Last Updated: May 2026

Marcus thought he had it figured out.

Fifteen years in software. Good pay. A benefits package with long-term disability coverage. He never worried much about it — it was just there, like the dental plan and the 401(k) match.

Then 2024 happened.

Over about eight months, his depression shifted. It stopped being background noise. It became the whole room. He couldn’t sleep. He’d sit down to code and his mind would go blank after twenty minutes. His doctor told him to stop working and file a disability claim.

He had everything. A diagnosis. A letter from his psychiatrist. Months of medical records.

Six weeks later, the denial letter arrived.

“No objective evidence of functional impairment.”

Marcus had never heard that phrase. Most people haven’t. But that one phrase is why more mental health disability insurance claims fail than any other reason. Not because people aren’t sick. Because people don’t know the rules before they walk in.

Mental health claims operate under the same policy structure as any other disability claim — but with added scrutiny. Our 2026 disability insurance guide covers the foundational mechanics, including the definition language that determines whether any claim — mental or physical — gets approved.

This guide is for you if you’re dealing with depression, anxiety, burnout, or a related condition — and you’re trying to figure out what you’re actually owed, how to build a claim that holds up, and what to do when a carrier says no.

What “Mental Health Coverage” Actually Means in Your Policy

Here’s where people get tripped up first.

Most group disability plans through employers do cover mental health. But the fine print almost always includes something called a mental nervous limitation. That’s a clause that caps your benefits for psychiatric conditions at 24 months — no matter how sick you are, no matter whether you’ve improved.

So yes, disability insurance for mental health exists. But for most people, there’s a hard stop built into the contract.

And it gets more complicated at that mark.

Most policies use two different definitions of disability depending on how long you’ve been on claim:

| Time on Claim | Standard Used | What It Means |

| Months 0–24 | “Own Occupation” | Can you do your specific job? |

| After Month 24 | “Any Occupation” | Can you do any job at all? |

Here’s why that matters. At month 24, two things happen at once. The standard gets tougher. And if your condition is classified as mental/nervous, the clock runs out entirely.

Disability attorneys call this the 24-month trap. It’s not a glitch — it’s by design.

Group plans frequently cap mental health benefits at 24 months — even when the same plan covers physical conditions to age 65. This is one of the starkest differences between group and individual coverage. See individual vs group disability insurance for a full comparison.

Can You Actually Get Money for Mental Illness?

Yes. The answer is yes.

But the path is narrower than most people expect, and it has nothing to do with how real your suffering is.

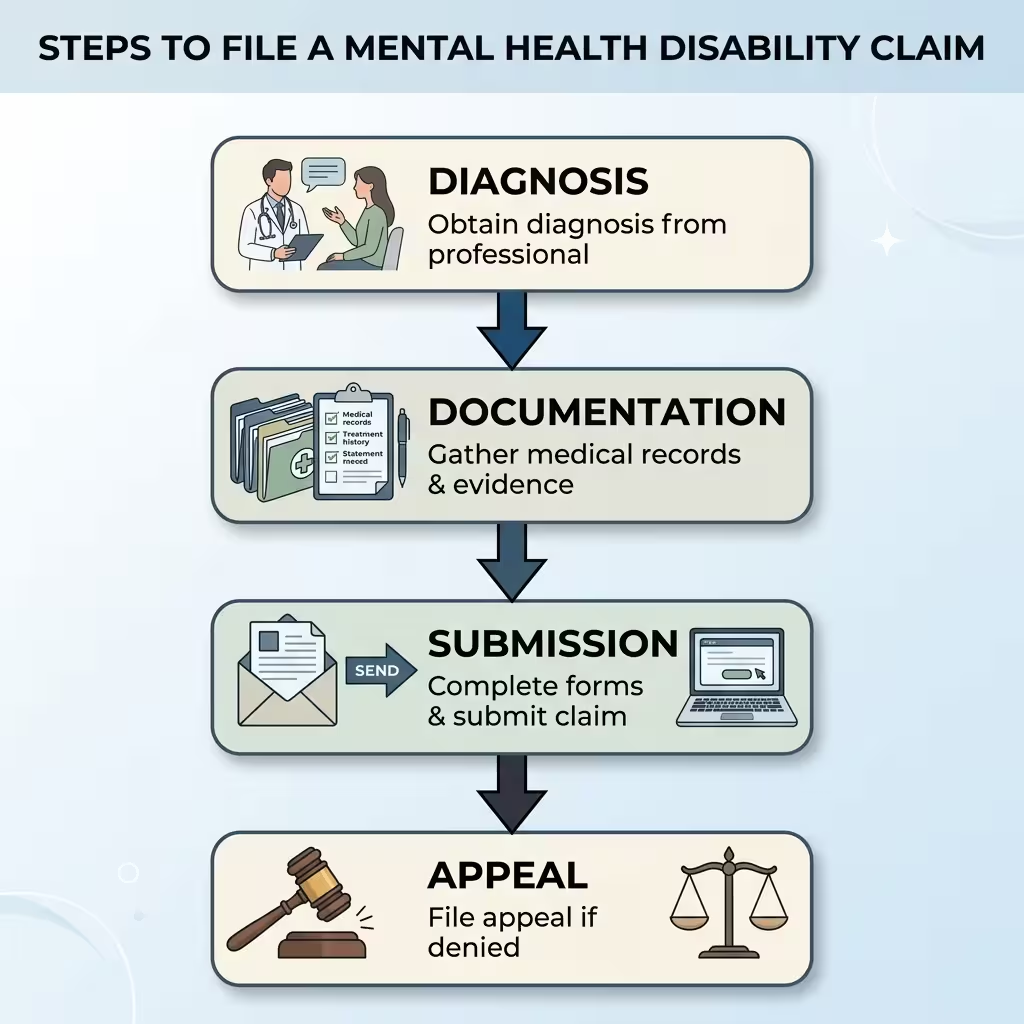

To qualify for mental health disability insurance benefits, you need three things in your file. Not one. All three.

First: a diagnosed condition. Major depressive disorder, generalized anxiety disorder, PTSD, panic disorder, bipolar disorder — all of these qualify under most policies. Diagnosis is the starting line, not the finish line.

Second: functional impairment that prevents you from working. This is where most claims succeed or fail. Insurers need to see that your condition blocks specific job tasks. “Cannot sustain concentration for more than 20 minutes” helps. “Feels depressed and overwhelmed” doesn’t. Your records need to show what you can’t do — not just how you feel.

A mental health condition that prevents you from practicing your specific specialty may not trigger benefits under any-occupation language — even with a clear diagnosis. Our guide to own-occupation vs any-occupation definitions explains why this matters for knowledge workers and professionals.

Third: objective evidence. This is what killed Marcus’s claim. Insurers want something measurable. Neuropsychological test results. Cognitive assessments. Formal capacity evaluations. Not just a doctor saying you seem impaired.

Mental health conditions now rank among the top causes of long-term disability — a pattern that’s been building for over a decade. Our breakdown of top causes of disability claims puts the mental health numbers in context alongside physical conditions.

That last requirement is, frankly, unfair. Depression doesn’t show up on an X-ray. Anxiety doesn’t produce a lab value. But the legal standard doesn’t care about fairness — it cares about documentation.

The 2025 Schwingle v. Hartford Life ruling made that plain. The plaintiff had real Long COVID symptoms — fatigue, brain fog, cognitive issues. The court still sided with the insurer. Why? Because she hadn’t completed formal neuropsychological testing. Her doctors had described her limitations, but she had no objective data to back them up. The court ruled the denial was legally defensible.

That’s where things stand right now.

The Real Reason Mental Health Claims Get Denied More

Let’s be direct about this.

Psychiatric claims face more resistance than physical ones. Not because the conditions are less serious. Because they’re harder to disprove — and that gives carriers more room to question them.

An insurer can’t argue your MRI shows no fracture if you never broke a bone. But they can argue your subjective symptoms of anxiety and depression aren’t backed by “objective findings.” That argument is easier to make, cheaper to defend, and often successful.

There’s another factor making this worse in 2026.

Approximately 71% of insurers now use AI to review disability claims. These systems scan thousands of records looking for patterns to flag for denial. One major carrier’s denial rate more than doubled after switching to AI review. Some of these tools reportedly carry error rates close to 90%.

Sound like a problem? It is.

California now requires a licensed clinician to personally review any AI-generated denial. Colorado has extended AI bias protections to health benefit plans. But if you’re in most other states, an algorithm can close your case — and there’s no requirement that a human ever looks at it.

What Is the 3-Month Rule in Mental Health Disability Claims?

This comes up a lot. Here’s the plain answer.

Most disability policies include what’s called an elimination period — a waiting window before benefits kick in. For many group plans, that’s 90 days. Some people call this the “3-month rule,” though it’s not a universal term.

During those 90 days, you must be consistently disabled and actively receiving medical care. That means therapy appointments. Psychiatric medication management. Documented clinical visits. You can’t go silent for six weeks and then expect the clock to count.

If you’re filing a disability claim for burnout and depression, this period is critical. Don’t miss appointments. Don’t take breaks from treatment thinking you’ll restart when you feel ready. Every gap becomes evidence against you.`

Depression, anxiety, and burnout-related claims often exceed short-term windows, making long-term coverage the relevant question. Our short-term vs long-term disability guide helps you evaluate which layer of coverage you actually need.

Your providers need to document functional limitations at every single visit — not just symptoms.

How the Parity Law Is Supposed to Protect You

Congress passed the Mental Health Parity and Addiction Equity Act — the MHPAEA — to fix something obvious: health plans were treating mental illness like a second-class condition.

The law says insurers can’t apply stricter limits to mental health benefits than they do to physical ones. If your plan covers knee replacement surgery without prior authorization, it can’t require prior authorization before approving outpatient treatment for depression. The standards have to match.

Federal enforcement ramped up significantly in 2025. The DOL and CMS sent more compliance demands to insurers than in any previous year. The violations they found were consistent across plans:

- Prior authorization for psychiatric care that isn’t required for comparable physical treatments

- Provider network standards that are harder to meet for mental health specialists

- Flat exclusions for therapies like Applied Behavior Analysis for autism

- Exclusions for nutritional counseling for eating disorders

Here’s something most people don’t know. Your employer is responsible for these violations — even if they hand benefits administration over to a third party. If the TPA messes up, you can hold your employer accountable.

That changes the leverage in a dispute. A lot.

Which Companies Offer Disability Insurance Plans That Include Mental Health Coverage?

All major carriers offer some form of mental health coverage. The differences are in the details — and the details are where claims get won or lost.

If you’re shopping for disability insurance with full mental health coverage, individual policies generally offer more flexibility than group plans. Three names that disability brokers frequently recommend for psychiatric-friendly terms are Guardian Life, Principal Financial, and MassMutual. These carriers have historically offered own-occupation coverage with fewer carve-outs for mental nervous conditions — though what’s available depends on your state and occupation class.

Before signing anything, ask these exact questions:

- Does this policy include a mental nervous limitation clause?

- Is the benefit period for psychiatric conditions the same as for physical ones?

- Does the disability definition change after 24 months?

- Will my treatment history affect how a claim is evaluated?

If the broker can’t answer those questions clearly, keep looking.

How to Apply for Disability Insurance If You Have a Pre-Existing Mental Health Condition

This is where people either get stuck or make costly mistakes.

For group plans through an employer — the ones tied to your job — you generally can’t be turned down or excluded during open enrollment because of a prior condition. That protection exists because of the ACA.

Individual plans are different. Carriers can deny you, exclude your condition from coverage, or charge more based on your history. Don’t try to hide anything on an individual policy application. Misrepresentation gives the insurer legal grounds to cancel your coverage at the worst possible time.

Work with an independent broker who has placed policies for people with psychiatric histories. This isn’t a general insurance question — it needs someone who knows how underwriting actually works for your situation. Some states also have guarantee-issue options or high-risk pools when private carriers won’t take you.

How to Build a Claim That Survives

Here’s what needs to be in your file. Every single piece matters.

Detailed clinical notes. Your doctor needs to write more than a diagnosis. They need to document what you can’t do. Not “patient struggles at work.” More like: “Patient cannot sustain focused attention for more than 20 minutes. Unable to manage multi-step tasks. Experiences significant emotional dysregulation in interpersonal settings.” Specific. Functional. Documented at every visit.

Neuropsychological testing. If you have cognitive symptoms — brain fog, memory issues, concentration problems — get formal testing. This produces measurable data that insurers can’t easily dismiss. It’s also what would have saved Schwingle’s claim.

Functional Capacity Evaluation. An FCE, done by an occupational therapist, measures your actual work capacity. It’s harder for a paper-reviewing adjuster to argue against than a clinician’s letter.

Daily symptom logs. Keep a running record. What you tried to do. What you couldn’t finish. How long things took. How you felt afterward. Conditions like depression and anxiety fluctuate — a log shows the pattern across time, not just a single appointment snapshot.

Third-party statements. A statement from your spouse, a close friend, or a former coworker who has watched you decline carries real weight. Especially on appeal. It’s corroboration from someone with nothing to gain.

Clean up social media. Insurers run surveillance. They search profiles. One photo from a birthday dinner doesn’t mean you can work full-time — but an adjuster will argue it does. Be aware of what you’re posting while a claim is open.

When They Deny You Anyway

Appeal. Every time.

The 2026 T.E. v. Anthem Blue Cross ruling out of the Sixth Circuit showed exactly what denial appeals can catch. The court found that Anthem had ignored treating clinicians entirely. The insurer had pulled selective quotes from records that showed stability — while leaving out notes documenting self-harm and repeated aggression. They couldn’t explain why they’d reversed their own initial approval of residential mental health treatment.

The court called it what it was: arbitrary and capricious. The case was sent back for a full and fair review.

Insurers make these errors more often than they should. They cherry-pick. They rely on reviews from physicians who never met you and spent eleven minutes on your file. They apply the wrong standard at the wrong time.

A strong appeal — or, when necessary, an ERISA lawsuit — catches those errors.

Most disability attorneys handle ERISA claims on contingency. No upfront cost. If your benefits are meaningful, one consultation to understand your options costs you nothing.

People Also Ask – PAA’s

Can you get money for mental illness if you’ve never been hospitalized?

Yes. Hospitalization isn’t a requirement. What matters is consistent outpatient treatment, a documented diagnosis, and clinical notes that specifically describe your functional limitations. The paper trail is everything.

What is the 3-month rule in mental health disability?

It’s the elimination period — typically 90 days of continuous disability with active medical treatment before benefits begin. Every appointment during that period needs to document your limitations, not just your symptoms.

Are there disability insurance providers specializing in mental health coverage?

Some individual carriers offer stronger psychiatric terms than others. Guardian, Principal, and MassMutual are frequently cited for own-occupation policies with fewer mental nervous carve-outs. Always review that clause before buying.

How can I apply for disability insurance if I have a pre-existing mental health condition?

For employer group plans, pre-existing conditions generally can’t bar you during open enrollment. For individual policies, work with a broker who knows psychiatric underwriting. Be honest on every application — misrepresentation voids coverage.

Which companies offer disability insurance plans that include mental health coverage?

Most major carriers include some coverage, but terms vary widely. The key factors to compare are the mental nervous limitation period, benefit duration, and whether the own-occupation definition applies past 24 months.

How do I file a disability claim for burnout and depression?

Notify your HR department and request claim forms right away. Get to your doctor and psychiatrist — their documentation of what you can’t do is the foundation of everything. Don’t gap your treatment. Keep copies of every submission and every response.

What Happened to Marcus

Marcus appealed.

His disability attorney requested the full claims file. In it was a record of the reviewing physician’s case notes. Eleven minutes. That’s how long the doctor spent reviewing fifteen years of someone’s career and eight months of someone’s collapse.

The attorney submitted formal neuropsychological testing ordered by Marcus’s psychiatrist. It showed measurable deficits in processing speed and sustained attention — exactly the kind of objective data the original claim was missing.

The appeal succeeded.

But it took eight more months. Eight months of savings disappearing. Of relationships stretched tight. Of fighting a system that was designed to make him quit.

The right documentation from the start would have shortened all of that.

If you’re reading this before you file — build the record now. If you’re reading this after a denial — appeal. Your condition is real. The rules are learnable. And the people who know those rules win cases like this every day.

Mental health disability insurance can be the bridge that keeps your life intact while you get better. Build your claim like it matters. It does.

About the Author This article was written by a benefits and disability insurance content specialist with over a decade covering ERISA litigation, mental health policy, and insurance compliance. It draws directly on 2025–2026 federal agency reports, published court decisions, and California legislative analysis.

Disclaimer: This article is for informational purposes only. It does not constitute legal or financial advice. Disability policies vary significantly by carrier, state, and employer plan. If you are filing or appealing a claim, consult a licensed disability attorney or benefits advisor in your state.