Last Updated: May 2026

My neighbor Terry works at a distribution center. Twelve years on the floor. Good at his job. Decent salary. When he blew out two discs last spring and the surgeon told him he’d be off his feet for at least four months, Terry wasn’t stressed about money. “I’ve got disability through work,” he told me. “I’m covered.”

He was not covered. Not the way he thought.

Short-term and long-term disability are two layers of the same protection strategy. For the full picture on how disability coverage works — including definitions, elimination periods, and what determines a valid claim — see our disability insurance guide.

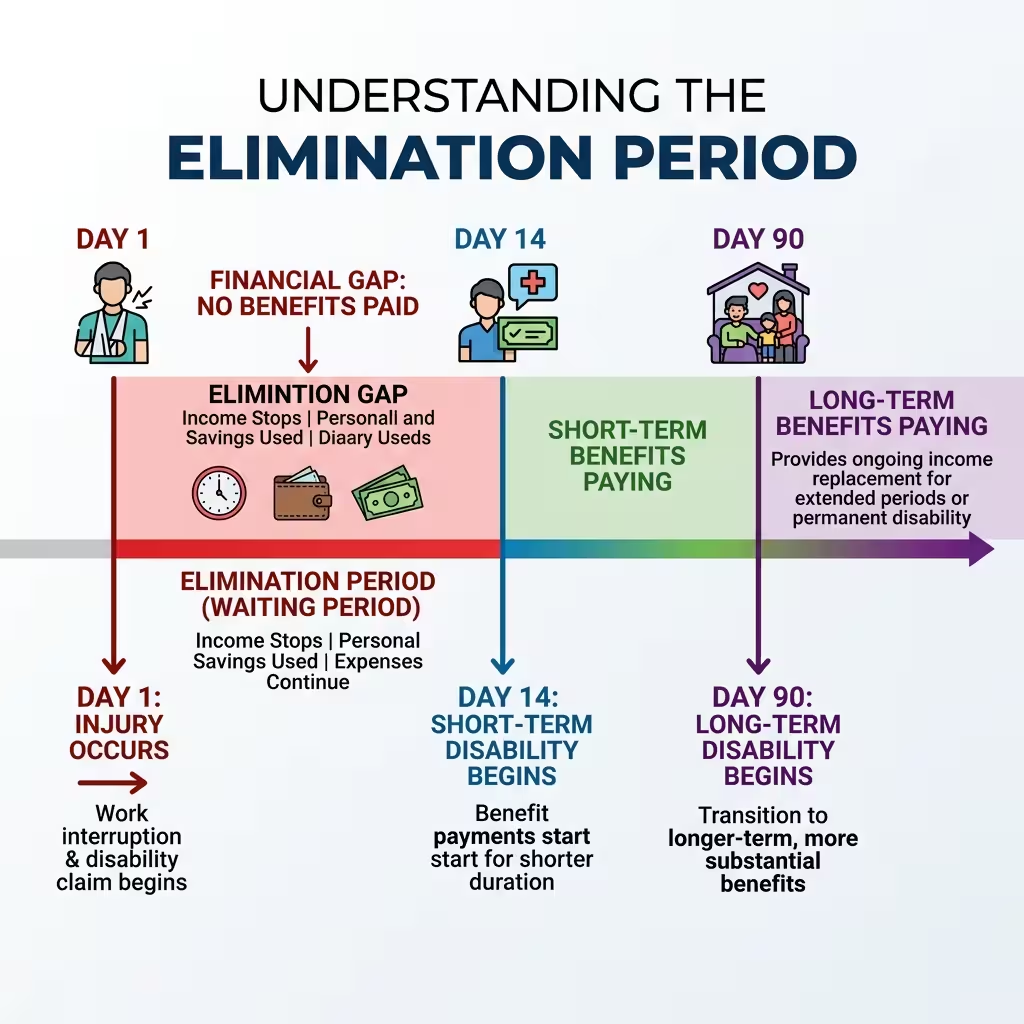

What Terry didn’t realize — what nobody had ever sat down and explained to him — was that his short-term disability policy had a 14-day elimination period baked in. He wouldn’t see a dollar for the first two weeks. And when his short-term benefits finally ran dry around week ten, his long-term disability plan had a 90-day elimination period that hadn’t even started counting from day one.

There was a gap. A real one. Three weeks with nothing coming in. Two mortgage payments late. His wife picked up weekend shifts.

That gap has a name. It’s called the elimination period. And if you don’t know where yours sits before something goes wrong, you’re going to learn about it the hard way — lying on a couch, leg elevated, watching your bank balance drop.

This is the part of short term vs long term disability insurance that the HR welcome packet leaves out. Let’s fix that.

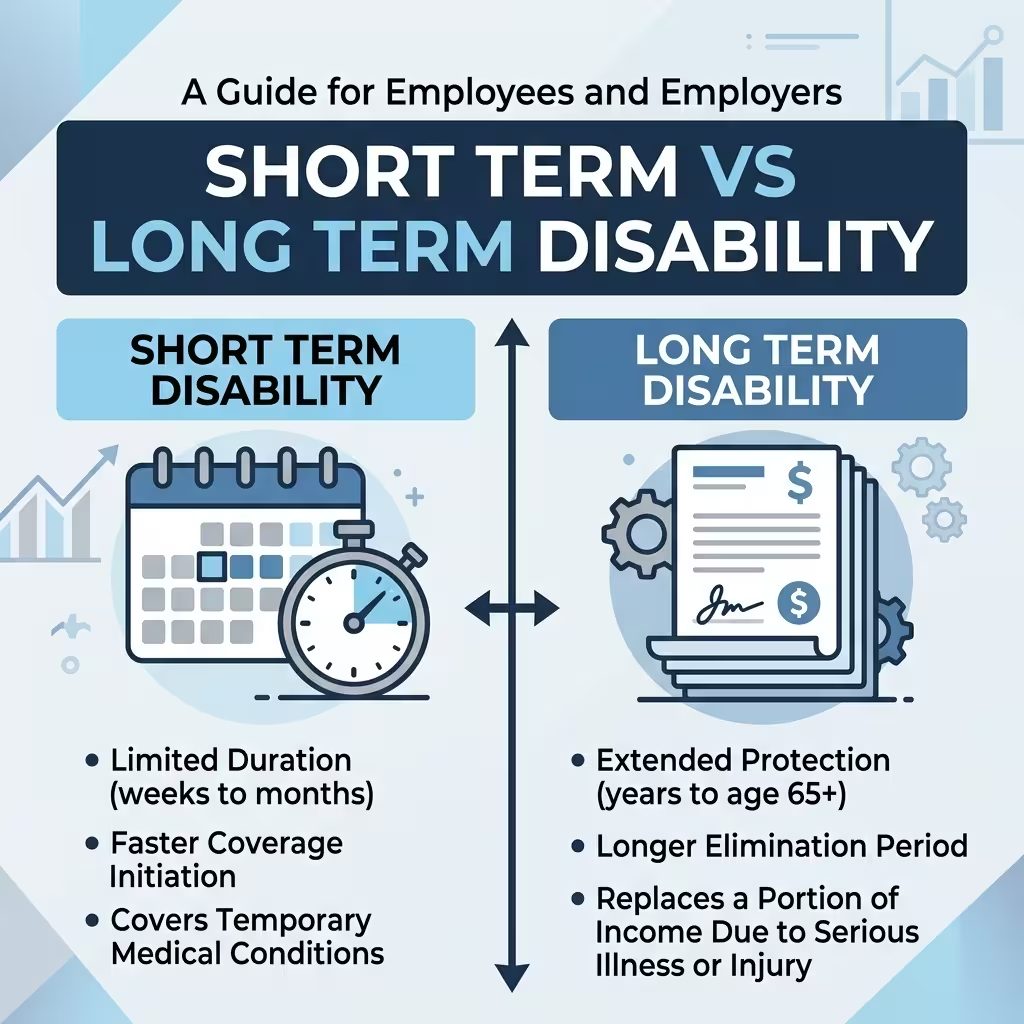

Short-Term Disability: What It Actually Does

Short-term disability insurance steps in when something stops you from working and it’s not a work injury. Think pregnancy leave, surgical recovery, a bad accident on your off day, or a mental health crisis that genuinely pulls you out of commission.

Mental health conditions — depression, anxiety, burnout — frequently require extended claims that go well beyond short-term windows. Our mental health disability insurance guide covers how these claims are evaluated and what documentation matters.

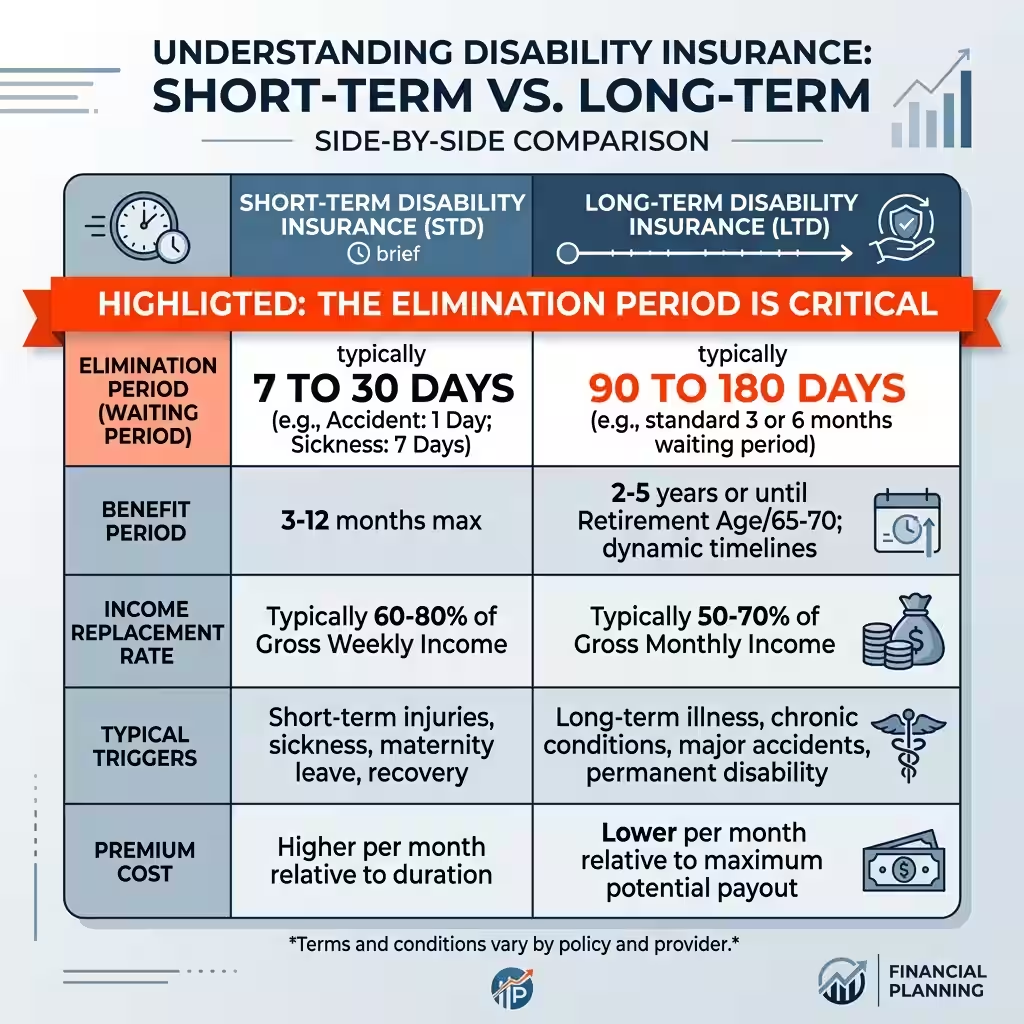

The policy replaces a chunk of your income — usually somewhere between 60% and 80% of what you normally earn per week. Most plans run for nine to fifty-two weeks before they stop paying out.

Here’s the thing most people skip past: the elimination period. For short-term policies, this usually runs between zero and thirty days, with fourteen days being about average. That means if something happens on a Monday, you don’t see your first check for two weeks. And that assumes everything goes smoothly with your claim.

Run the numbers on a real salary. If you take home $60,000 a year, your gross weekly pay is roughly $1,154. Two weeks with nothing — that’s over $2,300 sitting in a hole before any coverage kicks in.

If you’re a freelancer or self-employed person reading this — your situation is even messier, because group coverage through an employer isn’t available to you. Private individual policies exist, but the elimination periods and premiums vary wildly.

Now. If you’re sitting there wondering — is short term disability worth it if I have an emergency fund — the real question is: how long would that fund last? And would you still face a gap between when STD runs out and when LTD starts paying? That’s where people get surprised.

Long-Term Disability: The Coverage You Hope You Never Use

Long-term disability picks up where short-term leaves off. It’s built for situations that don’t resolve in a few months — chronic illness, spinal injuries that need multiple surgeries, conditions like MS or Parkinson’s that don’t follow a clean recovery schedule.

The benefit period is much longer. Some policies cover you for two years, some for five, some all the way until retirement age. The income replacement rate is typically 60% of your pre-disability earnings.

But the wait is longer. Much longer.

Most LTD plans have a 90-day elimination period. Some go to 180 days. A handful run to a full year. The tradeoff is premium — the longer you agree to wait, the lower your monthly cost. Which sounds like a reasonable deal until you’re at day 60 without income and you’ve got six weeks to go before the first LTD check could possibly arrive.

The federal program — Social Security Disability Insurance — is technically the ultimate long-term safety net. But SSDI has a mandatory five-month elimination period written directly into federal law. Five months from the date your disability begins before a single dollar is payable. The approval process on top of that can stretch another six months or more. People wait close to a year in some cases.

Most employer group plans focus on long-term disability and either skip short-term entirely or offer weak coverage. Our comparison of individual vs group disability insurance shows how these gaps typically look in practice.

The difference between short term and long term disability coverage, at its core, isn’t complicated: STD handles the first stretch. LTD handles what happens if you can’t go back. What trips people up is assuming those two things connect cleanly. They often don’t.

Short Term vs Long Term Disability – The Comparison That Actually Matters

| Feature | Short-Term Disability | Long-Term Disability |

| Elimination Period | 0–30 days (avg. 14 days) | 90–365 days (avg. 90 days) |

| Benefit Period | 9–52 weeks | 2 years to retirement age |

| Income Replacement | 60–80% of weekly wages | 60% of pre-disability income |

| Typical Triggers | Pregnancy, surgery, short illness | Chronic illness, serious injury |

| Federal Equivalent | N/A | SSDI — 5-month wait by law |

| Premium Cost | Lower | Higher |

The table looks clean. Real life is messier.

The number that determines whether you actually have money while you’re out of work is the elimination period — not the benefit amount, not the replacement rate. The elimination period is the gap between when your paycheck stops and when insurance money arrives. That’s it. That’s the whole game.

Why the Elimination Period Is the Number That Matters Most

Most people shopping for disability coverage ask one question: how much will I get? It’s the wrong first question.

The right first question is: when will I get it?

The elimination period is like a deductible you pay in time instead of money. Every day inside that window, you’re either spending savings, borrowing, or skipping bills. It doesn’t care that you’re hurt. It just keeps counting.

Choosing between short-term and long-term coverage depends partly on how much of each you already have through work — and how much more you need. Our guide to calculating disability insurance coverage helps you find the right number.

Here’s a real scenario. You have knee replacement surgery. Your doctor says twelve weeks off minimum. Your short-term disability policy has a 14-day elimination period. You lose two weeks. Then you collect STD for the remaining ten weeks. Tight, but workable.

Now say complications show up. Your recovery turns into six months. Your STD benefits end at week twelve. Your LTD has a 90-day elimination period — and depending on your policy language, that clock may have started on day one. Or it may only start the day your STD ran out.

If it’s the second option? You’re starting a fresh 90-day wait from scratch. That’s the gap. That’s where Terry ended up.

Before you sign anything, ask your benefits coordinator one question: does my LTD elimination period start from the onset of my disability, or from the last day of my STD benefits? That answer is worth more than anything else in the packet.

Real Numbers: What You Would Actually Collect

Say you earn $60,000 a year. Here’s how it plays out honestly.

Your weekly gross is about $1,154.

A short-term disability policy at 70% replacement pays roughly $808 per week — but only after your elimination period clears. Over a benefit period of ten weeks, you’d collect around $8,080 total.

A long-term disability policy at 60% pays about $693 per week. But after ninety days of waiting. If you go back to work at month three and a half, your LTD pays nothing. Zero. You’ve been paying premiums the whole time.

This is the real answer to — how much disability will I get if I make $60,000 a year? The benefit rate is only part of the picture. The elimination period decides whether that money ever reaches you at all.

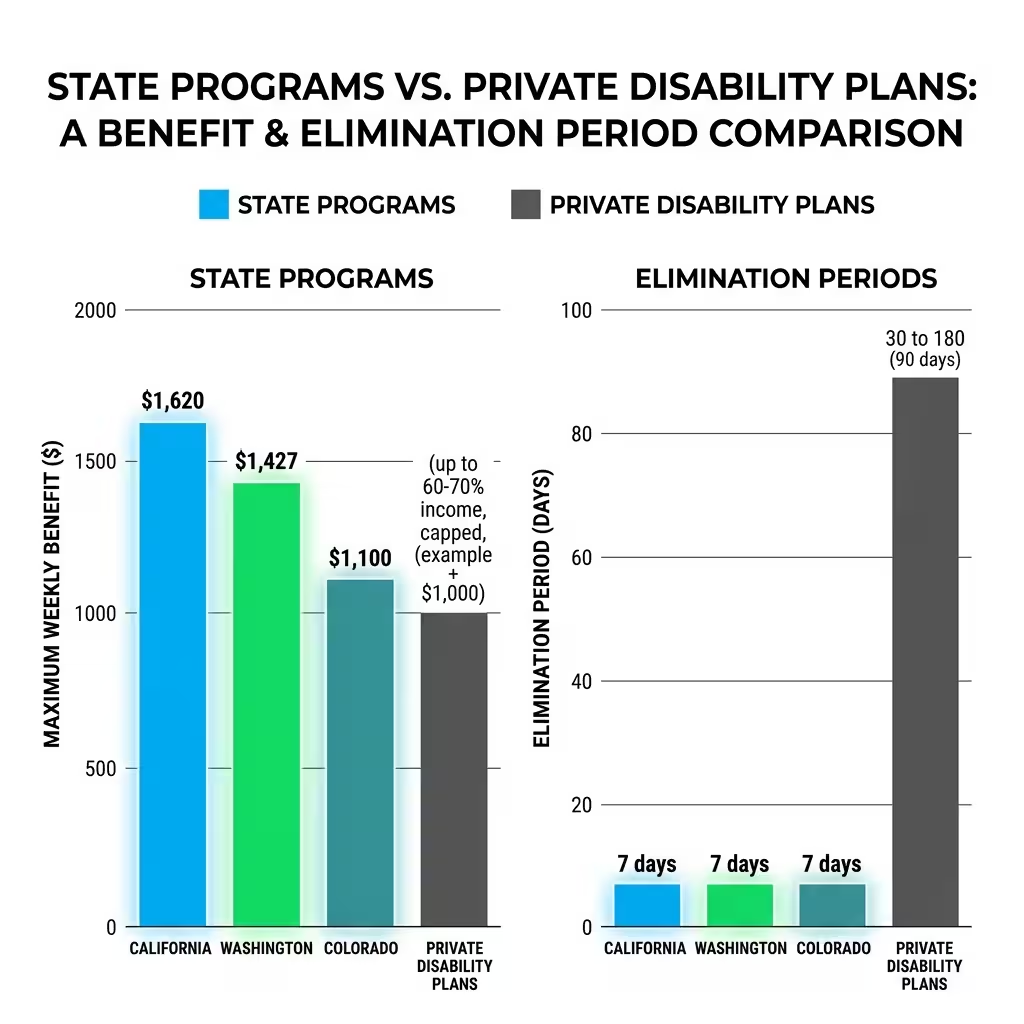

State programs can genuinely help. California’s SDI has a seven-day elimination period — far shorter than most private plans. Washington State’s PFML pays up to $1,647 a week in 2026. Colorado added twelve extra weeks of PFML leave this year if a newborn ends up in the NICU.

If you’re in California, Washington, Massachusetts, Colorado, or Minnesota — look hard at what your state program covers before buying extra private coverage. You may already have a bridge you don’t know about.

Should You Have Both?

In most cases — yes.

Short-term disability handles the first stretch after you get hurt or sick. Long-term disability handles the situation where things don’t get better on schedule. They’re not redundant. They’re sequential.

If you work in healthcare, construction, education, manufacturing, or any job that’s physically demanding — carrying both policies isn’t overkill. It’s just math.

People ask: can I get both short term and long term disability insurance from the same provider? Usually, yes. Most large insurers package them together. One company handling the handoff can make the claims process cleaner. But bundled doesn’t automatically mean better — compare the elimination periods on each piece separately, not just the combined premium.

What you want in a coordinated package: STD covers weeks one through twelve. LTD elimination period starts on day one of your disability — not day one after STD ends. That way the 90 days are running in the background while you’re collecting STD checks. When STD ends, LTD picks up with no cold restart.

Ask your HR team or insurance rep to draw that timeline out. If they can’t, that’s a red flag.

Claim Speed: The Real Story

People searching which insurance companies have the fastest approval for long-term disability claims are usually asking because they’re already in trouble. Or they know someone who is.

The blunt truth: there’s no insurer that rushes complex claims. What moves any approval faster — regardless of carrier — is documentation. Detailed, consistent records from your treating physician that directly link your condition to your job duties and your inability to perform them.

Vague notes slow things down. “Patient reports pain” gets a request for more records. “Patient is unable to stand for more than fifteen minutes due to documented L4-L5 herniation, which is required for his warehouse floor supervisor role” — that moves.

SSDI is the slowest. Initial decisions take three to six months. Denials on the first attempt are common, and appeals add more time. If you’re applying for SSDI, apply the same day you become disabled — not after waiting months. Every delay pushes your benefit start date out further.

Private LTD claims generally resolve in 45 to 90 days with clean documentation. Chronic conditions, mental health diagnoses, or anything subjective — budget for longer and get a disability attorney involved early. Most work on contingency and charge nothing unless they win.

People Also Ask – PAA’s

Should I choose short-term or long-term disability?

If you can only pick one and you’ve got three to six months of expenses in savings, lean toward long-term disability. The scenarios that wipe people out financially are the long ones — conditions that keep you out for a year or more. A savings cushion can bridge the STD gap. LTD is the one that protects against real collapse.

What is the main difference between short term and long term disability insurance?

Elimination period and duration. STD starts paying sooner — usually within two weeks — but stops in under a year. LTD makes you wait longer to collect (90 days or more) but can pay out for years. Most people need them to work together.

Is short-term disability worth it if I have an emergency fund?

Depends on the fund. If you can cover six to eight weeks of bills without stress, STD adds less urgency — especially if your LTD clock starts from day one of disability. But pregnancy leave and surgical recovery are the two situations where STD consistently earns its premium. If either is on your horizon, it’s worth keeping.

How much disability will I get if I make $60,000 a year?

At 70% through STD, roughly $808 a week after the elimination period. At 60% through LTD, about $693 a week — but only after 90 days without income. Whether benefits are taxable depends on how premiums were paid.

Can I get both short-term and long-term disability from the same provider?

Yes. Most major carriers offer both. The critical question: does the LTD elimination period start from day one of your disability or from the day STD ends? That one detail determines how the two policies actually connect.

What Terry Did After

Terry’s back at work now. Slower than before, but there. Once his mortgage situation stabilized, he sat down with his HR manager for the first time — really sat down — and went through every line of his benefit elections.

He found the gap. He closed it. He switched to a coordinated STD/LTD package where the 90-day LTD clock runs from day one of disability. Not from when STD stops.

“I had no idea,” he told me. “Nobody ever explained it.”

That’s the problem with short term vs long term disability coverage. The stuff that actually matters — where the elimination period sits, when the LTD clock starts, how the two policies connect — lives in pages nobody reads until there’s already a crisis happening.

Read those pages now. Ask the clock question. Check what your state’s PFML program covers. And if you’re choosing a longer LTD elimination period to save on premiums, make sure your savings can actually carry you through that window without bleeding out.

The weekly benefit looks great on paper. The elimination period is where the policy either pays off or falls apart.

Know yours before you need it.

About the Author

Selene Voss is a licensed insurance professional and employee benefits consultant based in the Midwest. She has spent over a decade helping employers in healthcare, logistics, and manufacturing design group disability programs and navigate PFML compliance. Jamie holds active insurance licenses in multiple states and has guided hundreds of workers through both private LTD and SSDI claims processes.

Disclaimer: This article is for general informational purposes only. It is not legal, financial, or insurance advice. Benefit amounts, elimination periods, and eligibility rules vary by policy, employer plan, and state. Always review your specific policy documents and speak with a licensed insurance professional before making coverage decisions. State program details and SSDI thresholds reflect information current as of April 2026.