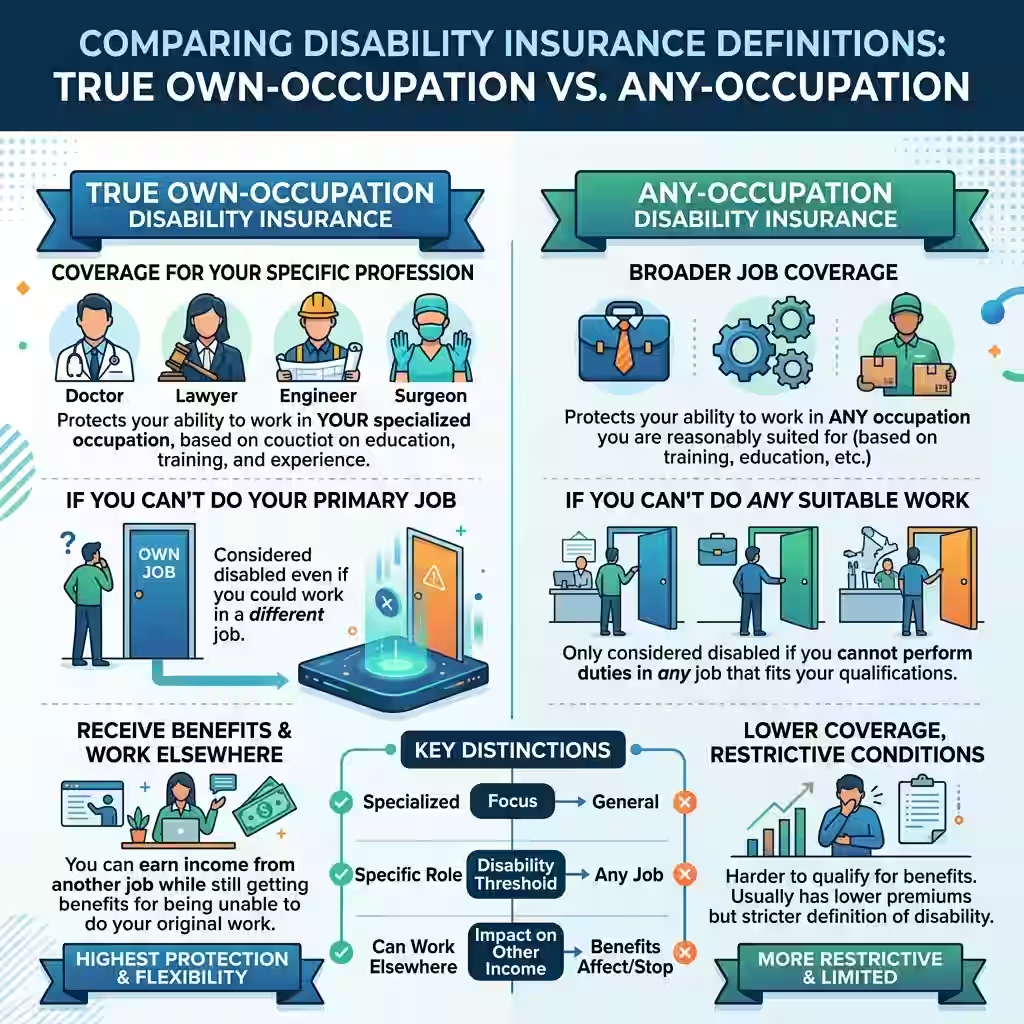

There’s a version called true own-occupation, and it’s what every physician and dentist should have. Under this definition, you’re considered disabled if you can no longer do the work of your specific specialty. A hand surgeon who loses fine motor control is disabled, full stop, even if she’s perfectly capable of giving grand rounds lectures or reviewing pathology reports. The policy pays. No argument.

For physicians, the disability definition isn’t a technicality — it’s the entire policy. Our dedicated breakdown of own-occupation vs any-occupation insurance shows exactly how these definitions play out when a specialist can no longer practice.

The problem is that most employer group plans don’t use that language. They use something called any-occupation, which only kicks in when you literally cannot work in any field your training qualifies you for. That’s the definition that gave Marcus’s insurer room to maneuver. And it’s the definition that makes dental specialty disability insurance and medical own-occupation coverage almost worthless for anyone who spent a decade training to do something specific.

Physicians who pay their own premiums on an individual policy receive tax-free benefits. Those covered under employer-paid group plans may not. See are disability insurance benefits taxable for how this affects your net payout.

There’s a middle version too — modified own-occupation — that looks better on paper but falls apart in practice. Under that one, the moment you take any other job, your benefits stop. A neurosurgeon who picks up part-time consulting after a spinal injury loses the entire benefit. It’s a trap written in plain language.

Some carriers go further than the standard definitions. Guardian Life, for one, offers what they call an Enhanced Medical Specialty definition where a physician is considered totally disabled if they lose more than fifty percent of their income because they can no longer do hands-on clinical or surgical work — even while continuing some other duties. For anyone who operates, scopes, anesthetizes, or does any kind of procedural work, that extra layer of language is worth every dollar of additional premium.

Why the Group Plan Your Hospital Gave You Probably Has Holes in It

I’m not going to tell you your group plan is worthless. It isn’t. But for most specialists, it’s covering maybe a third of the exposure that actually needs covering, and that’s before the tax problem.

Start with the benefit cap. Most hospital group plans max out somewhere around ten thousand dollars a month. That sounds like real money until you run the numbers. A physician earning three hundred and fifty thousand dollars a year is grossing close to twenty-nine thousand a month. Ten thousand covers about a third of that. The rest of your financial life — mortgage, kids in school, your own student loans, retirement contributions — keeps running on savings that drain faster than you’d expect.

Then there’s the tax issue, and this one genuinely surprises people. When your employer pays your disability premiums — which is exactly how group plans work — the IRS treats your benefit as ordinary income. That ten-thousand-dollar monthly check gets taxed. At a thirty-five percent marginal rate, you’re taking home around sixty-five hundred dollars. The plan that looked like a hundred and twenty thousand dollars a year in protection is actually seventy-eight thousand in your pocket. The longer you’re on claim, the more that gap matters.

Many physicians assume their hospital or group practice plan is adequate. It usually isn’t. Our comparison of individual vs group disability insurance shows exactly where employer plans fall short for high-income specialists.

The fix is buying your own individual policy and paying the premiums yourself with after-tax money. Benefits from those policies come out completely tax-free. Not partially. Completely. But you have to set it up before something happens, not after.

And then there’s the language problem, which is really what sank Marcus. Group plans use broad occupational categories. A CRNA gets filed as a registered nurse or a healthcare professional, not specifically as a nurse anesthetist. So when a CRNA develops a condition that prevents them from performing anesthesia, the insurance company can argue — with a straight face, citing their own policy — that the insured could work in case management, or patient education, or outpatient triage. Claim denied.

An individual policy that specifically covers “Certified Registered Nurse Anesthetist” doesn’t give them that out. The specialty language closes the argument before it starts. For any fellowship-trained specialist, any proceduralist, any dentist or oral surgeon whose income depends on doing one specific thing extremely well, that’s not a small distinction. It’s the whole ballgame.

What You’re Actually Going to Pay

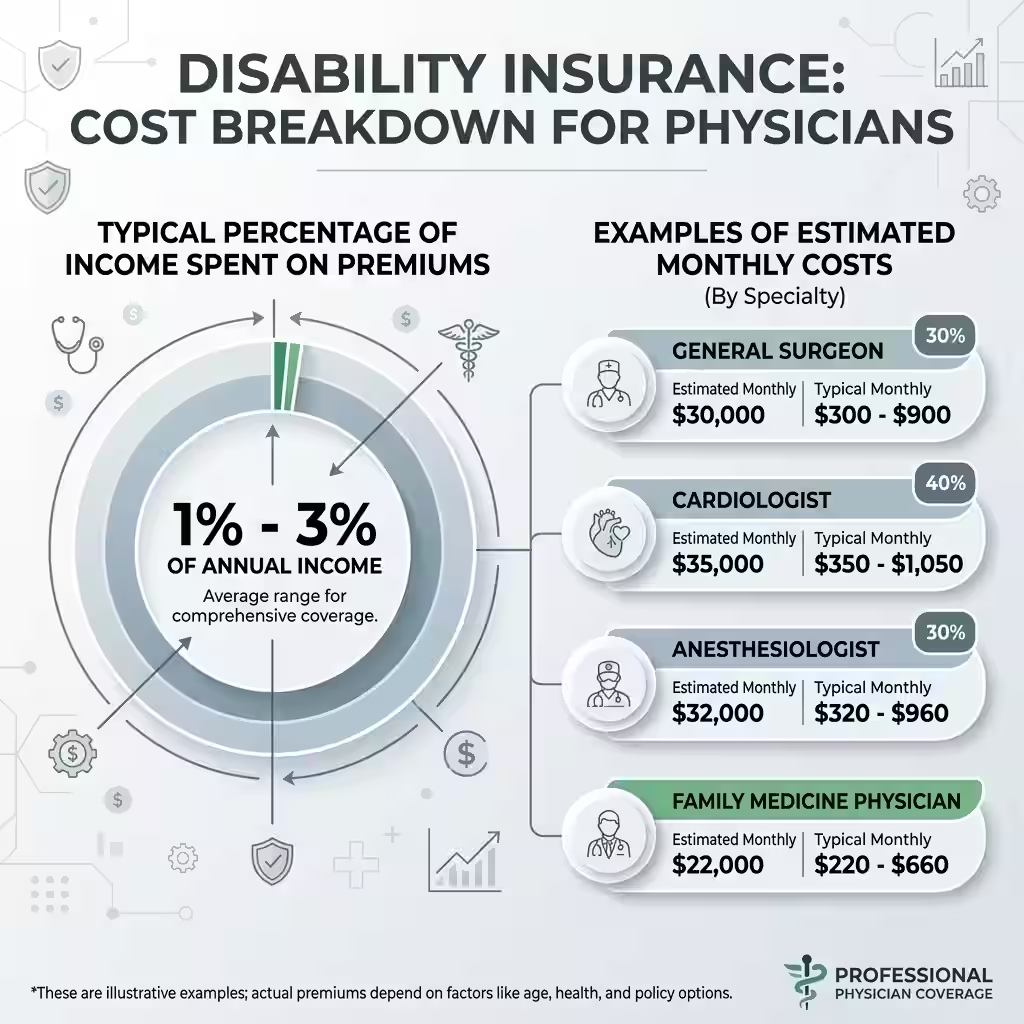

Disability insurance for physicians cost comes up in almost every conversation I have about this topic, and the honest answer is that there’s no single number — but there are real ranges.

For a solid individual policy, most physicians end up paying somewhere between one and three percent of their gross annual income in premiums. Put another way, two to six percent of the annual benefit they’re trying to protect. A thirty-year-old internal medicine doctor buying ten thousand a month in coverage through age sixty-five might pay two hundred to three fifty per month. A thirty-two-year-old orthopedic surgeon buying the same benefit could pay three fifty to five fifty, because surgical specialties carry a higher occupational risk rating with every major carrier.

That risk class thing affects cost more than most people going into the process expect. Insurers rate every specialty on a scale. Psychiatry, pathology, and administrative medicine sit at the low end. Emergency medicine, neurosurgery, and orthopedic surgery sit at the high end. That classification determines your base premium before your health history, any riders, or benefit period choices get factored in at all.

The best time to buy is during residency, and I want to be clear that this isn’t sales talk. Premiums lock at your age when you apply. The younger you are, the lower the base rate, and with a non-cancelable policy that rate holds for the entire life of the contract. You’re also getting underwritten on your health before clinical exposure has had time to create problems — before a needle stick, before the chronic back pain from standing at an operating table six days a week, before the anxiety diagnosis from sleep deprivation that shows up in your records during third year of fellowship. Those things turn into policy exclusions or outright declined applications when you apply later.

Most carriers also offer resident and fellow discounts of ten to thirty percent. Those disappear the day training ends.

One more reason to buy early: the Future Increase Option rider. It lets you increase your monthly benefit as your income grows, without any new health questions. A resident who locks in five thousand a month with that rider can eventually bump coverage to fifteen thousand a month as an attending, no underwriting required. Wait until you’re out of training with some medical history on file, and that door closes permanently.

The Five Carriers Worth Knowing

The individual, non-cancelable, own-occupation disability market is mostly controlled by five major players. Every specialist should know them.

Guardian is the strongest option for proceduralists. Their Enhanced Medical Specialty definition is the most physician-favorable language on the market, and their mental health coverage is notably better than most competitors — no arbitrary twenty-four month cap on psychiatric or behavioral claims. That matters more than it sounds because mental health conditions represent a significant and growing share of long-term disability claims.

Principal is often the best fit for female physicians. They offer gender-neutral pricing, which removes a premium gap that traditional gender-distinct rating systems create for female doctors. Strong resident discounts and flexibility in how they handle transitional work make them a frequent winner in side-by-side comparisons.

Ameritas has two features that set them apart. Their Good Health benefit shortens the elimination period after you’ve gone a stretch without a claim — meaning faster payment when you need it. They also cover COBRA premiums during a disability, which solves a real problem during any gap in employer-based coverage.

MassMutual’s Radius Choice contract includes both presumptive total disability coverage and a recurring disability benefit. The recurring benefit is the interesting one — if the same condition flares up after you’ve returned to work, they waive the elimination period. For anything chronic or episodic, that’s a real financial difference.

The Standard rounds out the group. Their Platinum Advantage policy is built to move with you — portable across hospital employment, private practice, locum tenens, and independent work. It also tends to price more competitively for certain specialties than the bigger names on the list.

Practical note: always get quotes from at least three of these. Which carrier prices you best depends entirely on your specific age, specialty, and health history. Any broker who tells you there’s a universal winner before running your numbers is guessing.

The Riders That Change What You Actually Collect

Adding the right riders to a base policy is the difference between coverage that fits your life and coverage that leaves gaps exactly where you’re most likely to need it.

The residual or partial disability rider is the one people most regret skipping. It pays a proportional benefit when you’re back at work but still earning less than before because of a partial disability. A surgeon returning at sixty percent capacity collects forty percent of the full monthly benefit. Without this rider, partial claims typically pay nothing at all, and most real-world return-to-work situations involve some kind of transitional period before you’re fully functional.

The COLA rider — cost of living adjustment — grows your benefit during a claim, typically around three percent per year. Ten thousand a month in year one becomes over thirteen thousand in year ten. Inflation doesn’t pause because you’re on a disability claim, and physicians who’ve been on long-term claims without this rider watch their purchasing power shrink year over year.

Once the right base policy is in place, riders are where physician coverage gets fine-tuned. Our full guide to disability insurance riders for physicians covers the six most important add-ons — including future increhospase options and residual disability riders.

The student loan rider covers up to around twenty-five hundred a month specifically for student loan payments, separate from the income benefit. It doesn’t reduce your monthly living expense protection. For anyone still carrying medical or dental school debt, worth pricing out.

And make sure every policy has both non-cancelable and guaranteed renewable provisions. Non-cancelable locks your premium. Guaranteed renewable locks the contract terms and definitions. Together, they mean the insurer can’t change what they promised you as long as you keep paying on time. If a policy you’re considering doesn’t have both, keep shopping.

People Also Ask – PAA’s

Is disability insurance worth it for physicians?

Yes. About one in four workers experiences a disability before retirement, and physicians face occupational risks — repetitive strain, bloodborne pathogen exposure, burnout, physical demands from procedural work — that concentrate that exposure in certain specialties more than others. No investment account replaces specialty income if you can’t practice. The question isn’t whether it’s worth buying. It’s whether the policy you have will actually pay the way you think it will.

How much should physician disability insurance cost?

For a solid individual policy, budget somewhere between two thousand and six thousand dollars a year as an attending — roughly one to three percent of gross income. Residents pay less. Premiums rise with age and occupational risk class. An orthopedic surgeon and a psychiatrist buying identical benefit amounts won’t see the same premium.

What is the hardest disability to get approved for?

Under any-occupation definitions, mental health conditions and musculoskeletal injuries face the most pushback. Insurers argue those conditions allow for sedentary or alternative work — and under broad occupational definitions, they often get away with it. Under true own-occupation contracts, those arguments mostly fall apart because the test is your specific specialty, not some other job you could hypothetically perform.

Why do some advisors say skip short-term disability insurance?

The argument is that high-income professionals with a real cash reserve can cover a short gap themselves. A ninety-day elimination period cuts premiums significantly, and three months of living expenses is manageable for most attendings. What the same advisors agree on is that long-term own-occupation coverage is non-negotiable — because no one self-insures a five-year disability on savings.

Physician disability insurance — group vs. individual. What actually matters?

Group coverage is employer-paid, taxable at claim, benefit-capped, uses broad occupational definitions, isn’t portable, and ends when employment ends. Individual policies are owned by you, tax-free when you pay the premiums, written with specialty-specific definitions, portable across every practice setting, and locked under non-cancelable terms. For anyone whose income depends on a specific skill set, group-only coverage leaves real risk sitting uncovered.

Back to Marcus

He got his partial check eventually. Nine months later, after paperwork and phone calls and an appeal process nobody warned him about.

He bought an individual policy shortly after — true own-occupation, residual rider, non-cancelable through sixty-five. When residents rotate through his service now and ask about financial planning, he tells them the same thing every time: find the definition section before you sign anything. That one paragraph determines everything.

The coverage exists. The five carriers listed here are legitimate. The riders are available. The residency discount window is open right now for anyone still in training.

What isn’t guaranteed is that the policy sitting in your benefits portal right now — or the one you’re about to sign — actually uses language that pays when you need it most. Pull the document. Find the definition. If it isn’t specialty-specific, that’s the gap worth fixing.

For unbiased research on policy terms, the Council for Disability Awareness is a good starting point. For quotes, use an independent broker who works across all five of the carriers above — not just the one they write the most business with.

About the Author

Selene Voss covers insurance and professional income protection. He’s written about the U.S. disability market for over ten years and contributes regularly to publications focused on physician financial education. He is not a licensed insurance agent and does not sell policies.

Disclaimer: Nothing in this post is financial, legal, or insurance advice. Policy definitions, carrier availability, and premium ranges vary by state, specialty, and individual underwriting. Talk to a licensed professional before making coverage decisions. Premium figures are general market estimates only.