Last Updated: May 2026

Disclosure: This blog contains general educational information only. Some links may be affiliate links. Talk to a licensed insurance advisor before buying any policy.

Marcus didn’t think much about riders when he bought his policy.

He was a third-year internal medicine resident in Houston. Tired. Behind on everything. His advisor sent a PDF. Marcus skimmed it, signed the DocuSign, and went back to a 14-hour shift. He figured disability insurance was disability insurance. He had it. Done.

Fast forward six years. Marcus is an attending now. His income went from $64,000 to $290,000. He’s got $240,000 in private student loans — refinanced during residency when the rates looked good. He got diagnosed with Type 2 diabetes last spring. Managed, but documented.

He called to increase his coverage. The underwriter flagged his application. His base benefit, the one he’d bought in a rush? Covered about $4,800 a month. His mortgage alone is $4,200.

The policy wasn’t the problem. What he left off the policy was.

That’s the whole point of disability insurance riders. The base coverage gets you something. The riders are what make that something actually useful when your life goes sideways.

If you’re new to how disability policies are structured, our 2026 disability insurance guide is the right starting point — it covers definitions, benefit periods, and the policy mechanics that riders are built on top of.

Your Base Policy Is Just the Starting Point

Most people shopping for disability insurance spend their energy picking a carrier. The “Big 5” — Ameritas, Guardian, MassMutual, Principal, The Standard — dominate this market for one reason. All five offer what’s called True Own-Occupation coverage. That means if you can’t do your specific job anymore, you get paid. A hand surgeon who loses grip strength collects full benefits even while teaching at a med school. That distinction matters enormously.

A rider on a policy with any-occupation language won’t protect a specialist’s income the way it should. Make sure your base policy uses true own-occupation coverage — our comparison of own-occupation vs any-occupation definitions explains what to look for.

But here’s what most people miss.

The base policy covers the catastrophic, worst-case scenario. You’re completely out. Can’t work at all. Benefits kick in after your elimination period and run until 65.

Real life is messier than that.

Most disability claims aren’t total. They’re partial. A shoulder surgery that keeps a surgeon off the OR table for eight months. A mental health episode that has a hospitalist working half-days. A neurological condition that starts slow and gets worse over years. In every one of those situations, a stripped-down base policy either pays nothing or pays far less than it should.

That’s the gap. Riders fill it.

Not all of them. You don’t need every rider ever invented. But there are six that make a real difference — and knowing which ones apply to your situation could be worth hundreds of thousands of dollars.

1. Future Purchase Option — Buy Your Insurability Now

If you’re a resident or fellow right now, you should read this section twice.

The future purchase option — some carriers call it the Future Increase Option (FIO) or the Benefit Update rider — lets you buy more coverage later without new medical underwriting. No exam. No new health history. No one asking about that arrhythmia your cardiologist is monitoring.

Why does that matter so much?

Because you don’t know what your health looks like in five years. Most residents are healthy. But residency is brutal. Things happen. A back injury from standing 12-hour shifts. A mental health diagnosis. High blood pressure that shows up at 34. Once any of that is on your medical record, getting new coverage — or increasing existing coverage — gets a lot harder. Sometimes impossible.

With the future purchase option locked in during training, you keep the right to buy more coverage as your income grows. No questions asked.

Before adding a future increase option, it’s worth confirming your current benefit amount is sized correctly. Our guide to calculating how much disability insurance you need walks through the right formula for high-income professionals.

Residents can usually qualify for around $5,000 a month in coverage. That’s appropriate for a $65,000 salary. But the same person making $320,000 as an attending needs $15,000 to $20,000 a month or more. The FPO is the bridge between those two numbers.

Principal offers a Benefit Update rider that reopens every three years. Guardian and MassMutual have similar structures. The specific rules vary — ask your broker to walk through the option windows — but the underlying point is the same across all of them. You’re buying your future insurability today, at today’s health status, before life gets complicated.

I’d argue this is the single most undervalued rider on the market for anyone still in training. Not because it pays a benefit today. Because it protects the ability to get covered tomorrow.

2. Residual Disability Benefit — The Rider for What Actually Happens

Here’s a question worth sitting with: what does a disability actually look like?

Most people picture total incapacitation. Unable to get out of bed. The dramatic scenario. And yes, that happens. But statistically, it’s not the most common story.

More often it looks like a gastroenterologist with Crohn’s disease who can see patients but can’t do procedures anymore. A psychiatrist dealing with a depressive episode who drops from 40 patients a week to 18. An OB who develops a repetitive stress injury and has to cut deliveries by half. Each of these physicians is still working. Still contributing. Still showing up.

Riders only make sense on a solid policy foundation. If you haven’t reviewed your base coverage yet, start with our guide to disability insurance for physicians before evaluating add-ons.

And under a base-only policy? Many of them would collect nothing.

That’s exactly what the residual disability benefit is designed to fix. If your income drops by 15 to 20 percent or more because of an illness or injury — but you’re still working in some capacity — this rider pays proportionately. Income drops 50 percent, rider covers roughly 50 percent of your monthly benefit.

Guardian’s version triggers at just 15% income loss. That’s one of the lowest thresholds you’ll find anywhere. Some carriers also bundle in what’s called a Recovery Benefit, which keeps the partial payments coming even after you return to full-time work — until your income actually climbs back to where it was before the disability. That runway matters more than people think, especially in private practice where rebuilding a patient panel takes time.

Skipping this rider is one of the most common mistakes I see. And it usually happens because people are trying to save on premium. The irony is that by cutting the residual benefit, they’re removing protection for the exact scenario they’re most likely to face.

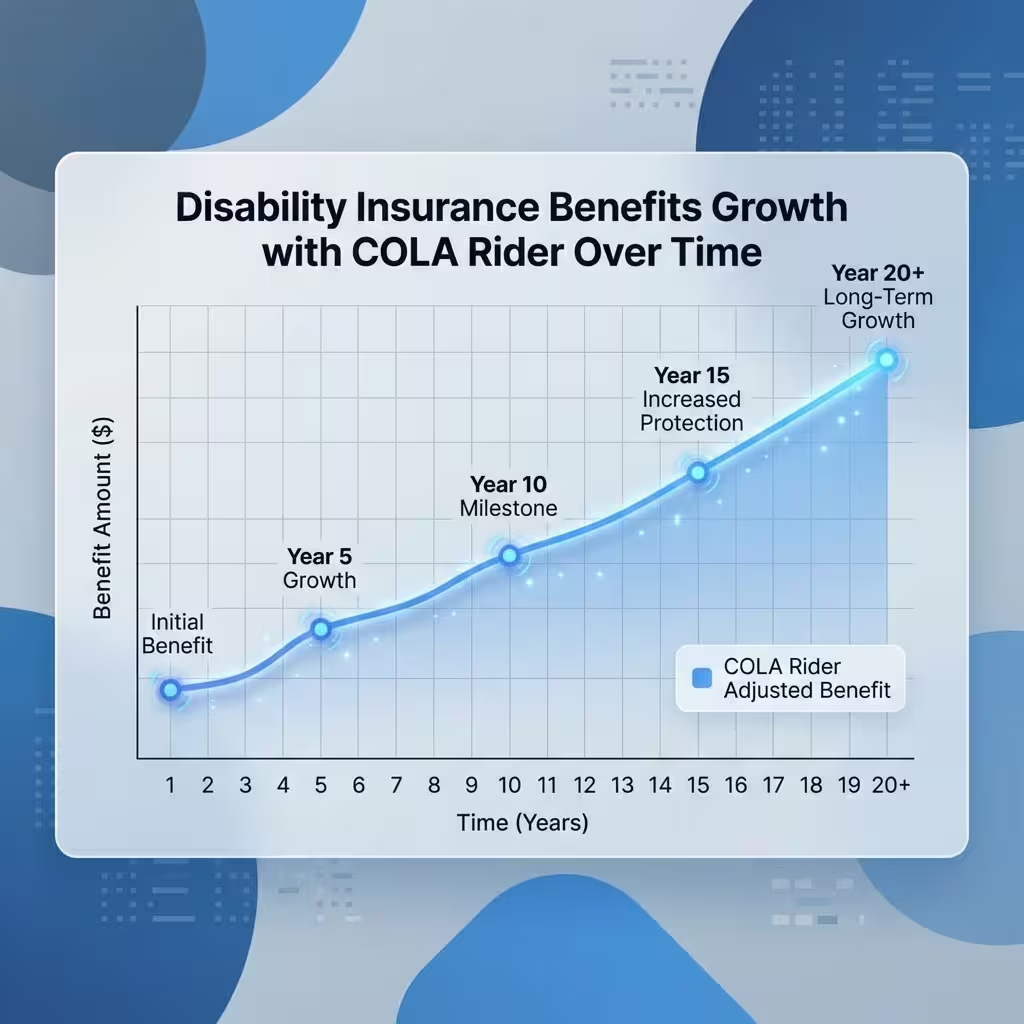

3. COLA Rider — Is the Cost of Living Adjustment Worth It?

Short answer: yes, if you’re under 50.

The COLA rider — cost of living adjustment — increases your monthly benefit each year while you’re on a disability claim. Most policies tie the adjustment either to the Consumer Price Index or to a fixed percentage, usually 3%. The compound version grows faster than the simple version, and the difference is significant over a long claim.

Here’s the math that makes this concrete.

You’re 36 years old. You become disabled. Your policy pays $14,000 a month. Without a COLA rider, that’s your number until age 65. Twenty-nine years from now. What does $14,000 buy in 2055? A lot less than it buys today. Groceries, utilities, healthcare costs — they all climb. Your benefit doesn’t.

With a 3% compound COLA rider, that same $14,000 grows to around $26,000 a month by the end of the benefit period. That’s not hypothetical math — that’s the actual inflation protection built into the rider.

For disability insurance riders for young professionals, the COLA is close to essential. The longer the potential claim period, the more value it delivers.

That math changes as you get older. A 57-year-old with an eight-year benefit period remaining gets much less value from a COLA rider than a 34-year-old does. The premium cost stays high, but the benefit window is short. At that point, many advisors recommend skipping it and putting the money toward a higher base benefit instead.

Ameritas, Guardian, and MassMutual all offer COLA options, though the structures differ. Some are simple, some compound, some CPI-linked. Before you sign, have your broker run the actual dollar projections for your age and benefit amount. The difference between a compound COLA and a simple one over 25 years is not small.

4. Catastrophic Disability Rider — The Extra Layer for Worst-Case Scenarios

This rider lives at the extreme end of the disability spectrum.

The catastrophic disability rider pays an additional benefit — on top of your base policy — if you become so severely disabled that you can’t perform two or more Activities of Daily Living. ADLs include things like bathing, dressing, eating, or moving from a bed to a chair without help. It can also kick in for severe cognitive impairment, or for what policies call “presumptive total disability” — things like complete loss of sight, hearing, or the use of both hands.

If that happens to you, the CAT rider adds a meaningful amount — often $5,000 to $10,000 a month or more — on top of whatever your base policy pays.

Now, is it worth it?

Honest answer: it depends where you are in building your coverage.

The case against: those events are rare, the premium is real, and some advisors argue you’d be better off just increasing your base monthly benefit by the same dollar amount. That’s not wrong.

The case for: catastrophic disabilities come with costs that income replacement doesn’t fully cover. Round-the-clock care. Home modifications. Assisted living that runs $8,000 to $15,000 a month in most major US cities. Your base benefit might cover your pre-disability lifestyle. It might not cover the lifestyle a catastrophic disability forces on you.

My take — if you’ve already built a solid base benefit and you have room in the budget, the CAT rider makes sense as a second layer of protection. If you’re still trying to get your base monthly benefit to an appropriate level, start there first.

5. Student Loan Protection Rider — Only If You Have the Right Kind of Debt

Medical school is expensive. That’s not a newsflash. The average physician leaves training carrying more than $200,000 in student loans. Specialists often hit $300,000 or beyond. So when a policy offers a rider that covers those loan payments during a disability — $2,000 to $2,500 a month is typical — it sounds like a no-brainer.

Except it’s not always necessary.

Here’s the piece most people aren’t told: federal student loans may be eligible for Total and Permanent Disability discharge through the U.S. Department of Education. If you qualify, the entire balance gets wiped out. Gone. No more payments. On top of that, Income-Driven Repayment plans calculate your payment as a percentage of discretionary income. If you’re disabled and have zero earned income, your required monthly payment under IDR is $0.

So for someone with only federal loans? The student loan protection rider is probably redundant. The federal safety net handles it.

But here’s the catch that trips people up. A lot of physicians — especially those who refinanced during residency to chase a lower interest rate — now have private loans. Private loans are not eligible for TPD discharge. Private lenders don’t offer IDR. If you get disabled and can’t work, those payments keep coming regardless.

For that group, the student loan protection rider shifts from “nice to have” to “genuinely necessary.”

Before you add this rider, check your loan types. Log into studentaid.gov and look at what you actually have. Then make the call.

6. Retirement Protection — What Happens to Your 401(k) When You Can’t Work?

This is the rider that almost never comes up in basic disability conversations, and that gap is a problem.

Think about a physician who becomes disabled at 43. Good base policy — $16,000 a month until age 65. That’s 22 years of income protection. But here’s what stops the day they stop working: 401(k) contributions. Employer matches. The compounding growth that was supposed to fund the back half of their life.

A disability policy protects monthly income. It doesn’t protect retirement savings.

That’s the gap the retirement protection rider addresses. MassMutual’s version is called RetireGuard. While you’re disabled, the insurer makes contributions into an irrevocable trust on your behalf — designed to replace the retirement savings you would have made if you’d kept working. When your disability benefit ends at 65, the trust funds are available.

The criticism of this rider is fair: the fees aren’t small. Some financial planners argue you’re better off buying a higher base benefit and investing the excess yourself. For a physician with investment discipline and a good advisor, that logic holds up.

For everyone else — and realistically, that’s a lot of people — having retirement contributions made automatically while you’re disabled is a meaningful form of protection that a base policy completely ignores.

My honest view: if you have a long benefit period and you’re in your 30s or 40s, this rider deserves a serious look. If you’re 55 and your benefit ends in 10 years, the math probably doesn’t work out as well.

How the Six Riders Stack Up

| Rider | What It Does | Who Needs It Most | Priority |

| Future Purchase Option | Lets you increase coverage later, no medical exam | Residents, fellows | Essential |

| Residual Disability Benefit | Pays partial benefits for partial income loss | Every physician | Essential |

| COLA Rider | Adjusts benefit for inflation while on claim | Physicians under 50 | High |

| Catastrophic Disability | Extra benefit for severe ADL-level impairment | Physicians with solid base coverage | Moderate |

| Student Loan Protection | Covers loan payments during disability | Private/refinanced loan holders only | Situational |

| Retirement Protection | Replaces retirement contributions while disabled | Long benefit period, 30s-40s | Moderate |

A Word on Budget: You Don’t Need All Six

This is the part most insurance content glosses over.

Stacking every rider onto a policy drives the premium up fast. Residents working on $65,000 don’t have unlimited room in their budget. Neither do a lot of early attendings still paying down debt.

The realistic approach: prioritize by career stage.

If you’re still in training, the Future Purchase Option and Residual Disability benefit are the two you shouldn’t skip. COLA is worth adding if the budget allows. The others can wait until income is higher and coverage can be expanded.

If you’re an attending with solid income, revisit everything. Get the base benefit to an appropriate level first — typically covering 60 to 70 percent of gross income. Then layer in COLA, and evaluate CAT and retirement protection based on your personal situation.

No two physicians have identical financial lives. The right rider stack for a 29-year-old orthopedic resident in Nashville looks nothing like what makes sense for a 48-year-old cardiologist in private practice in Dallas. That’s the whole point. Riders are how you make a standardized product actually fit your specific situation.

Back to Marcus.

He eventually found an independent advisor who walked him through what he’d missed. Getting new coverage with his diabetes diagnosis was harder and more expensive — but not impossible. He added a residual disability benefit and a COLA rider. The future purchase option from his original policy had expired unused. That window closed when he turned 35.

He’d have made different decisions at 27 if someone had explained this clearly.

That’s what this guide is for.

People Also Ask – PAA’s

What are disability insurance riders?

Riders are add-ons you attach to a base disability policy. Each one adds a specific type of protection — like partial benefits, inflation adjustments, or the ability to buy more coverage later. Most riders cost extra premium, and most have to be added when you first buy the policy, not years down the road.

What are the most common types of disability insurance riders available?

The six most common are the Future Purchase Option, Residual Disability Benefit, COLA rider, Catastrophic Disability rider, Student Loan Protection rider, and Retirement Protection rider. Most base policies also include a Waiver of Premium as a standard feature — that one suspends your premium payments while you’re collecting benefits.

Which companies offer the best disability insurance riders for freelancers?

Self-employed professionals and freelancers should stick to the Big 5 — Ameritas, Guardian, MassMutual, Principal, and The Standard. These are the only carriers offering True Own-Occupation coverage, which is rarely available through group plans or employer-sponsored policies. Guardian and Ameritas tend to get high marks for rider flexibility.

Can I add a residual disability rider to my existing policy?

Usually not after the fact. Riders are almost always added at the time of policy issue. A few carriers allow modifications at specific intervals, but it’s far more limited than most people expect. This is one of the main reasons getting the structure right from the beginning matters so much.

Is the cost of living adjustment rider worth it?

For anyone under 50 with a long potential benefit period — yes. A fixed benefit loses ground to inflation every year. A 3% compound COLA rider roughly doubles a benefit over 25 years. Its value drops significantly as the benefit period shortens, so physicians closer to 60 should run the numbers carefully before paying the premium.

About the Author

Selene Voss covers physician personal finance and insurance strategy. He has spent eight years focused on helping residents and early-career attendings understand long-term income protection, with writing appearing across medical finance publications and healthcare professional education platforms.

Disclaimer: This article is for informational and educational purposes only. It is not financial, legal, or insurance advice. Policy terms, rider availability, and eligibility vary by carrier and state. Always consult a licensed insurance professional before making any coverage decisions.