Last Updated: May 2026

My neighbor found out the hard way.

He’s a dentist. Late 30s, solid practice, two kids in school. Fell off a ladder cleaning gutters — broke his wrist, damaged two tendons. Couldn’t operate for seven months.

His group disability plan at work paid him $3,200 a month. Sounds fine until you know his mortgage alone was $3,800.

He told me later he never actually read his policy. He just assumed “disability insurance” meant he’d be okay. That assumption cost him about $40,000 in depleted savings before he was back in the chair.

That story is why this guide exists.

Figuring out how much disability insurance do i need? isn’t something most people ever actually sit down and calculate. They assume their job’s group plan covers it. Or they figure Social Security will kick in. The truth is messier than that, and the gap between what people think they have and what they’d actually receive in a real disability is — in most cases — enormous.

If you’re not yet familiar with how disability policies are structured — what definitions, elimination periods, and benefit periods mean — our disability insurance guide covers all of that foundation before you run the numbers.

Let’s fix that. Step by step.

The Social Security Number Nobody Warns You About

Before we get to your personal calculator, we need to talk about Social Security Disability Insurance. Because a lot of people are counting on it more than they should be.

Here’s the 2026 reality.

The maximum monthly SSDI payment is $4,152. But the average monthly payment is roughly $1,630. That’s the number most working Americans would actually receive — not the max. And $1,630 a month doesn’t cover rent in most U.S. cities, let alone a mortgage, car payment, utilities, food, and out-of-pocket healthcare costs on top.

There’s another problem. SSDI has a five-month waiting period before benefits start. Then the application process itself typically drags on for 12 to 24 months. Most first applications get denied. You can be waiting over two years with zero income from Social Security while your bills keep piling up on schedule.

And the math gets worse the more you earn.

The SSA uses what they call “bend points” to calculate your benefit. For 2026, the formula works like this: they replace 90% of your first $1,286 in monthly earnings, then only 32% of earnings between $1,286 and $7,749, and just 15% of anything above $7,749. The higher your income, the smaller the percentage SSDI actually replaces. A physician earning $250,000 a year gets almost as little from SSDI as someone earning $80,000.

This is why private disability income insurance exists. It fills the gap between what you actually need and what the government will actually send.

Step 1: What’s Your Real Monthly Net Income?

Not your salary. Your take-home.

Gross income is a lie for planning purposes. What matters is the money that lands in your bank account after taxes, 401(k), health insurance, and everything else gets pulled out. That’s what your household actually runs on. That’s what disappears when you can’t work.

Quick way to estimate it:

Monthly Net = (Annual Gross Salary × 0.70) ÷ 12

That assumes about a 30% effective tax burden. If you want precision, pull your last three bank statements and average the actual deposits.

A $150,000 salary? You’re probably netting around $8,750 a month. A $200,000 salary? Figure roughly $11,667 per month. A $100,000 salary? Closer to $5,833.

Write your number down. That’s your target — the income your household needs replaced.

One factor that affects your target coverage amount: whether your benefits will be taxable. The answer depends on who pays the premiums. See are disability insurance benefits taxable to factor this into your calculations.

Step 2: Your Non-Negotiable Monthly Expenses

This is the part people skip. Don’t skip it.

Go through your last two months of bank and credit card statements. Find every expense that doesn’t stop if you stop working. Not subscriptions you could cancel. Not dinners out you could skip. The bills that show up regardless.

Write down:

- Mortgage or rent payment

- Car loan(s)

- Minimum student loan payments

- Health insurance premiums (these don’t go away — they often get more expensive)

- Utilities: electric, gas, water, internet

- Groceries

- Childcare, if applicable

- Any other fixed debt payments

Add them up. That total is your floor — the minimum your household needs to survive financially each month without selling assets or going into debt.

For most American families, this number lands between 60% and 75% of monthly net income. Sometimes higher.

Now ask yourself one question: if you became disabled tomorrow, how much of that floor would actually be covered?

Step 3: Take Stock of What You Already Have

This step surprises people.

Most workers have some disability coverage already. The question is whether it’s anywhere near enough.

Group long-term disability through your employer. Most plans replace 60% of your pre-disability gross income — not net. And almost every group plan has a monthly cap. Common caps: $5,000, $8,000, or $10,000 per month. If you earn $200,000 a year and your plan caps at $5,000 monthly, you’re already looking at a $7,800/month gap before anything else factors in.

Before counting your employer’s group plan toward your coverage total, it’s worth understanding its actual limitations. Our comparison of individual vs group disability insurance will help you assess what your workplace plan is actually worth.

One more thing about group plans. They’re employer-owned. If you leave your job — or lose it — the coverage goes with it. You can’t take it with you.

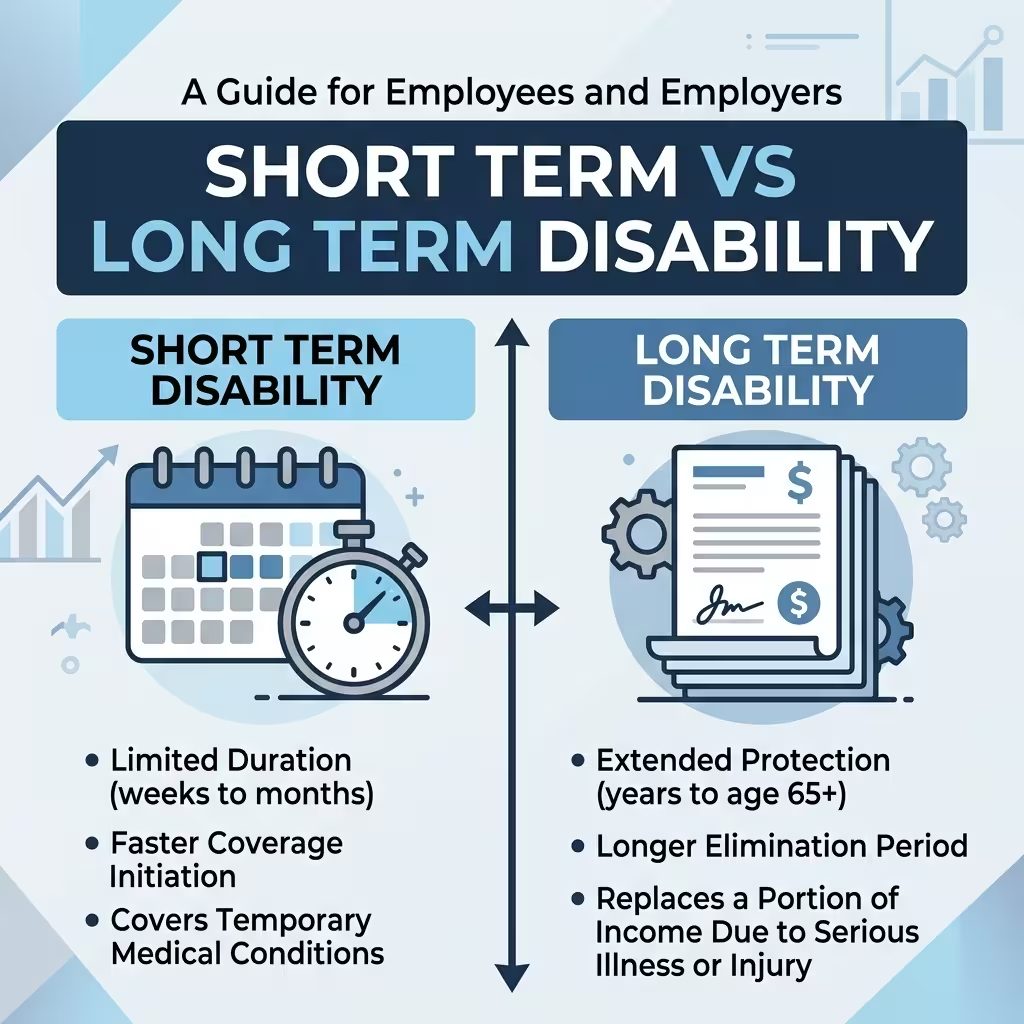

Short-term disability. Usually covers 60–70% of income for 90 to 180 days. It bridges the gap between day one and when long-term coverage begins. If your employer doesn’t offer it, your emergency fund has to do that job.

SSDI. You now know the 2026 numbers. Log into ssa.gov and look at your actual Social Security statement. It shows your projected disability benefit based on your earnings history. Use that real number — not the $4,152 maximum.

Add your existing coverage together. Then compare it to your essential expense floor from Step 2.

The difference is your coverage gap. That number is exactly how much additional private disability insurance you need.

Step 4: The Disability Insurance Calculator — Your Actual Numbers

Here’s the math laid out clean.

1. Monthly net income — your take-home pay per month 2. Essential monthly expenses — the floor from Step 2 3. Existing coverage — group LTD monthly benefit + your actual projected SSDI 4. Coverage gap — Line 2 minus Line 3 5. Private IDI target — round up to the nearest $500

Real Example: $200,000 Salary (Physician)

| Line Item | Amount |

| Monthly net income | ~$11,667 |

| Essential monthly expenses | $8,500 |

| Group LTD benefit (capped at $5,000) | $5,000 |

| Projected SSDI benefit (high earner) | ~$2,800 |

| Total existing coverage | $7,800 |

| Monthly gap | $700 |

In this example, the gap looks manageable. But change one variable — say, the group LTD cap drops to $3,500, which is common in older plans — and the gap jumps to $3,300 per month instantly.

Real Example: $100,000 Salary (Marketing Director)

| Line Item | Amount |

| Monthly net income | ~$5,833 |

| Essential monthly expenses | $4,200 |

| Group LTD benefit (60%, capped at $5,000) | $3,500 |

| Projected SSDI benefit | ~$1,800 |

| Total existing coverage | $5,300 |

| Monthly gap | $0 — actually overcovered |

Wait. Does that mean this person doesn’t need private IDI?

Not exactly. Group LTD is tied to employment. Lose the job, lose the coverage. A personal IDI policy that you own and control protects you regardless of where you work. It’s portable. That’s worth something.

The Part Nobody Mentions (But Should)

Here’s where I’ll be blunt about something the insurance industry doesn’t love to advertise.

The income replacement insurance amount you can buy is limited. Individual disability carriers won’t just hand you a policy for 100% of your income — most cap coverage at 60–70% of pre-disability gross. The reasoning: if disability insurance replaced 100%, some people might choose not to return to work. That’s not cynicism, it’s actuarial reality, and most carriers design around it.

Which means there’s a ceiling to how much gap you can close with private coverage. For very high earners — surgeons earning $500,000+, for instance — maximum issue limits from a single carrier may top out around $30,000/month. To get coverage above that, you’d need multiple policies from different carriers. That’s called “stacking,” and it’s a legitimate strategy.

Also: benefits from individually-owned IDI policies are tax-free if you paid the premiums with after-tax dollars. That changes the math. A $6,000/month tax-free disability benefit is worth more than a $6,000 taxable benefit. Factor that in when comparing to your net income replacement target.

How Much Long Term Disability Insurance Do I Need? It Depends on Who You Are.

If you’re a physician or surgeon asking “how much disability insurance do I need”

Stop here, because this deserves its own section.

Doctors face a problem the standard formula doesn’t capture. A hand surgeon who loses grip strength can’t operate. But they might still be able to do hospital administration or consult. Most group LTD plans would look at that and say “you can still work — benefits denied.”

That’s why true own-occupation disability insurance is non-negotiable for medical specialists. Under a genuine own-occ policy, you’re considered totally disabled if you can’t perform the specific duties of your specialty — even if you’re physically capable of other work. You keep your full benefit while earning income in a different role.

Doctors and surgeons made up 33% of all new individual disability insurance premiums in 2024. That’s not a coincidence. Medical professionals understand what they stand to lose.

If you’re a physician with a group plan only, you’re underinsured. Period.

If you’re self-employed

Your calculation starts at zero for existing employer coverage.

No group LTD. No employer contribution. Nothing — unless you’ve bought it yourself already. That means the entire gap between your essential expenses and your projected SSDI benefit needs to be covered by a private policy.

Self-employed professionals — consultants, freelancers, independent contractors, small business owners — are the most exposed group in the country on this issue. They also tend to have the most irregular income, which makes SSDI calculations tricky because the SSA uses your reported earnings history. If you’ve underreported income for years, your projected SSDI benefit will be lower than you expect.

Target: 60–70% of your average monthly gross income over the last 24 months.

How much short term disability insurance do I need?

Short-term coverage handles the first 90 to 180 days of a disability. Most people need it to cover the elimination period on their long-term policy — that waiting window before long-term benefits kick in.

Part of the coverage calculation depends on how long you can self-fund the elimination period. Understanding short-term vs long-term disability insurance helps you decide whether short-term coverage is worth adding to the stack.

If your emergency fund has three to six months of expenses sitting liquid, you can self-insure the short-term gap and save money on premiums. If it doesn’t — you need short-term coverage.

One scenario where short-term disability matters a lot: pregnancy. Most policies cover maternity leave as a medical disability (typically 6 weeks for vaginal delivery, 8 weeks for C-section). Buy the policy before you’re pregnant. Pre-existing condition exclusions are real.

Inflation and the Long Game — Why This Isn’t a One-Time Calculation

Most people calculate their disability insurance need once. They buy a policy. They stop thinking about it.

That’s a mistake.

Here’s why. At 3% annual inflation, prices double in 24 years — that’s the Rule of 72 at work. A $5,000/month benefit you buy today is worth $2,500 in real purchasing power by 2050. If you’re disabled at 40 and collecting benefits to age 65, the early years feel fine. The later years don’t.

The 2026 Social Security COLA is 2.8%. That helps. But SSDI tracks the CPI-W — the Consumer Price Index for Urban Wage Earners and Clerical Workers. The problem is that CPI-W is built around working-age spending patterns. Disabled Americans and retirees tend to spend more on healthcare, which consistently outpaces general inflation. Your real cost of living rises faster than your SSDI benefit does.

Private IDI policies solve this with a COLA rider — a feature that increases your benefit each year of a disability claim, either by a fixed rate (often 3%) or tied to the actual CPI (sometimes capped at 6%). Compound COLA riders are better than simple ones over a long claim. The math adds up fast over a 20-year disability.

Buy the COLA rider. It matters more than most people realize.

What Does It Actually Cost?

Fair question.

Individual disability income insurance typically runs 1% to 3% of your annual income in premiums. For a 40-year-old white-collar professional earning $120,000 a year, that’s somewhere between $1,200 and $3,600 annually — or $100 to $300 per month.

Several things affect that number:

- Your occupation. Medical professionals and white-collar workers get better rates than physical-labor jobs. Most carriers assign an occupational class (1 through 5 or 6) that heavily influences your premium.

- Elimination period. A 90-day wait — the industry standard, used in 73% of all new policies sold — costs less than a 30-day wait.

- Benefit period. A policy that pays to age 65 or 67 costs more than one that caps at five years. For working-age adults, “to age 65” is the right choice almost every time.

- Own-occupation definition. The strongest policy language costs more. It’s also worth more.

- Your health history. Underwriters look at your medical records. Pre-existing conditions can mean exclusion riders or higher premiums.

Shop with an independent broker who works with multiple carriers — not a captive agent tied to one company. The pricing spread between carriers for the same coverage can be significant.

People Also Ask – PAA’s

How much disability insurance do I need for a $200k salary?

Your monthly net income is around $11,667. Your essential expenses likely run $7,000 to $9,000 a month. After accounting for SSDI (likely $2,800 to $3,200 for a high earner) and group LTD (check your cap), most people at this income level still have a $1,500 to $4,000/month gap. Run the four-step calculator above with your actual numbers rather than relying on any rule of thumb.

What is the SGA limit for 2026?

The Substantial Gainful Activity (SGA) limit for 2026 is $1,690 per month for non-blind individuals and $2,830 per month for blind individuals. If you earn above the SGA limit, the SSA considers you not disabled, and you won’t qualify for SSDI benefits. This threshold matters especially if you’re trying to do part-time work while applying.

How long does it take for SSDI to start?

There’s a mandatory five-month elimination period after your disability onset date — no exceptions. After that, processing can take another 12 to 24 months. Initial denials are common; many successful applicants get approved on appeal. Private IDI starts paying after your elimination period (usually 90 days) without a multi-year approval battle.

Can I collect both SSDI and private disability insurance?

Yes — with a catch. Individually-owned IDI policies generally pay independently of SSDI. But most employer-sponsored group LTD plans include a Social Security offset clause. Once your SSDI benefit begins, your group plan benefit gets reduced dollar-for-dollar. That’s why you can’t just add SSDI and group LTD together as if they’re separate streams.

How do I calculate disability insurance coverage if I’m self-employed?

Start with your average monthly net income over the past 24 months. Target 60–70% of that figure as your total monthly coverage goal. Subtract your projected SSDI benefit (find yours at ssa.gov). The remainder is what you need from private IDI. Most carriers require 2 years of tax returns to verify self-employment income.

How much short term disability insurance do I need as someone who’s pregnant or planning to be?

Buy before you’re pregnant — that’s the most important answer. Plan for 6 to 8 weeks of benefit at 60–70% of your income. If your employer offers short-term disability as a voluntary benefit, elect it at open enrollment even if you’re not planning pregnancy yet. Once you’re pregnant, it’s a pre-existing condition and you likely can’t buy it.

Back to my neighbor, the dentist with the broken wrist.

He’s fine now. Back at work, savings rebuilt. But he spent about six months regretting that he’d never actually looked at his policy. He’d bought disability insurance the same way most of us buy it — because HR said to, not because he understood what he was actually purchasing.

He now carries a supplemental individual IDI policy on top of his group plan. True own-occupation definition. 90-day elimination. COLA rider. It costs him $230 a month.

He told me it’s the best $230 he spends every month because he knows exactly what it does.

That’s the goal of this guide. Not to scare you. Not to sell you something. To get you to actually run the numbers — once, deliberately — so you know where you stand.

Run the four steps. Find your gap. Then decide what to do about it with eyes open.

About the Author

This guide was written by a licensed financial planning professional specializing in income protection, Social Security benefit analysis, and retirement income strategy. The author has spent over a decade working with individual clients on disability coverage analysis across income levels from $60,000 to $500,000.

This article is for informational purposes only. It does not constitute financial, insurance, or legal advice. Social Security figures cited reflect 2026 SSA benchmarks and are subject to annual change. Consult a licensed insurance professional before purchasing any disability income policy.