Last Updated: May 2026

It started with a Tuesday morning run.

Kyle, a 34-year-old freelance web developer from Austin, tripped on a cracked sidewalk three blocks from his house. Nothing dramatic. No dramatic fall story. Just a bad ankle fracture that needed surgery and eight weeks in a boot — no keyboard, no mouse, no billable hours.

Week one was fine. He had savings.

Week three, he called two clients to explain delays. Week six, he canceled a family vacation. By week eight, he’d pulled $11,000 from his retirement account. The taxes on that early withdrawal came later. That hurt too.

Kyle told me afterward he’d thought about disability insurance for freelancers before the accident. He’d even gotten a quote once. “I just figured it wouldn’t happen to me,” he said.

It happened.

If you’re a freelancer or independent contractor, your income is 100% dependent on your ability to show up and do the work. No PTO. No HR department. No sick pay waiting in a company system somewhere. That gap is real — and for gig economy workers, it’s wider than most people want to admit.

The disability insurance fundamentals apply whether you’re employed or self-employed — the policy structures, definition language, and claim mechanics are the same. Our disability insurance guide covers all of it as a starting point.

This guide covers what self employed disability insurance actually is, what it covers, and how to pick coverage that fits your situation before you’re the one making that phone call to your clients.

The Risk Nobody Talks About at Freelancer Meetups

Let’s get one thing out of the way.

Most freelancers obsess over client acquisition, rate negotiations, and invoice chasing. Fair enough — those things pay the bills. But ask a room full of 1099 workers who has disability coverage, and the hands that go up are depressingly few.

Here’s what the numbers say: 1 in 4 people who are 20 years old today will become disabled before they retire. That’s from the Social Security Administration. Not a scary insurance ad — a federal agency.

And the causes? They’re not what you picture.

Mental health conditions — depression, anxiety disorders, burnout-related illness — drove 34% of disability claims in 2026. Musculoskeletal problems came in second at 20%. Cancer at 17%. Accidents were only 7%. The freelancer hunched over a keyboard for ten hours a day isn’t immune to any of these. If anything, the isolation and financial pressure of self-employment can make some of them more likely.

Here’s the part that stings. Traditional employees have a cushion built into their job. Short-term disability coverage from HR. Sick leave. Job protection under FMLA. For someone on a W-2, a serious health setback is hard — but survivable.

For someone on a 1099? It’s a financial emergency from day one.

That’s the protection gap. And it’s not small.

So What Is Self Employed Disability Insurance, Exactly?

Plain and simple: it replaces your income when you can’t work.

You get sick. You get hurt. A chronic condition flares up badly enough to sideline you. The policy kicks in after a waiting period — called the elimination period — and starts paying you a monthly benefit. Usually somewhere between 60% and 80% of your average income.

That’s the foundation. But there’s a detail inside that definition that freelancers get wrong constantly.

Calculating the right benefit amount is trickier when income varies month to month. Our 4-step guide to how much disability insurance you need addresses variable-income scenarios specifically.

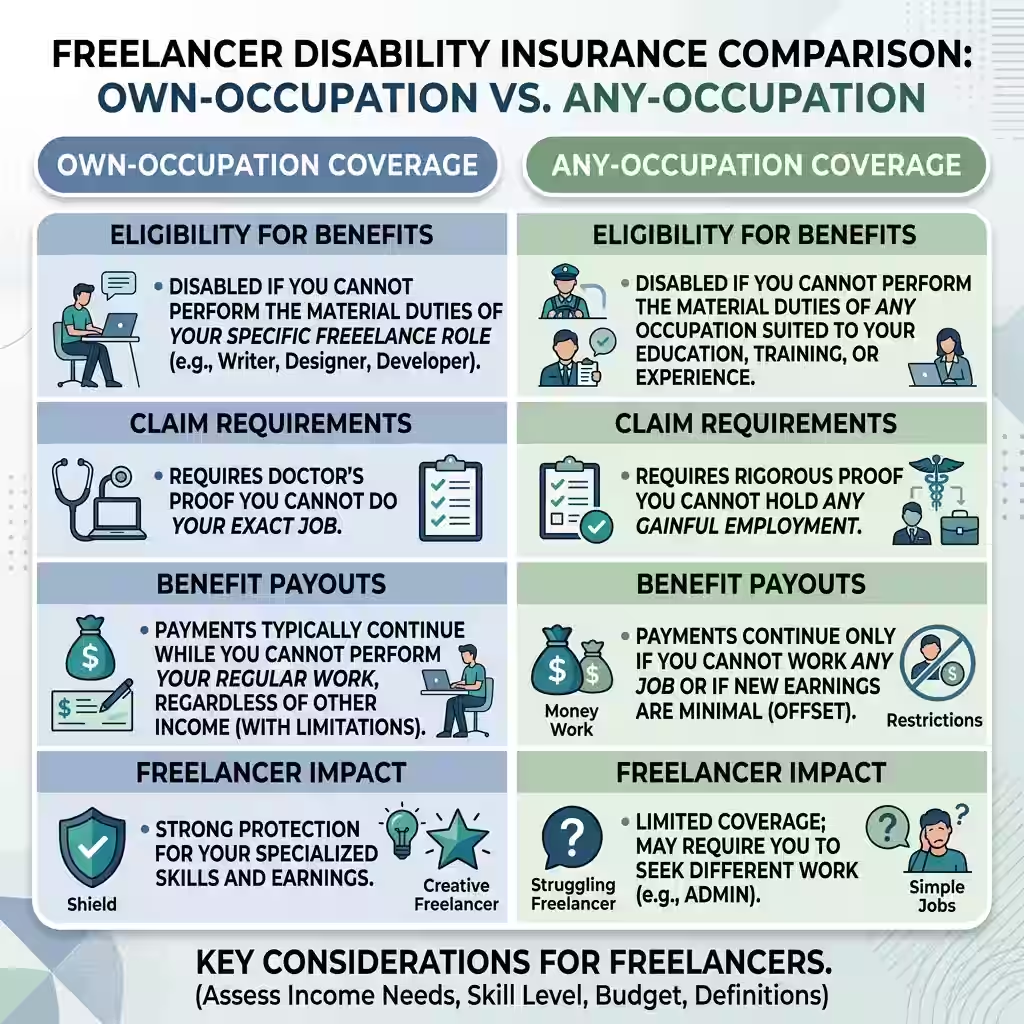

The definition of “disabled” isn’t standard. It varies massively.

Two types exist, and one of them is basically useless for skilled gig workers:

Any-Occupation coverage — You’re considered disabled only if you can’t do any job you’re reasonably qualified for. A hand injury that stops you from coding? If you could theoretically answer customer service calls, some policies won’t pay a dime.

Own-Occupation coverage — You’re disabled if you can’t do your specific job. The one you trained for. The one your clients pay you for. A designer who can’t use their dominant hand qualifies — period — regardless of what else they might theoretically do.

Own-Occupation policies cost more. I’d argue they’re non-negotiable for anyone earning $60,000 or more from freelance work. Paying for Any-Occupation coverage and then finding out at claim time that it doesn’t apply to your actual situation is one of the more expensive mistakes you can make.

Short-term policies typically pay for 3 to 6 months, with short elimination periods. Long-term policies can run all the way to age 65. Most smart freelancers pair a strong emergency fund — enough to cover the elimination period — with a long-term IDI policy that does the heavy lifting after.

What Are Your Real Options in 2026?

A note: Some links below connect to state program pages. We don’t earn commissions on state programs. For private policies, we recommend working with an independent insurance broker who quotes from multiple carriers — not one tied to a single company.

State Disability Insurance — Only in Five States, and You Have to Opt In

California, New York, New Jersey, Rhode Island, and Hawaii are the only states with State Disability Insurance (SDI) programs. If you’re in one of those states, this is worth understanding.

But here’s what most freelancers miss: these programs were built for employees. As a self-employed person, you usually aren’t automatically enrolled. You have to apply separately.

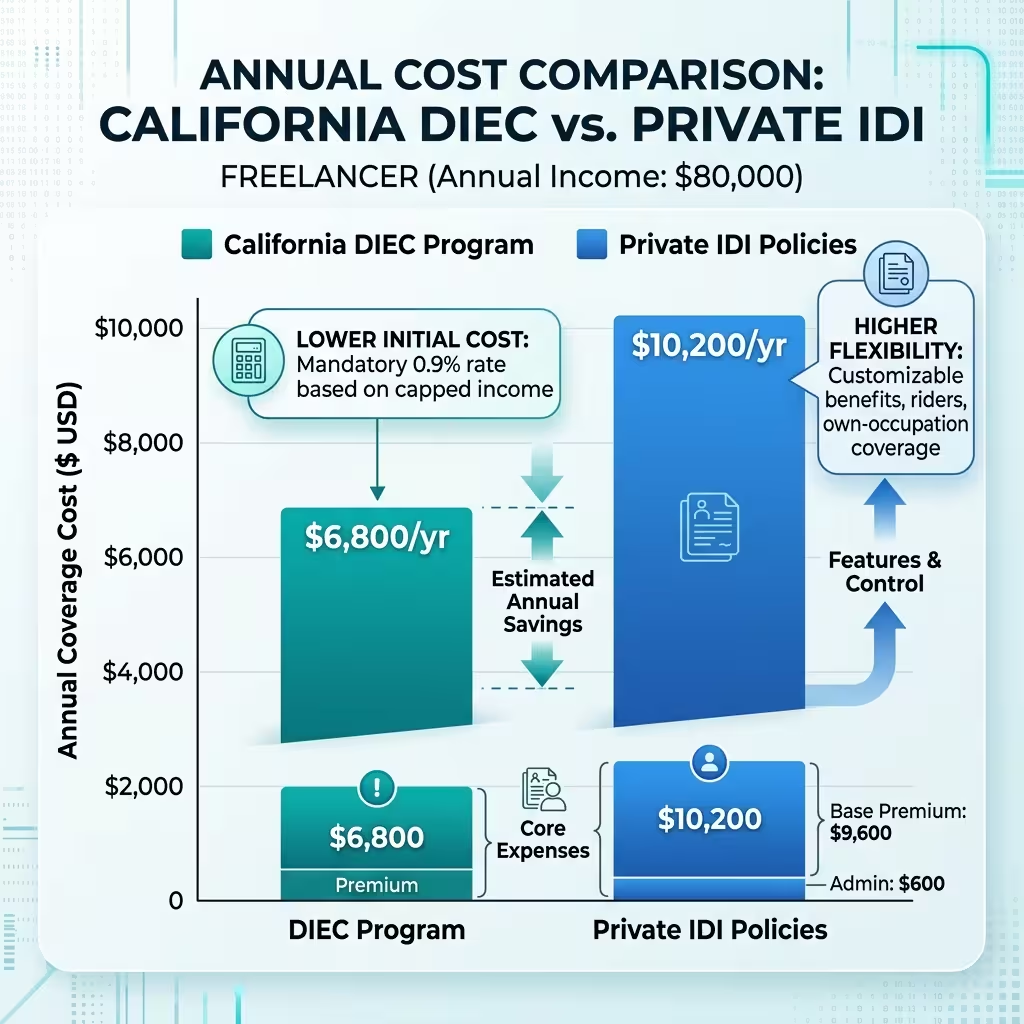

California’s DIEC — the Disability Insurance Elective Coverage program — lets self-employed Californians voluntarily opt in to state disability coverage. In 2026, California’s SDI contribution rate is 1.3%. The maximum weekly benefit is $1,765. The state fund is solid — projected to reach $3.9 billion by year-end.

Sounds great, right? There’s a catch.

Premium for DIEC is calculated at 8.84% of your net profit from your tax returns. For a freelancer clearing $80,000 a year net, that’s over $7,000 annually. And the benefit definition still leans toward Any-Occupation standards. High earners often find that a private IDI policy costs less and covers more.

Freelancers with specialized skills — designers, developers, writers, consultants — need the same own-occupation protection as physicians. Our comparison of own-occupation vs any-occupation definitions explains why the definition clause matters as much for independent professionals as it does for doctors.

New York’s SDI deducts at 0.5%, with a max benefit near $1,228 a week. New Jersey replaces up to 85% of average wages, capped at $1,119 per week. Meaningful money — but capped. If your freelance income runs higher than those numbers, state programs alone don’t cut it.

Individual Disability Insurance — The Serious Option for Freelancers Who Earn Real Money

If you’re a full-time freelance graphic designer, consultant, developer, photographer, or copywriter billing consistently above $50,000 a year, individual disability insurance is what you should be looking at.

IDI policies follow you everywhere. No job tied to them. No employer who can take the coverage away. You own it. You pay premiums with after-tax dollars — and when you collect benefits, they’re tax-free. Compare that to employer group coverage, where benefits are often taxable, and the real payout shrinks fast.

As a freelancer, you’re effectively always in the individual insurance market — there’s no employer group plan to rely on. Our guide to individual vs group disability insurance explains the tradeoffs between those two markets and why individual policies offer stronger protection.

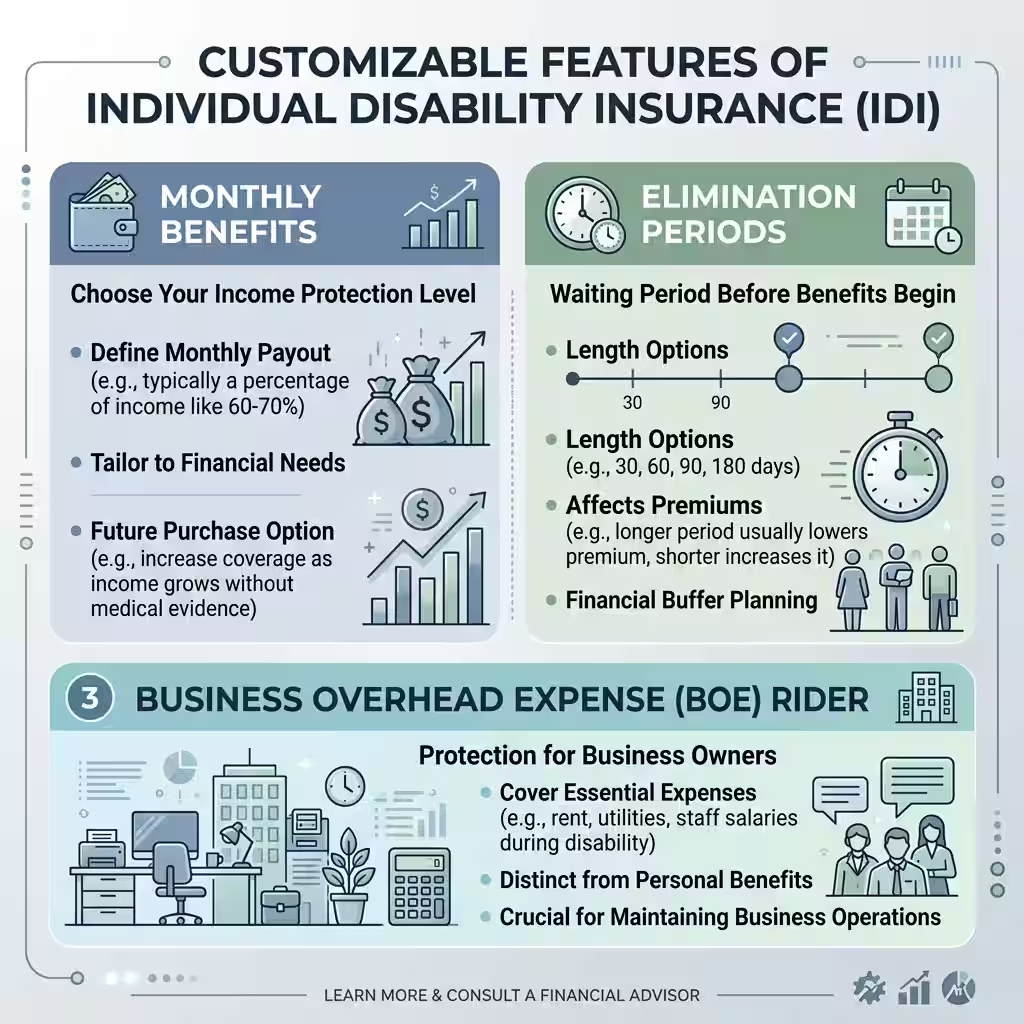

What you can customize:

- Monthly benefits structured to match your income (some carriers go up to $30,000/month for high earners)

- Elimination periods set to match your savings — 60, 90, or 180 days

- Business overhead expense riders that cover your rent, software, and contractor costs while you’re out

- Future Increase Options so you can add coverage later without new medical underwriting

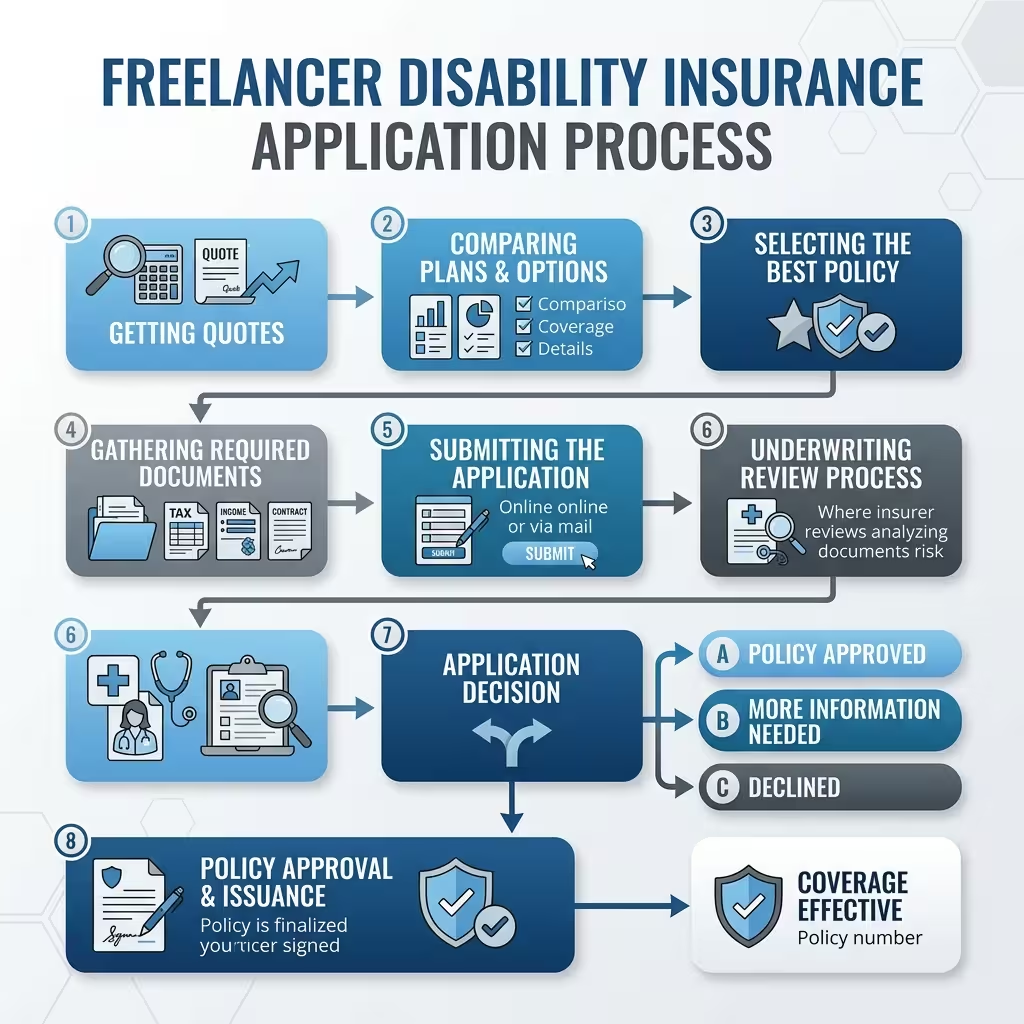

The honest downside? Underwriting is strict.

Carriers look at your net profit from tax returns — not gross revenue, net profit. Two or three years of inconsistent income can limit your approved benefit amount. Pre-existing conditions can complicate things. That’s the core reason to apply while you’re healthy and while your income is strong. Not after something happens.

For freelancers, who pays the premium is entirely up to you — and that choice has a direct impact on whether your benefits are taxable. Get the details in are disability insurance benefits taxable.

Portable Benefits — Newer, but Worth Watching

This one’s still early-stage, but it’s moving fast.

Alabama passed SB 86, effective December 31, 2025 — the first law in the country that lets businesses contribute to a freelancer’s benefit account with a clean tax structure. The business deducts 100% of the contribution. The contractor owes zero income tax on it. That’s a clean model.

Utah and Tennessee followed with similar voluntary portable benefits laws. At the federal level, the Unlocking Benefits for Independent Workers Act would create a national safe harbor — meaning companies could fund contractor benefit accounts without triggering misclassification claims.

None of this replaces a personal IDI policy right now. But if your biggest clients are larger companies, this is a conversation worth having. The landscape is shifting.

The Part That Changes How You Think About This

Most freelancers treat disability insurance as an abstract “what if.” Let me make it concrete.

Say you’re a freelance graphic designer. You net $72,000 a year. Something serious happens — a diagnosis, a surgery, a mental health crisis that takes you off work — and you’re out for five months.

Lost income: $30,000.

That’s before you factor in any business overhead that kept running. Software subscriptions. A shared office space. Maybe a contractor you had helping with projects. Add another $3,000 to $5,000 on top.

Now imagine you had a long-term IDI policy with a 90-day elimination period and a $4,500 monthly benefit. You cover the first three months with savings. The policy pays $9,000 for the final two months. Not a full replacement. But the difference between staying financially intact and raiding your retirement at a penalty.

Here’s what I think is underappreciated: most people who end up in financial crisis after a disability weren’t irresponsible. They just assumed it wouldn’t happen to them. Kyle assumed that. He was wrong. The risk is real — and it’s more manageable than people think when you plan ahead.

That’s the actual point.

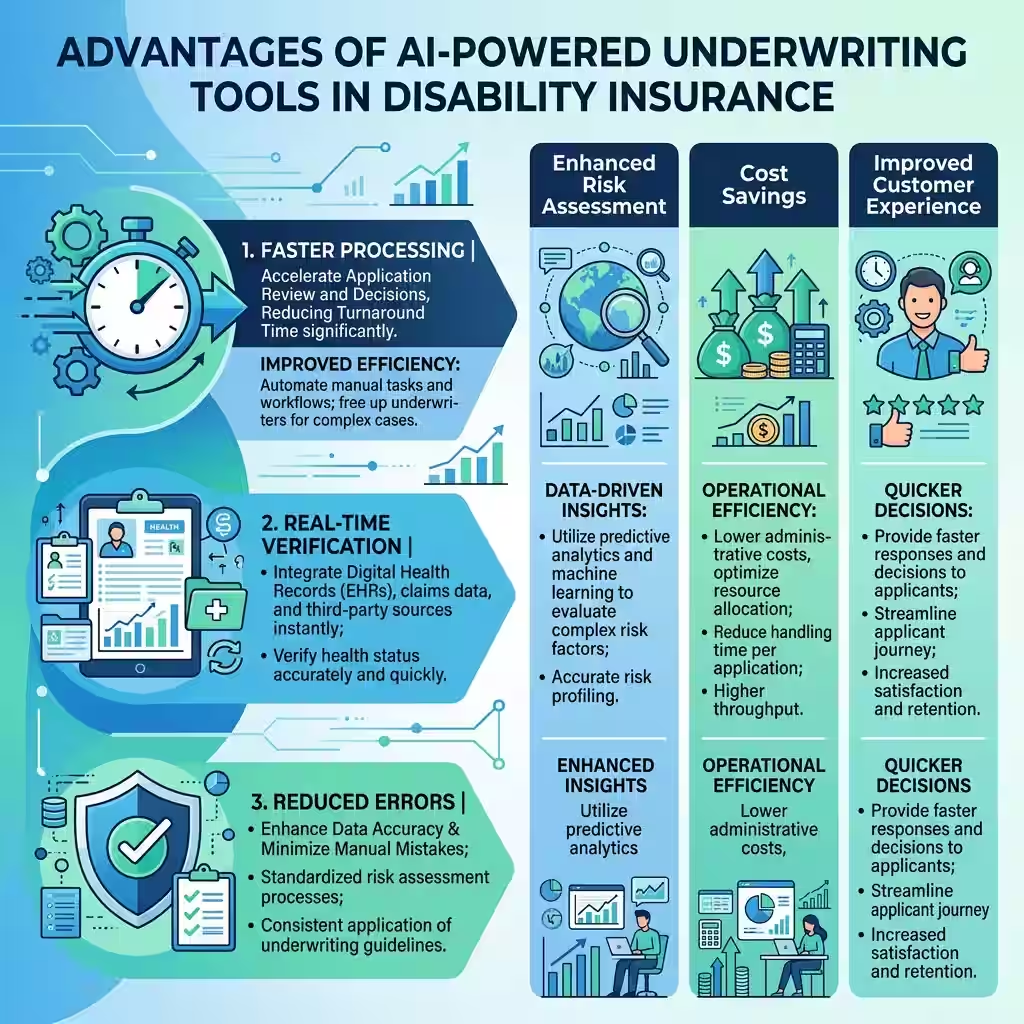

How AI Is Making Coverage Easier to Actually Buy

The coverage hasn’t changed. Getting it has.

In 2026, insurance platforms use AI-powered underwriting tools that process applications faster, connect directly to electronic health records for real-time verification, and cut administrative error rates by 40 to 60%. What used to take weeks of back-and-forth paperwork now moves in days.

Enrollment platforms using conversational tools have cut the time it takes to apply for coverage by 20 to 30%. For freelancers who’ve delayed buying a policy because the process felt like a second job — that excuse doesn’t hold up anymore.

People Also Ask – PPA’s

Should self-employed people have disability insurance?

Yes. And I’d go further — for most freelancers, it’s the single most important financial protection you can buy. Every safety net that W-2 employees take for granted doesn’t exist for you. A disability policy fills that gap. Without it, your savings is the only buffer between a bad diagnosis and financial collapse.

What are the best disability insurance options for freelancers?

It depends on your income and state. If you’re in California, New York, New Jersey, Rhode Island, or Hawaii, look at your state’s voluntary SDI program first — it’s cheaper for lower earners. For most full-time freelancers earning above $50,000 net, an individual Own-Occupation IDI policy from a carrier like Guardian, Principal, or MassMutual is the stronger option. Use an independent broker to compare — not a captive agent tied to one company.

How does disability insurance work for self-employed individuals?

You apply, provide 2 to 3 years of tax returns showing net profit, go through medical underwriting, and pay monthly premiums. If a covered disability keeps you from working, you collect a monthly benefit after your elimination period ends. Benefits from personally paid policies are generally tax-free.

Is affordable disability insurance for freelance graphic designers realistic?

Yes. For a healthy designer in their 30s, a long-term policy with a 90-day elimination period and a $3,500 to $4,500 monthly benefit typically runs $100 to $200 per month. That’s less than most people’s gym membership and car insurance combined — for coverage that replaces your income.

What is gig economy income protection?

It’s the collection of tools freelancers use to stay financially stable when work stops — disability insurance, emergency savings, business overhead expense coverage, and the emerging wave of portable benefits programs. Disability insurance is the most critical and structured piece of that system.

What does the elimination period mean?

It’s the waiting period before your benefits start — typically 30, 60, 90, or 180 days. You cover that window with savings. Longer elimination periods mean lower premiums. Most freelancers with 3 to 6 months of savings do well with a 90-day elimination period.

Back to Kyle.

He recovered. It took nearly a year to rebuild what he pulled from his retirement account, including the tax hit. He bought an Own-Occupation IDI policy six weeks after getting back to work. His premium is $147 a month.

“I think about it like this,” he told me. “My income is my whole business. It made no sense not to insure it.”

That’s the right way to think about disability insurance for freelancers. You insure your car. You insure your apartment. Your ability to earn — the thing everything else depends on — deserves the same treatment.

About the Author Selene Voss is an independent finance and insurance writer with eight years covering 1099 workers, self-employment benefits, and personal finance for the gig economy. Prior to writing full-time, they spent five years as a licensed insurance professional advising independent contractors on income protection strategies.

Disclaimer: This article is for informational purposes only and does not constitute financial or insurance advice. Coverage options, rates, and eligibility rules vary by state and carrier. Speak with a licensed insurance professional before buying any disability policy.